Question

(a) From the following information, calculate Cash flow from Operating Activities.

Additional Information:-

Proposed Dividend for the year ended March 31, 2023 and March 31, 2024 was ₹1,50,000 and ₹1,80,000 respectively.

(b) From the following information calculate the Cash from Investing Activities.

Additional Information:-

(i) Machinery costing ₹ 50,000 (Book Value ₹ 40,000) was lost by fire and insurance claim of ₹ 32,000 was received.

(ii) Depreciation charged during the year was ₹ 3,50,000.

(iii) A part of Machinery costing ₹ 2,50,000 was sold at a loss of ₹ 20,000.

| Particulars | 31 March 2023 | 31 March 2024 |

| Surplus i.e Balance in Statement of Profit and Loss | 6,00,000 | 5,00,000 |

| Provision for Tax | 1,00,000 | 1,20,000 |

| Trade Receivables | 2,00,000 | 2,40,000 |

| Trade Payables | 1,50,000 | 2,00,000 |

| Goodwill | 2,00,000 | 1,50,000 |

Proposed Dividend for the year ended March 31, 2023 and March 31, 2024 was ₹1,50,000 and ₹1,80,000 respectively.

(b) From the following information calculate the Cash from Investing Activities.

| Particulars | 31 March 2023 | 31 March 2024 |

| Machinery (Cost) | 20,00,000 | 28,00,000 |

| Accumulated Depreciation | 4,00,000 | 6,50,000 |

(i) Machinery costing ₹ 50,000 (Book Value ₹ 40,000) was lost by fire and insurance claim of ₹ 32,000 was received.

(ii) Depreciation charged during the year was ₹ 3,50,000.

(iii) A part of Machinery costing ₹ 2,50,000 was sold at a loss of ₹ 20,000.

