Question

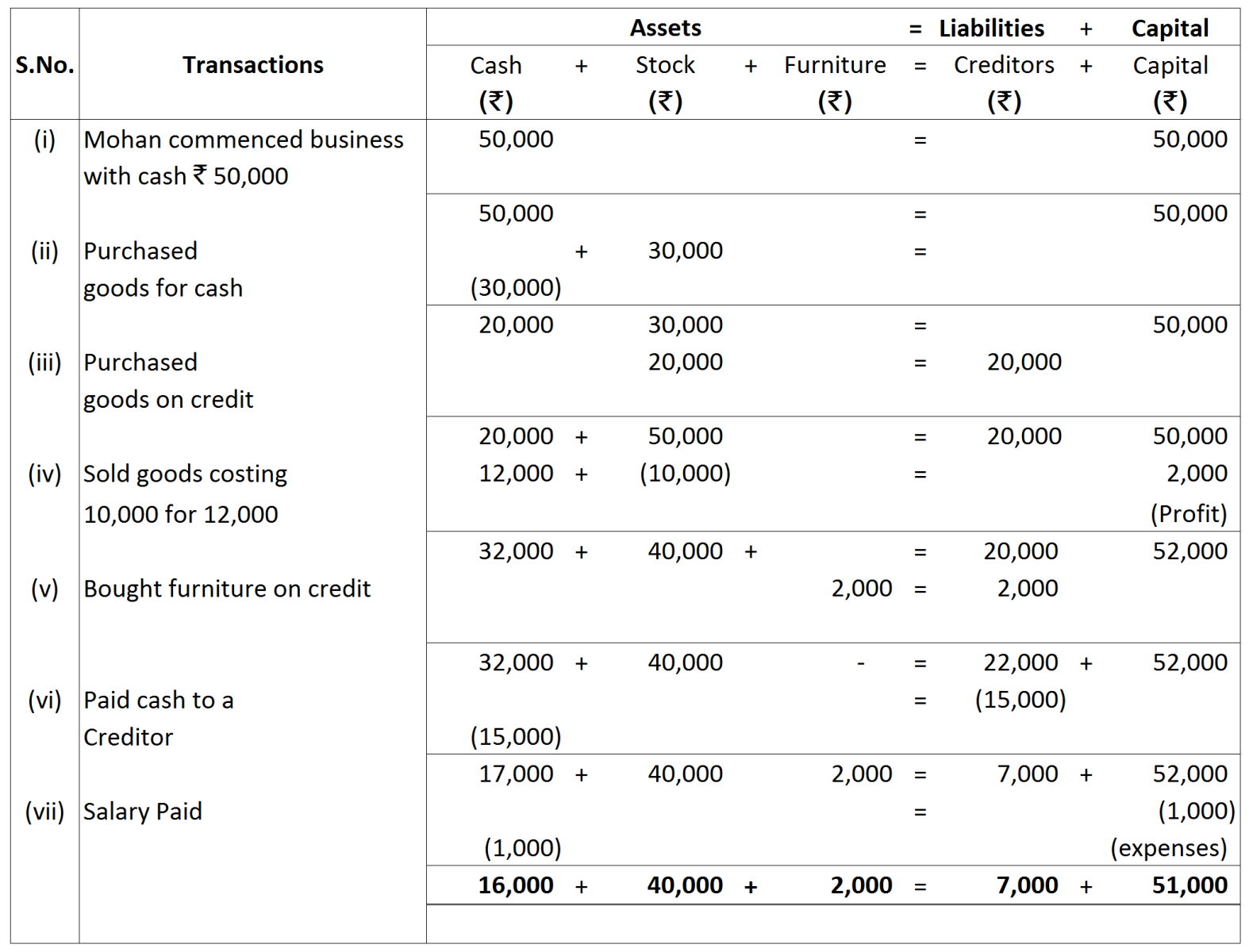

Develop an Accounting Equation from the following transactions:

| S.no | ₹ | |

| (i) | Mohan commenced business with cash | 50,000 |

| (ii) | Purchased goods for cash | 30,000 |

| (iii) | Purchased goods on credit | 20,000 |

| (iv) | Sold goods (costing ₹ 10,000) for | 12,000 |

| (v) | Bought furniture on credit | 2,000 |

| (vi) | Paid cash to a creditor | 15,000 |

| (vii) | Salary paid | 1,000 |