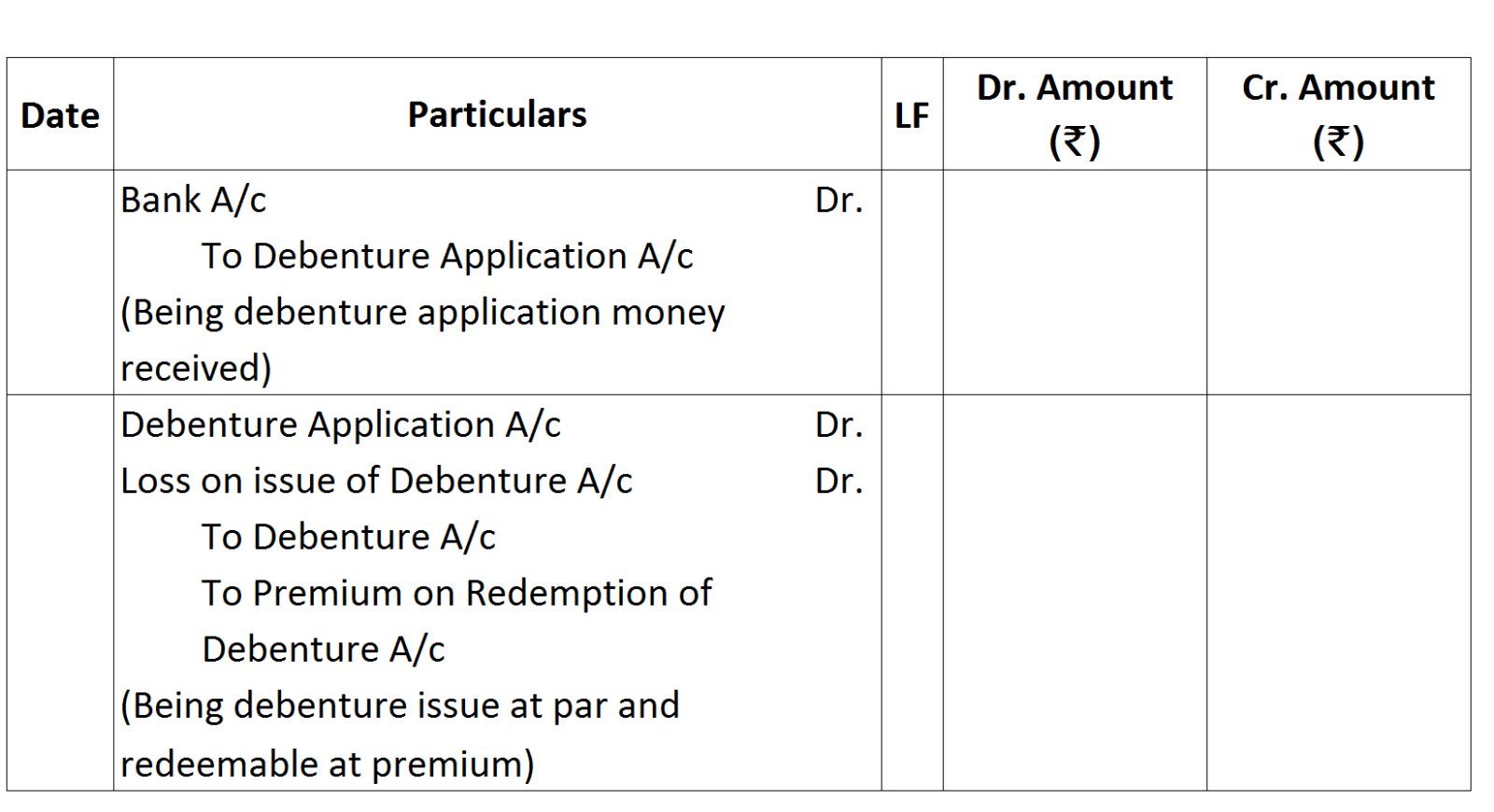

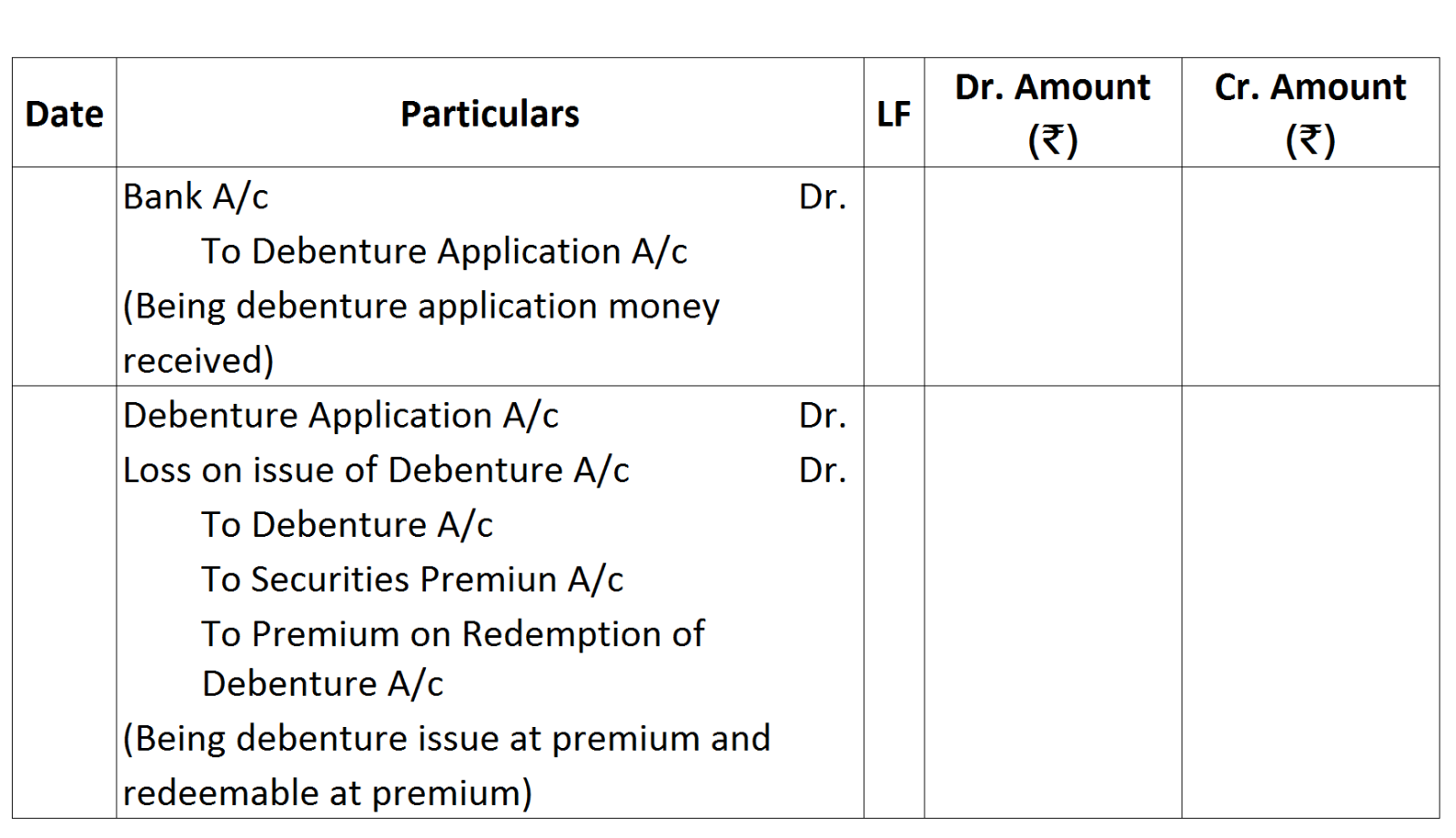

Question

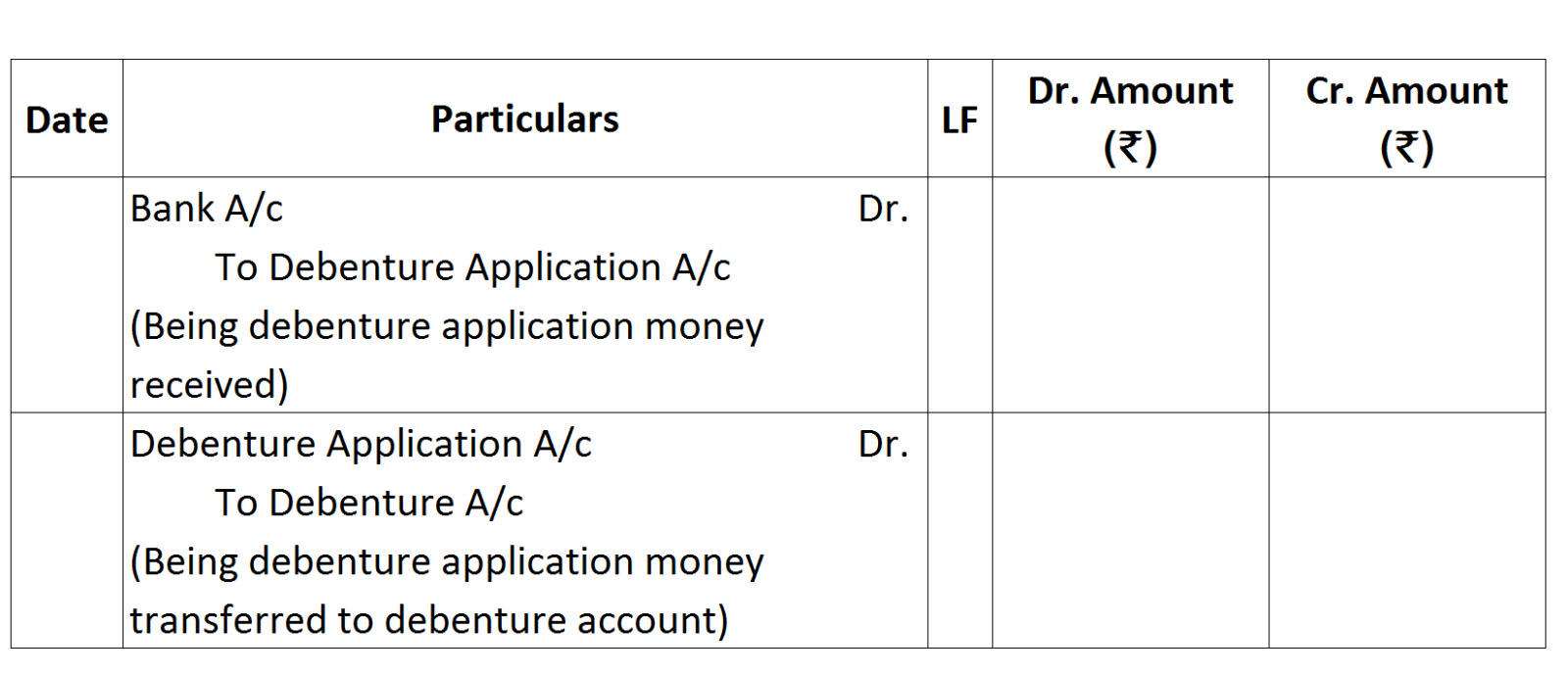

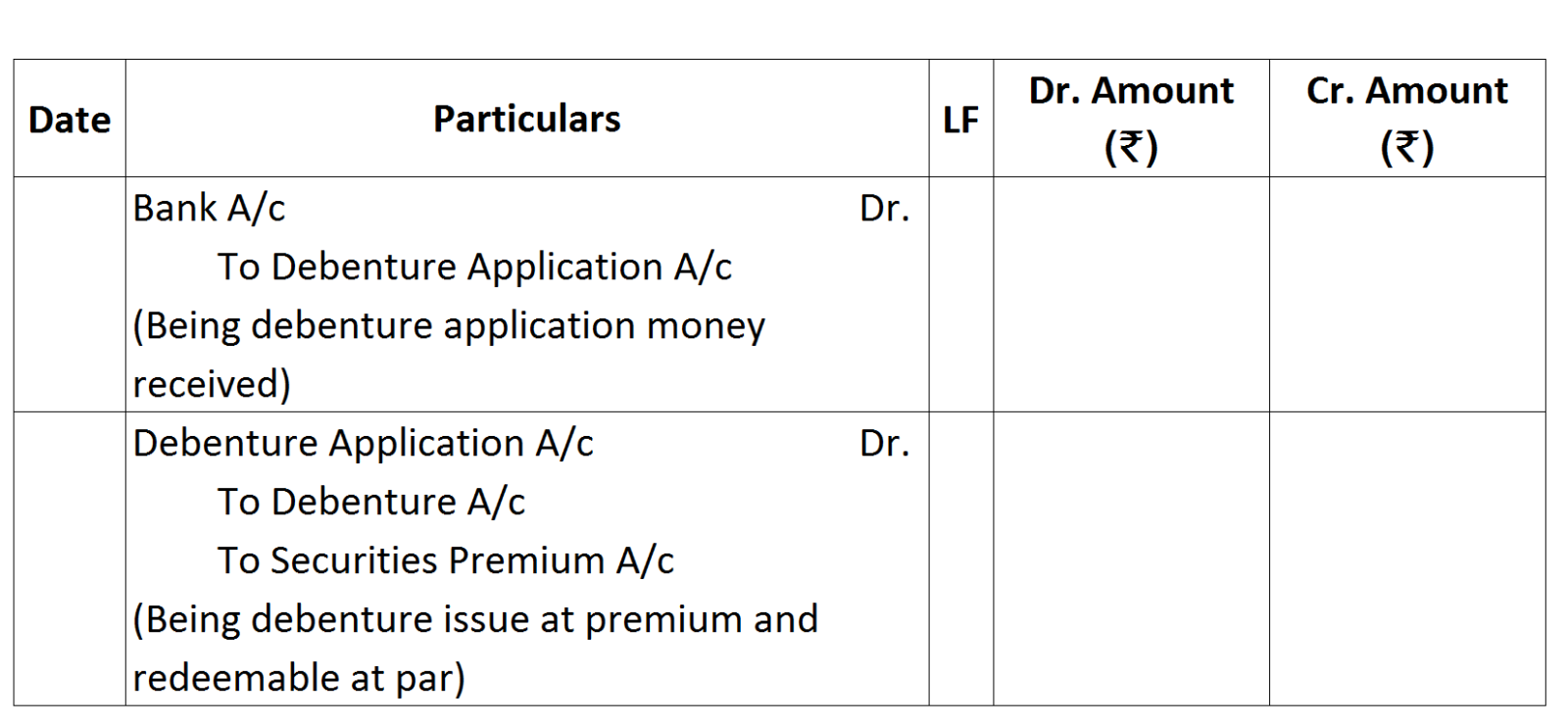

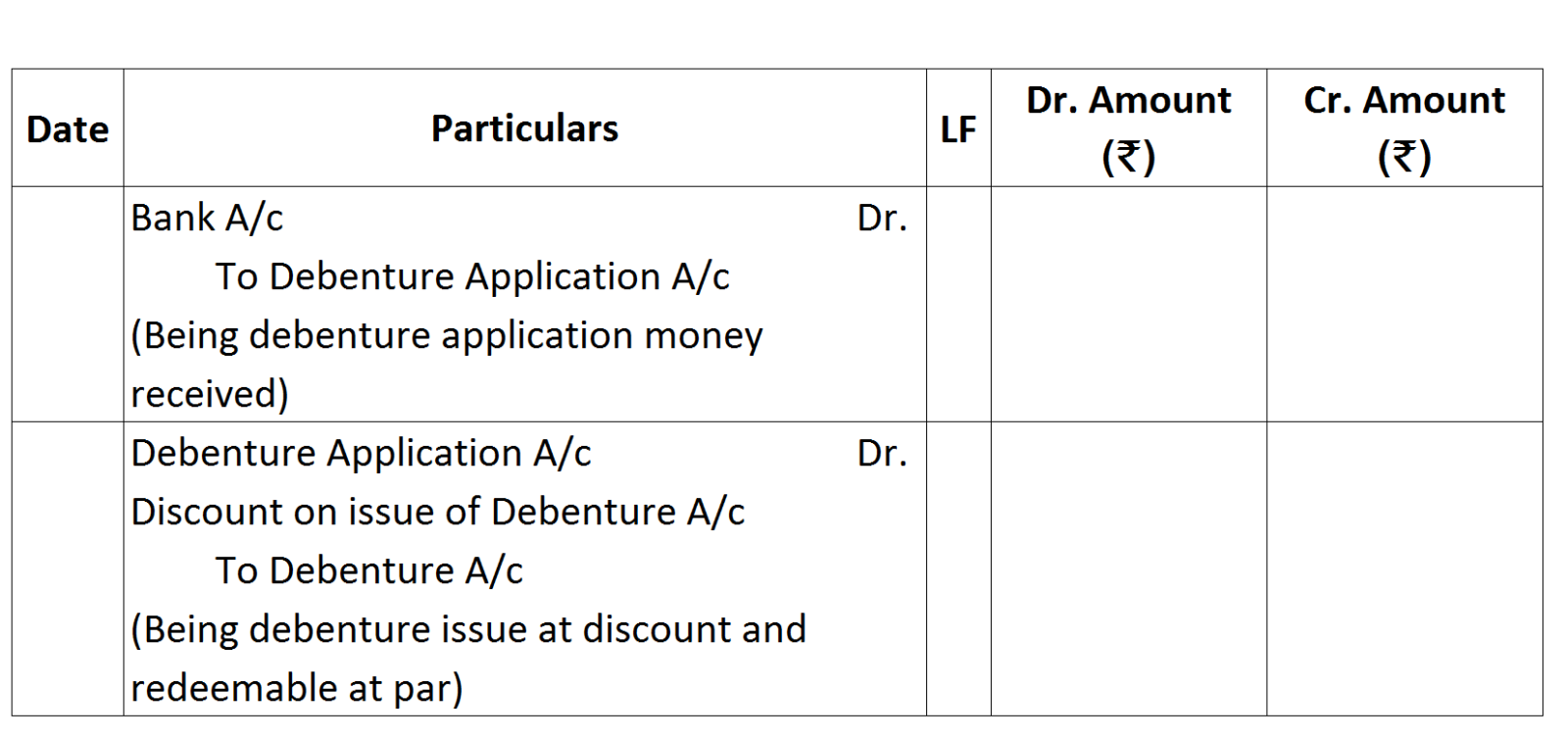

Explain the different terms for the issue of debentures with reference to their redemption.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

Particulars

|

₹

|

|

Net Profit after Provision for Tax nd Payment of Dividend

Provision for Tax

Final Dividend paid during the year

Depreciation

Loss on Sale of Machinery

Patents Amortised

Gain on Sale of Land

Income Tax Refund

|

2,15,000

45,000

50,000

25,000

10,000

30,000

70,000

30,000

|

Notes to Account:

Notes to Account: Additional Information: Depreciation for the year was ₹ 75,000.

Additional Information: Depreciation for the year was ₹ 75,000.|

|

₹

|

|

Paid up Capital

|

20,00,000

|

|

Capital Reserve

|

2,00,000

|

|

9% Debentures

|

8,00,000

|

|

Net Sales

|

14,00,000

|

|

Gross Profit

|

8,00,000

|

|

Indirect Expenses

|

2,00,000

|

|

Current Assets

|

4,00,000

|

|

Current Liabilities

|

3,00,000

|

|

Opening Stock

|

50,000

|

|

Closing Stock ---- 20% more than opening stock

|

|