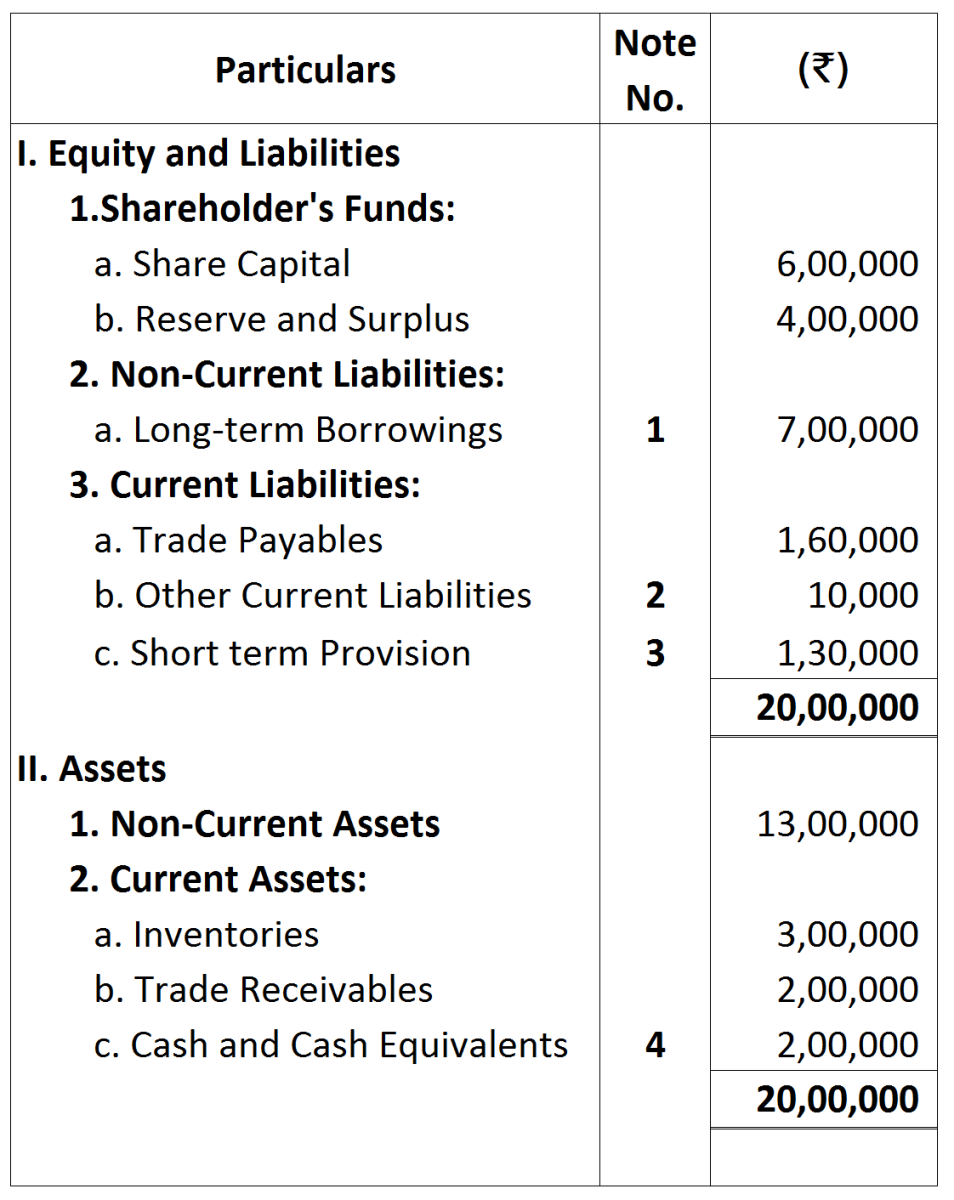

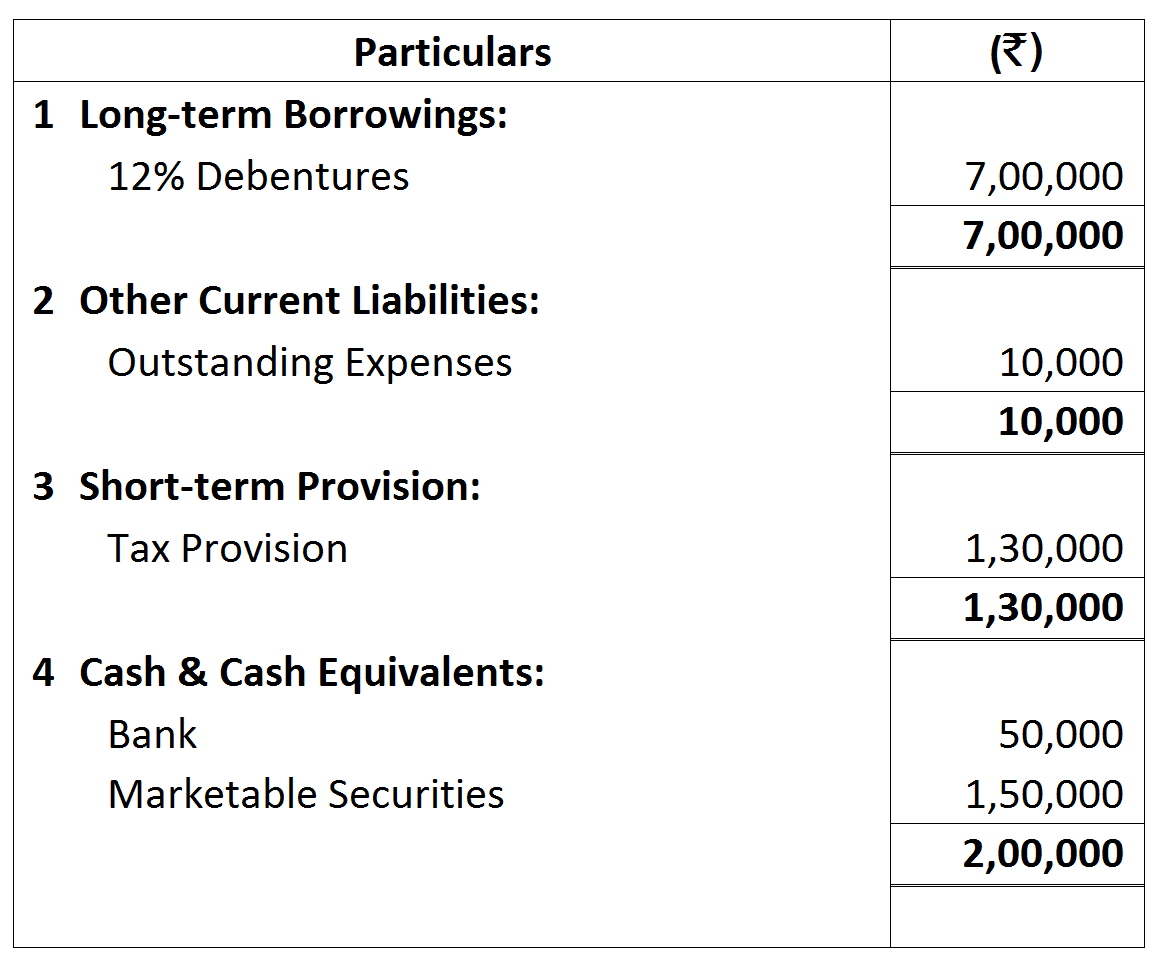

Note:

