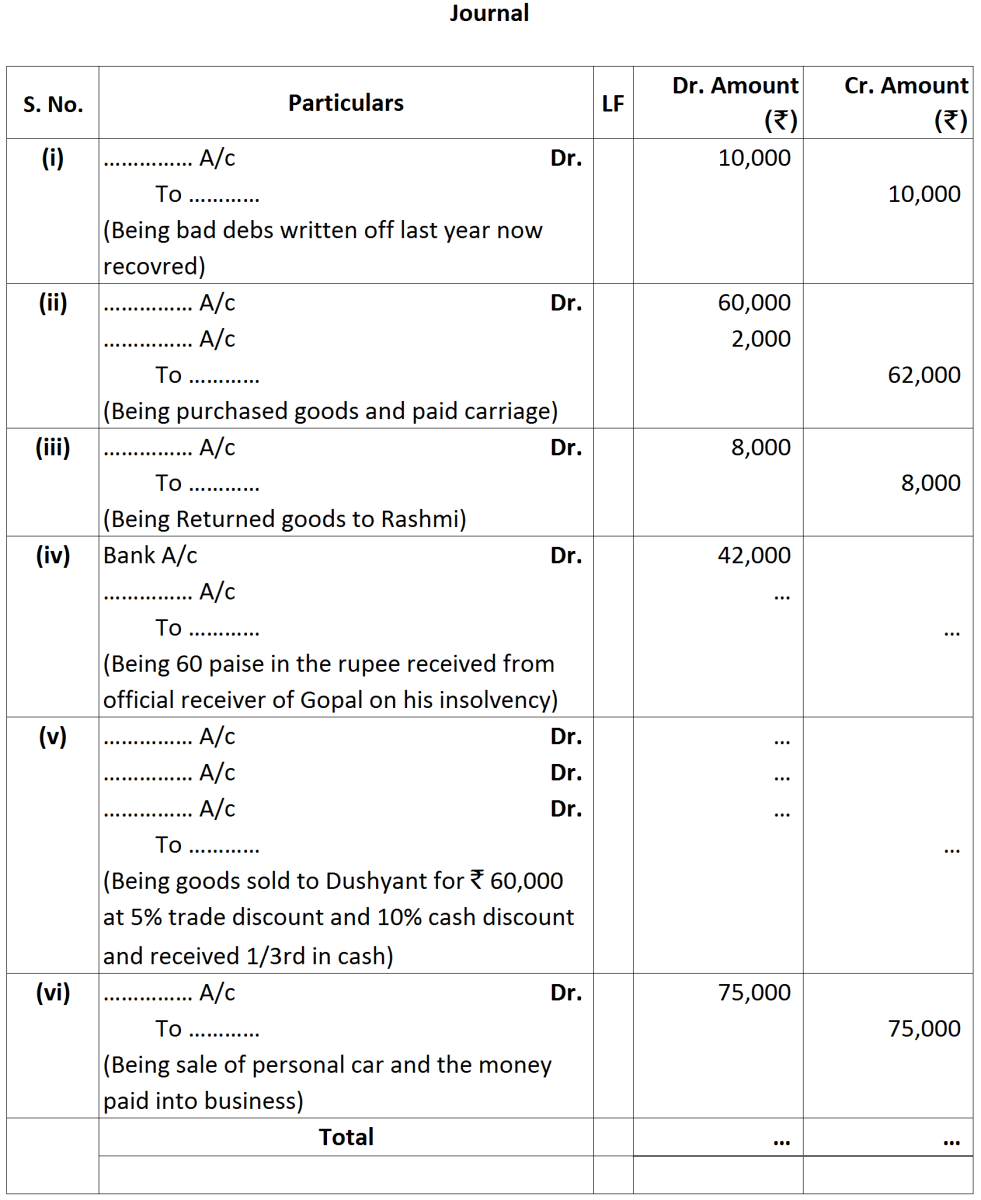

Question

Fill in the missing information in the following journal entries:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2017

|

|

|

Jan. 2

|

Purchased Typewriter for ₹ 7,500

|

|

Jan. 4

|

Sold goods for Cash of the list price of ₹ 25,000 at 20% trade discount and 5% Cash discount

