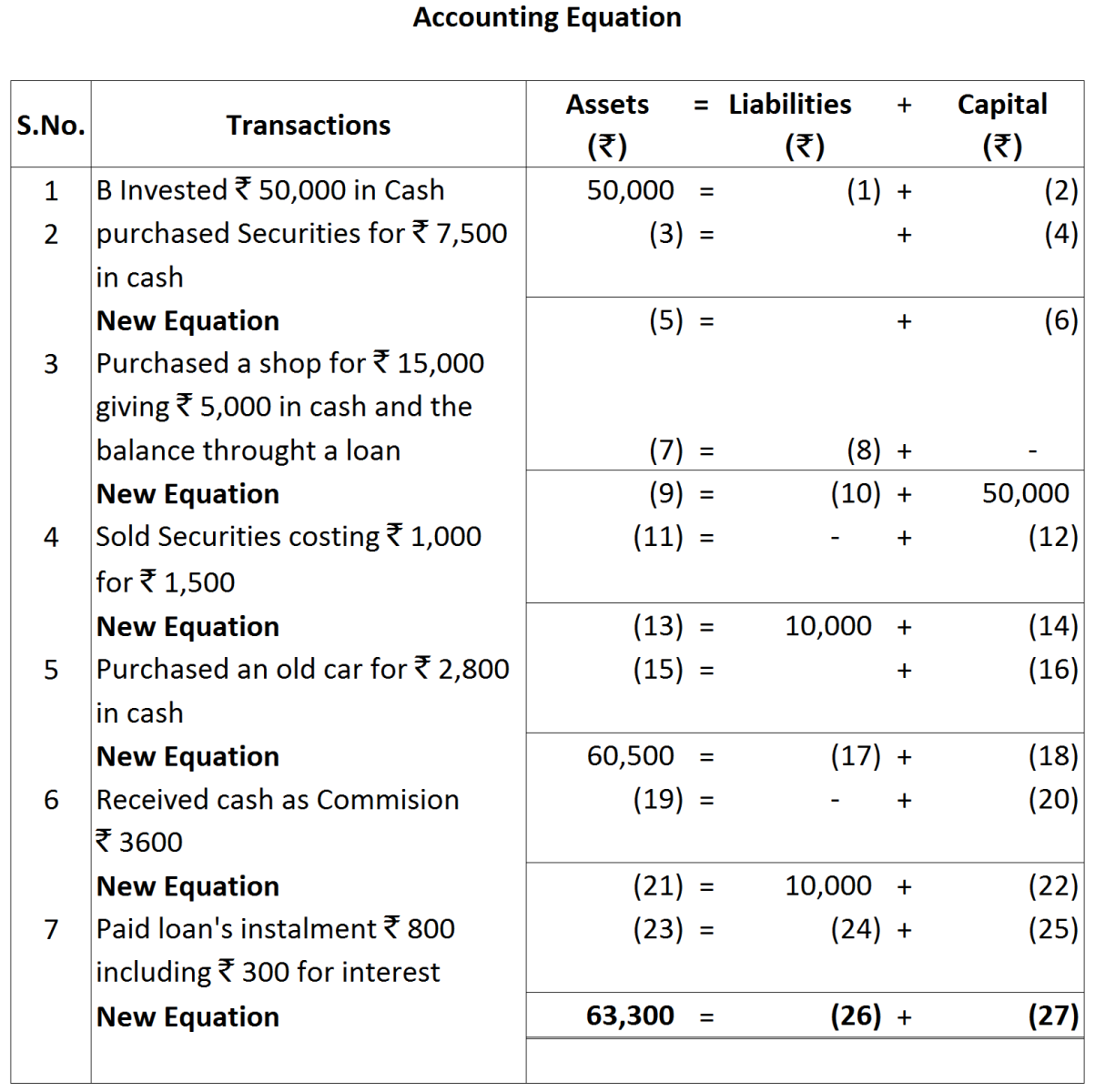

Question

Elucidate the following statement:

Cash Book is both Journal and Ledger'.

Cash Book is both Journal and Ledger'.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

May 1

|

Balance of Cash in Hand ₹ 12,400; Bank Overdraft ₹ 36,000

|

|

May 3

|

Direct deposit by Mr. Ganesh in our bank account ₹ 10,000. Discount allowed ₹ 200

|

|

May 5

|

Issued a cheque of ₹ 7,700 to Mr. Suresh in full settlement of his account of ₹ 8,000

|

|

May 6

|

Received a cheque from X for ₹ 12,000. Discount allowed ₹ 500. This cheque was deposited into bank on 7th May

|

|

May 8

|

Received Cash ₹ 22,000 and cheque of ₹ 8,000 for cash sale

|

|

May 12

|

Cash sale ₹ 70,000 of which ₹ 55,000 banked

|

|

May 15

|

Cheque received on 8th May endorsed to Mr. Sunil. Discount received ₹ 150

|

|

May 20

|

Discounted a B/R of ₹ 10,000 at 1% through bank

|

|

May 24

|

Cheque received from X dishonoured, Bank debits ₹ 20 in respect of bank charges

|

|

May 25

|

Purchased goods for ₹ 50,000 at a trade discount of 10%. Payment was made in cash

|

|

May 26

|

Withdrew from bank ₹ 10,000 for office use and ₹ 2,000 for personal use

|

|

May 31

|

Interest debited by Bank ₹ 4,500

|

|

2017

|

|

₹

|

|

Jan. 1

|

Paid into bank for opening a Current Account

|

10,000

|

|

Jan. 3

|

Goods sold for ₹ 50,000 and the amount was deposited into the bank

|

|

|

Jan. 7

|

Amount withdrawn from bank

|

20,000

|

|

Jan. 10

|

Goods sold for Cash

|

15,000

|

|

Jan. 12

|

Amount deposited into bank

|

12,000

|

|

Jan. 14

|

Goods purchased and payment made by cheque.

|

25,000

|