Note:

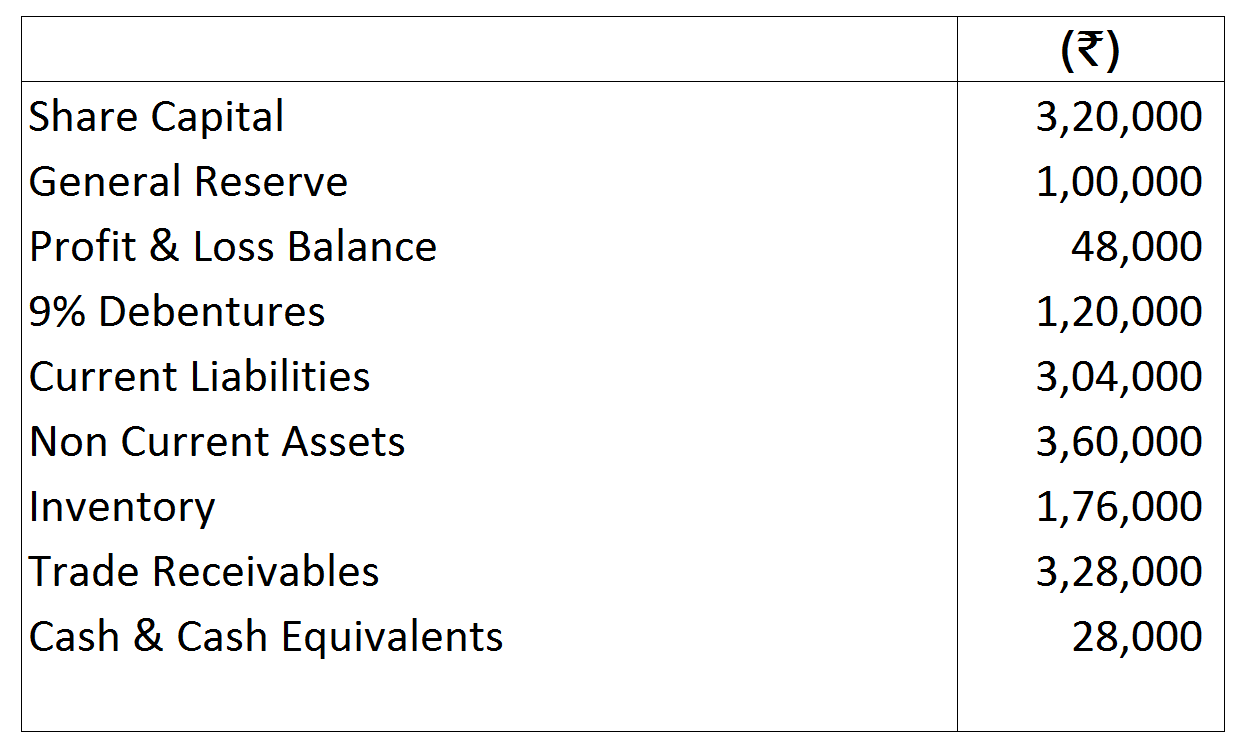

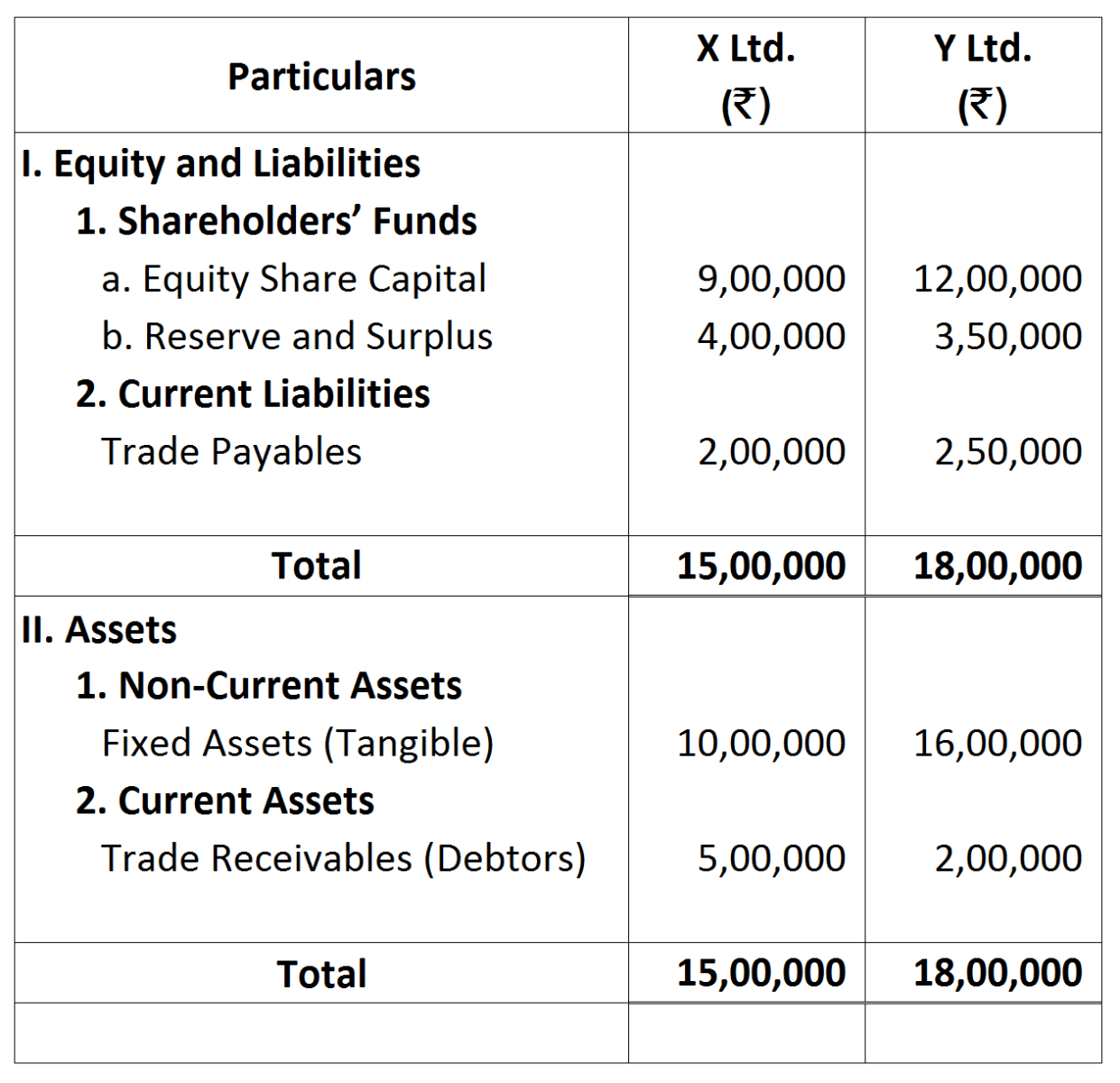