|

|

Jan. 6

|

Sold goods to Gopal Seth for ₹ 10,000

|

|

Jan. 8

|

Gopal Seth returned goods for ₹ 1,500

|

|

Jan. 12

|

Purchased goods from Arun ₹ 12,000, and from varun ₹ 15,000

|

|

Jan. 13

|

Settled Arun's account in full after deducting 5% for cash discount

|

|

Jan. 14

|

Paid cash to Ghanshyam in full settlement of his account

|

|

Jan. 16

|

Received ₹ 7,500 from Lal Chand in full settlement of his account

|

|

Jan. 17

|

Purchased a Scooter for office use ₹ 18,000

|

|

Jan. 20

|

Sold goods for cash 20,000

|

|

Jan. 22

|

Received from Gopal Seth ₹ 4,850 and discount allowed ₹ 150

|

|

Jan 27

|

Paid for Wages ₹ 7,000 and Salaries ₹ 3,000.

|

|

Jan. 28

|

Withdrew goods for ₹ 2,000 and Cash ₹ 1,500 for private use

|

|

Jan. 29

|

Paid for Life Insurance Premium of the Proprietor ₹ 1,600

|

|

|

|

₹

|

|

(a)

|

Cash Book Balance (Overdraft)

|

12,500

|

|

(b)

|

Cheques deposited but not recorded in Cash Book

|

2,000

|

|

(c)

|

Cheque received but not sent to Bank

|

1,500

|

|

(d)

|

Credit side of the Bank Column has been overcast

|

60

|

|

(e)

|

Bank charges entered in Pass Book twice

|

75

|

|

(f)

|

Bills Receivable directly collected by the Bank

|

4,000

|

|

(g)

|

Deposited cheques returned dishonoured by Bank

|

1,700

|

|

(h)

|

Electricity Bill paid by Bank as per instruction

|

800

|

|

(i)

|

Cheques issued but not presented for payment

|

5,400

|

|

(j)

|

Cheques deposited but not cleared

|

3,200

|

|

2019

|

|

₹

|

|

April 2

|

Bought office furniture

|

20,000

|

|

April 5

|

Purchased goods

|

16,000

|

|

April 8

|

Purchased goods from Ramesh, Chandigarh

|

11,000

|

|

April 12

|

Sold goods to Sameer, Delhi

|

21,000

|

|

April 13

|

Purchased stationery for cash

|

1,800

|

|

April 13

|

Paid to Ramesh in cash on account*

|

10,000

|

|

|

Discount allowed by him*1,000

|

|

|

April 17

|

Withdrawn cash for office use*

|

4,000

|

|

April 18

|

Sen of Chandigarh sold goods to S.K. Gupta

|

30,000

|

|

April 19

|

Cash received from Sameer on account*

|

20,000

|

|

|

Allowed him discount*

|

1,000

|

|

April 20

|

Sold to Raj Banwari, Delhi

|

40,000

|

|

April 28

|

Cash sales

|

1,400

|

|

April 30

|

Paid salary by cheque*

|

8,000

|

|

April 30

|

Paid rent by cheque

|

5,000

|

|

April 30

|

Paid telephone expenses by cheque

|

2,000

|

|

April 30

|

Paid cash into bank*

|

2,000

|

|

2016

|

|

(₹)

|

|

April 2

|

Taxi fare

|

750

|

|

April 3

|

Refreshments

|

450

|

|

April 5

|

Registered postal charges

|

200

|

|

April 5

|

Wages

|

700

|

|

April 8

|

Auto fare

|

200

|

|

April 9

|

Courier charges

|

150

|

|

April 12

|

Postal Stamps

|

600

|

|

April 14

|

Eraser/ Sharpeners/ Pencils

|

400

|

|

April 17

|

Speed Post charges

|

200

|

|

April 20

|

Cartage

|

600

|

|

April 20

|

Computer Stationery

|

500

|

|

April 22

|

Wages

|

300

|

|

April 24

|

Bus fare

|

600

|

|

April 25

|

Office Sanitation

|

800

|

|

April 26

|

Refreshments

|

750

|

|

April 28

|

Loading Charges

|

300

|

|

April 30

|

Photostatting Charges

|

200

|

|

April 30

|

Wages

|

800

|