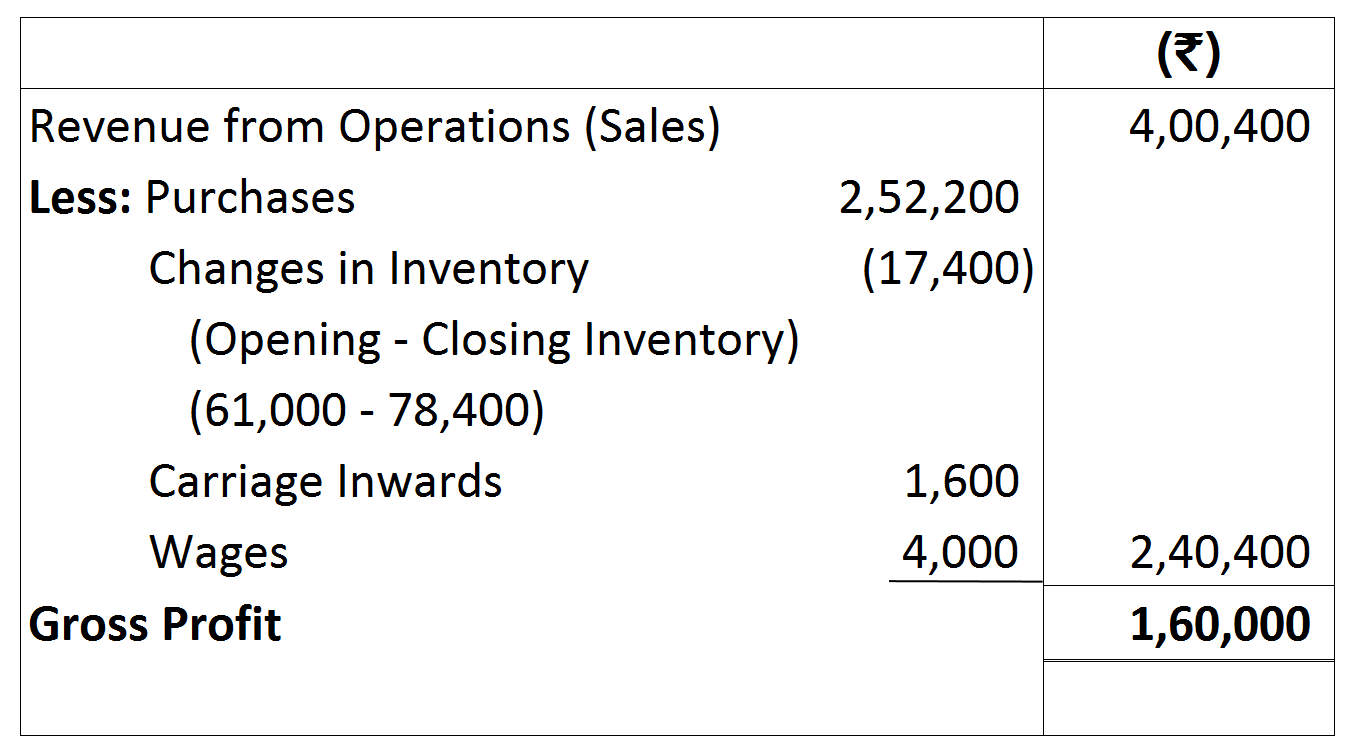

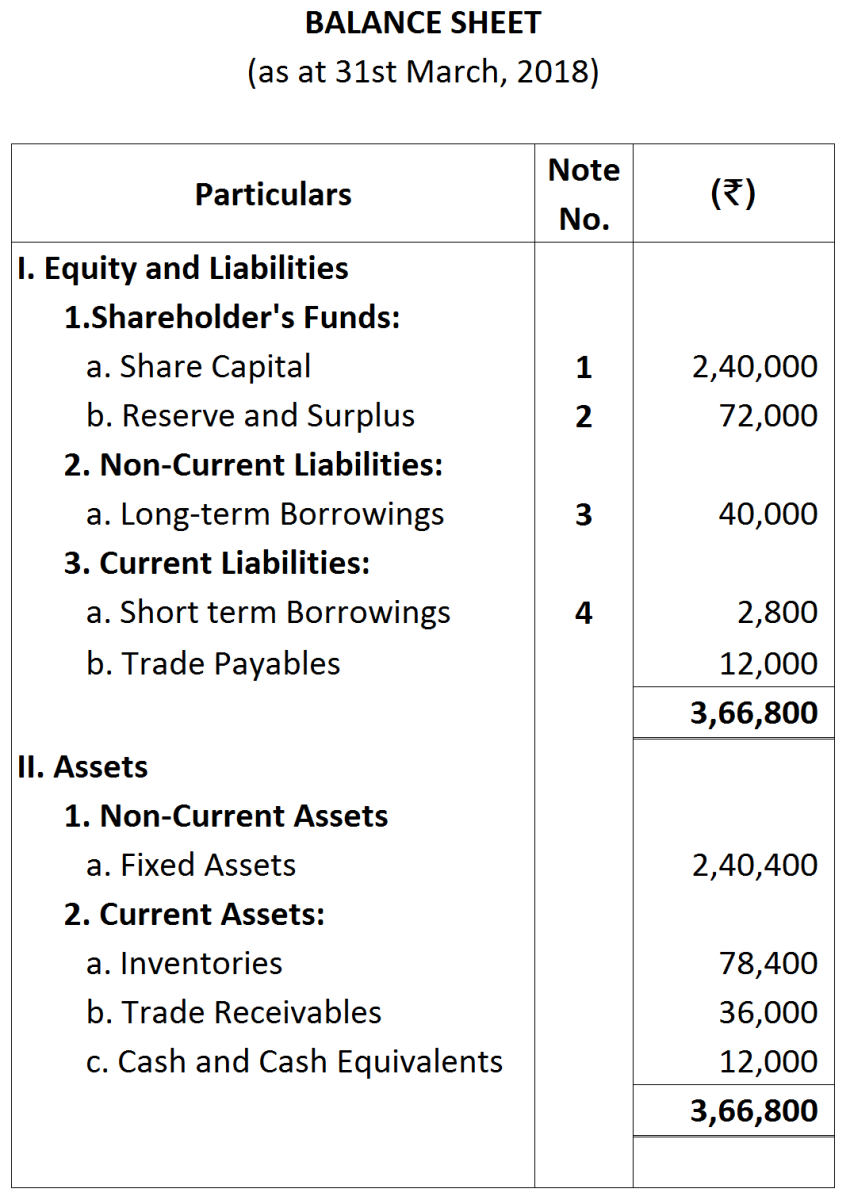

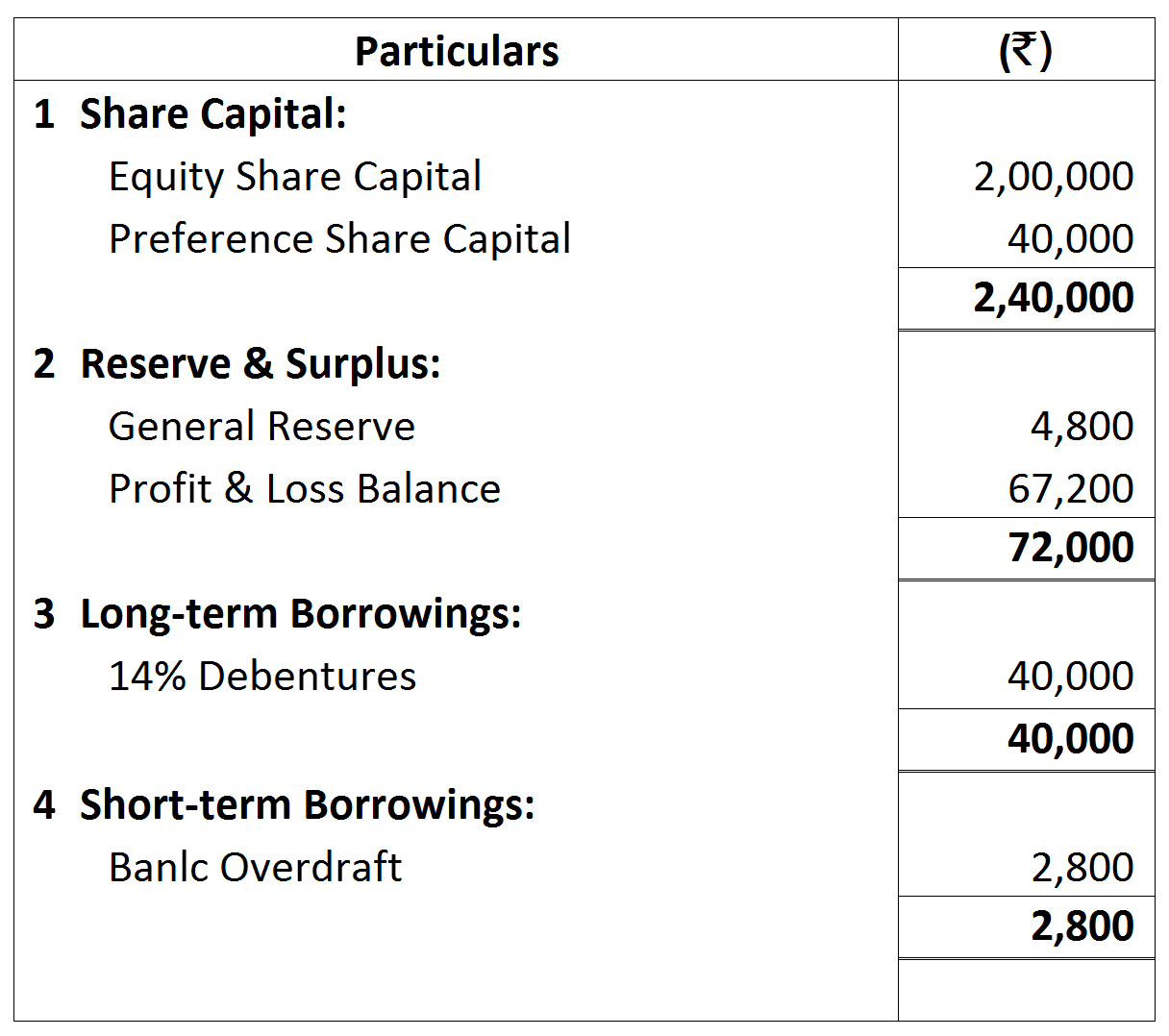

Calculate the following ratios and indicate the purpose which they serve:

Calculate the following ratios and indicate the purpose which they serve: