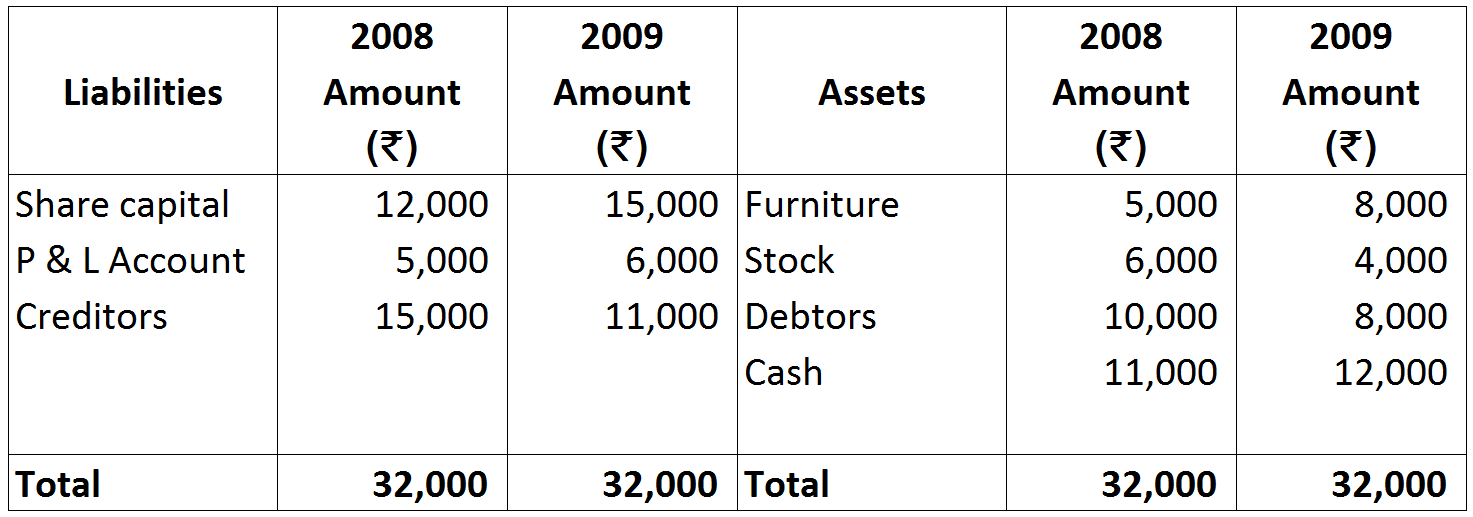

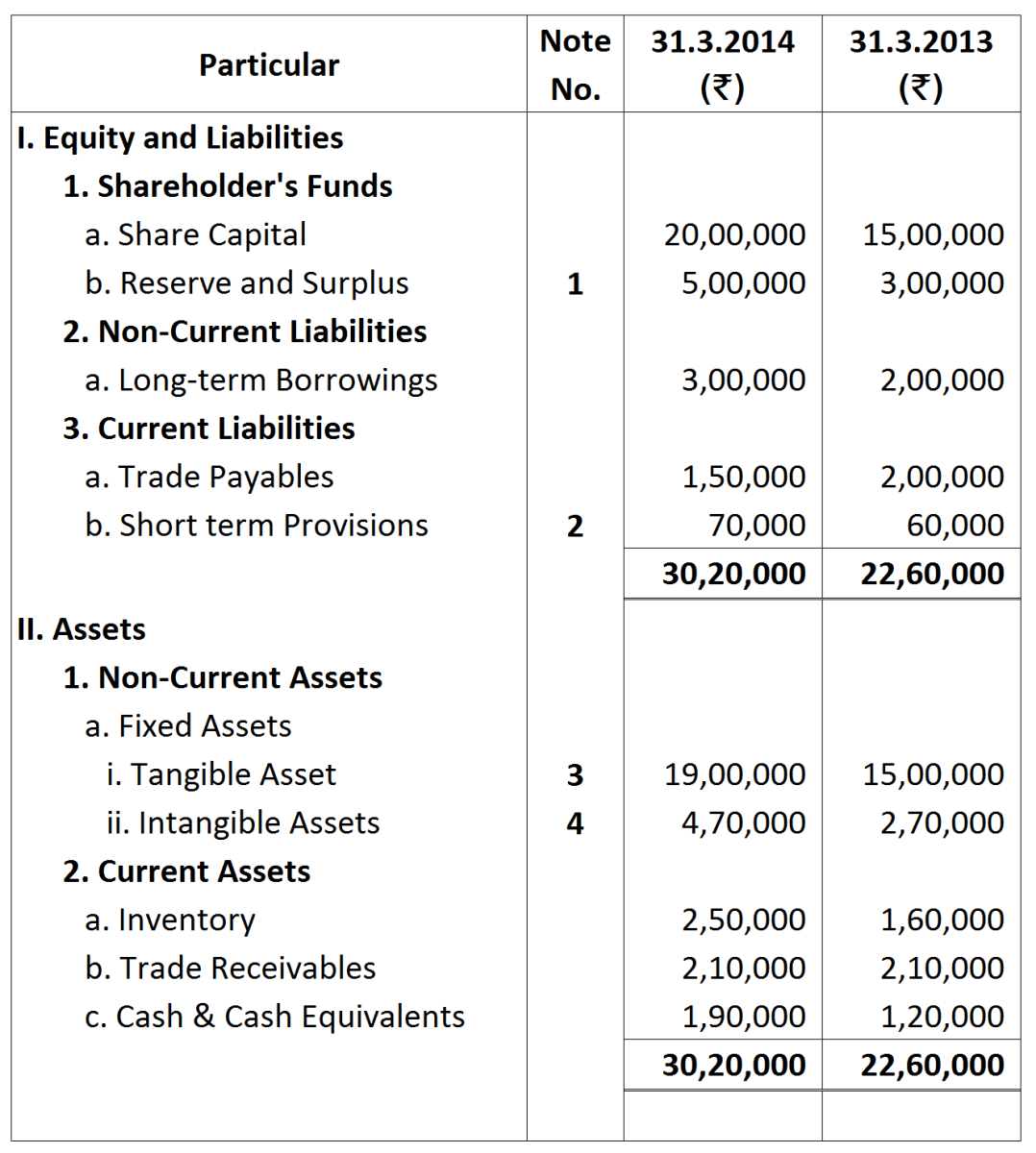

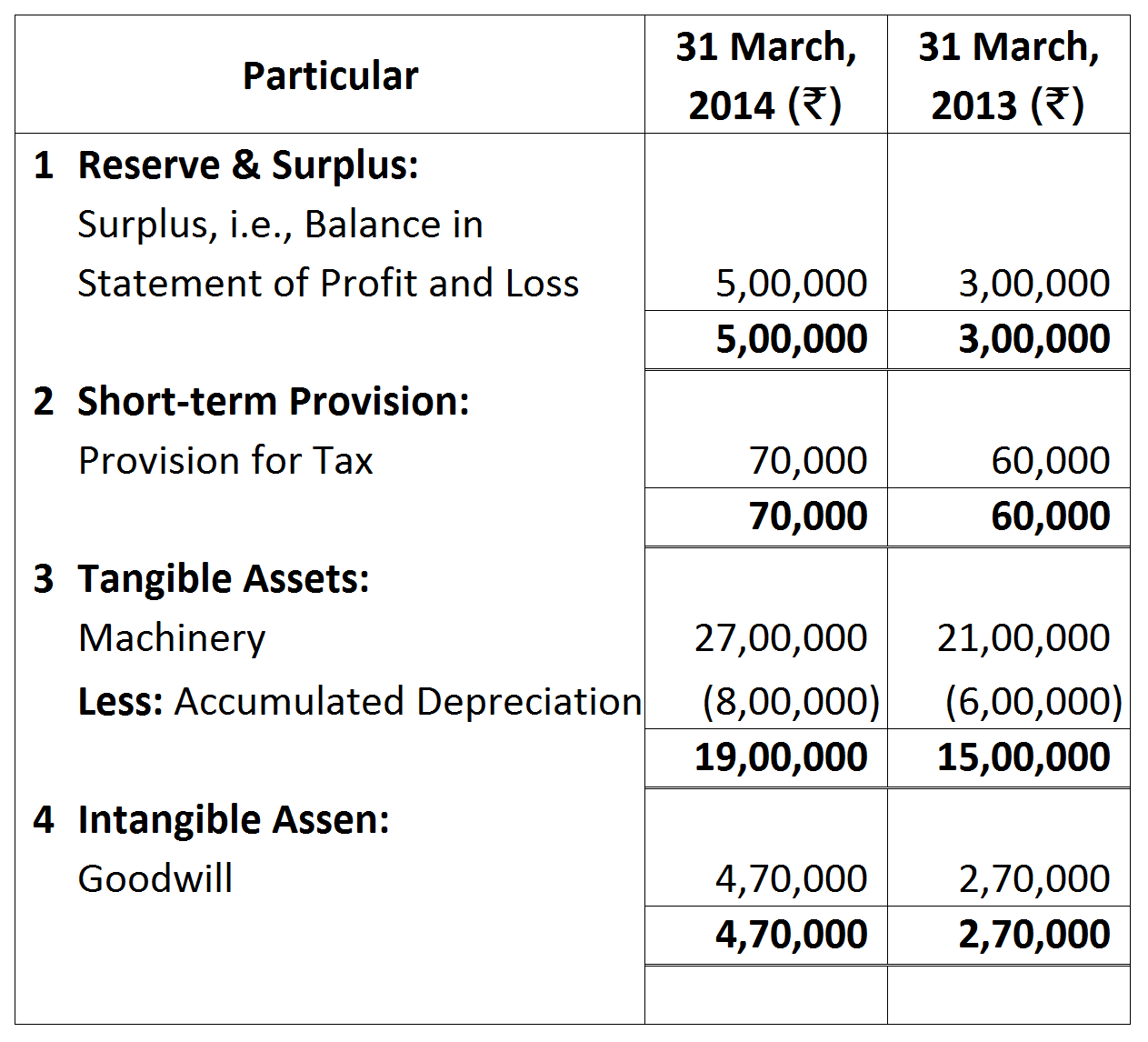

Question

From the following Balance Sheets, prepare a Cash Flow Statement as per AS-3 (revised)

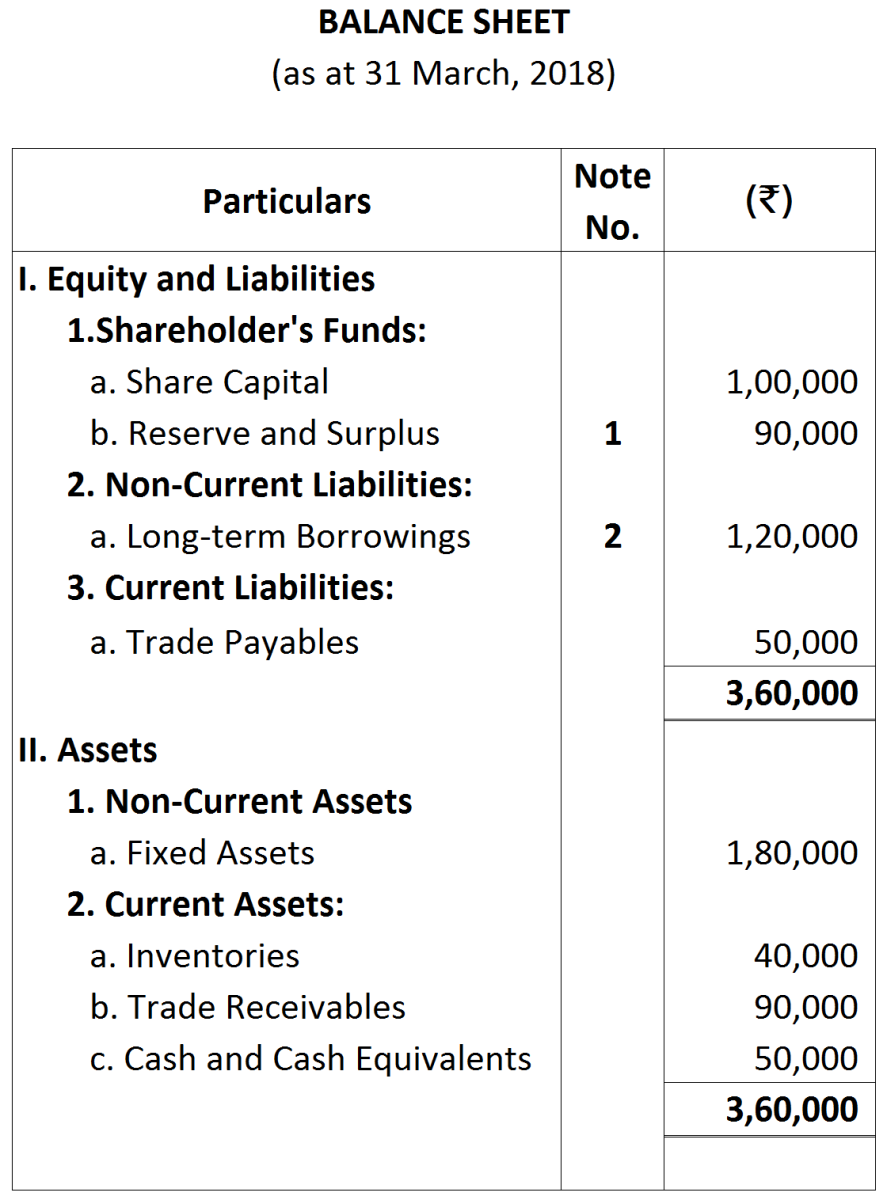

A dividend of ₹ 3,000 was paid during the year 2008-09.

A dividend of ₹ 3,000 was paid during the year 2008-09.

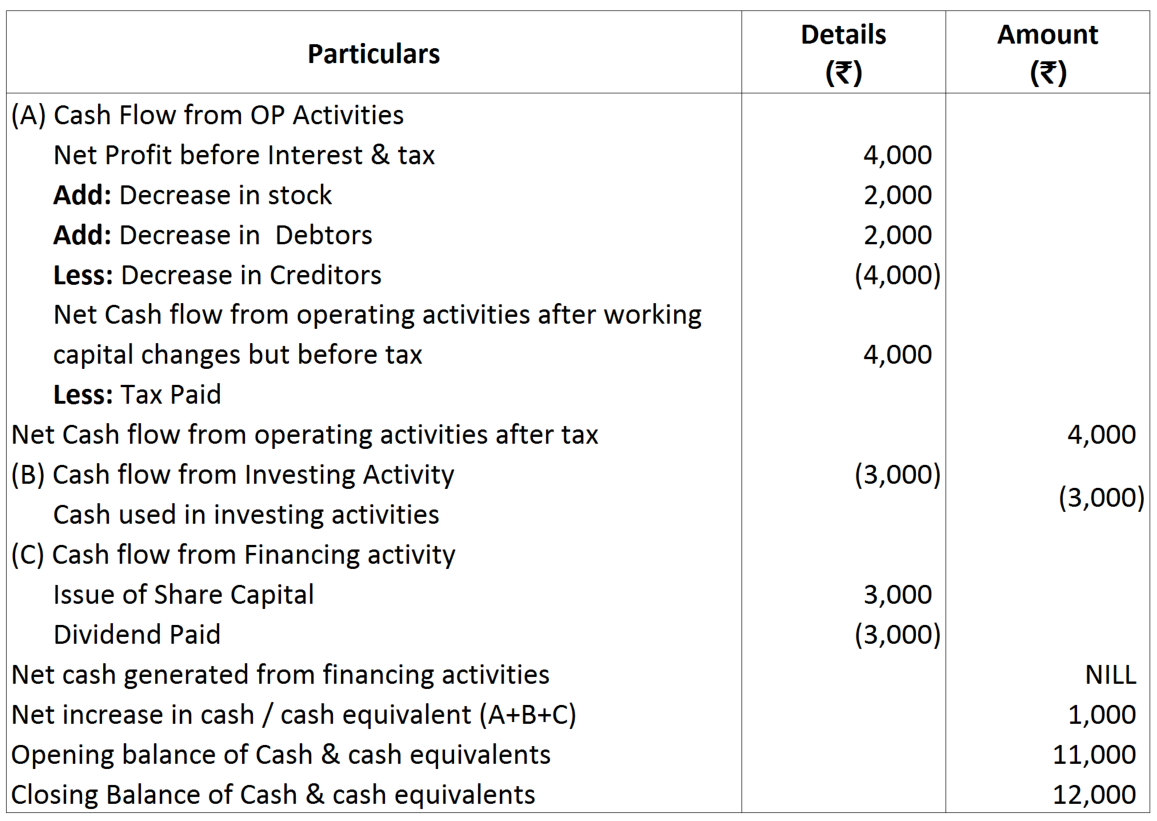

| Profit earned : | ₹ 1,000 |

| Add : Dividend: | ₹ 3,000 |

| ₹ 4,000 |

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

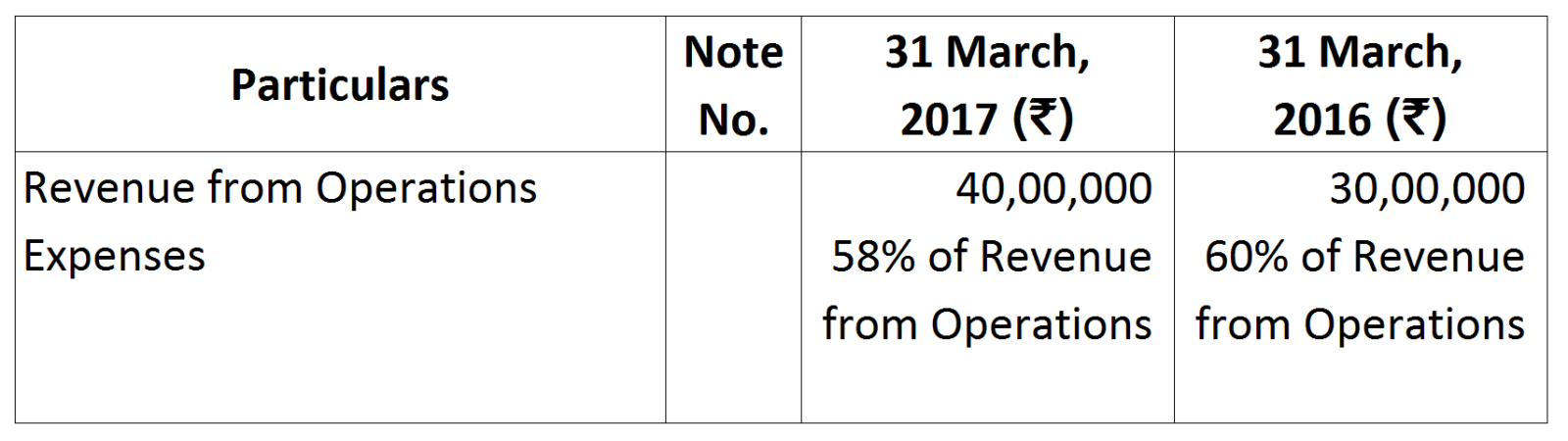

Other Information:

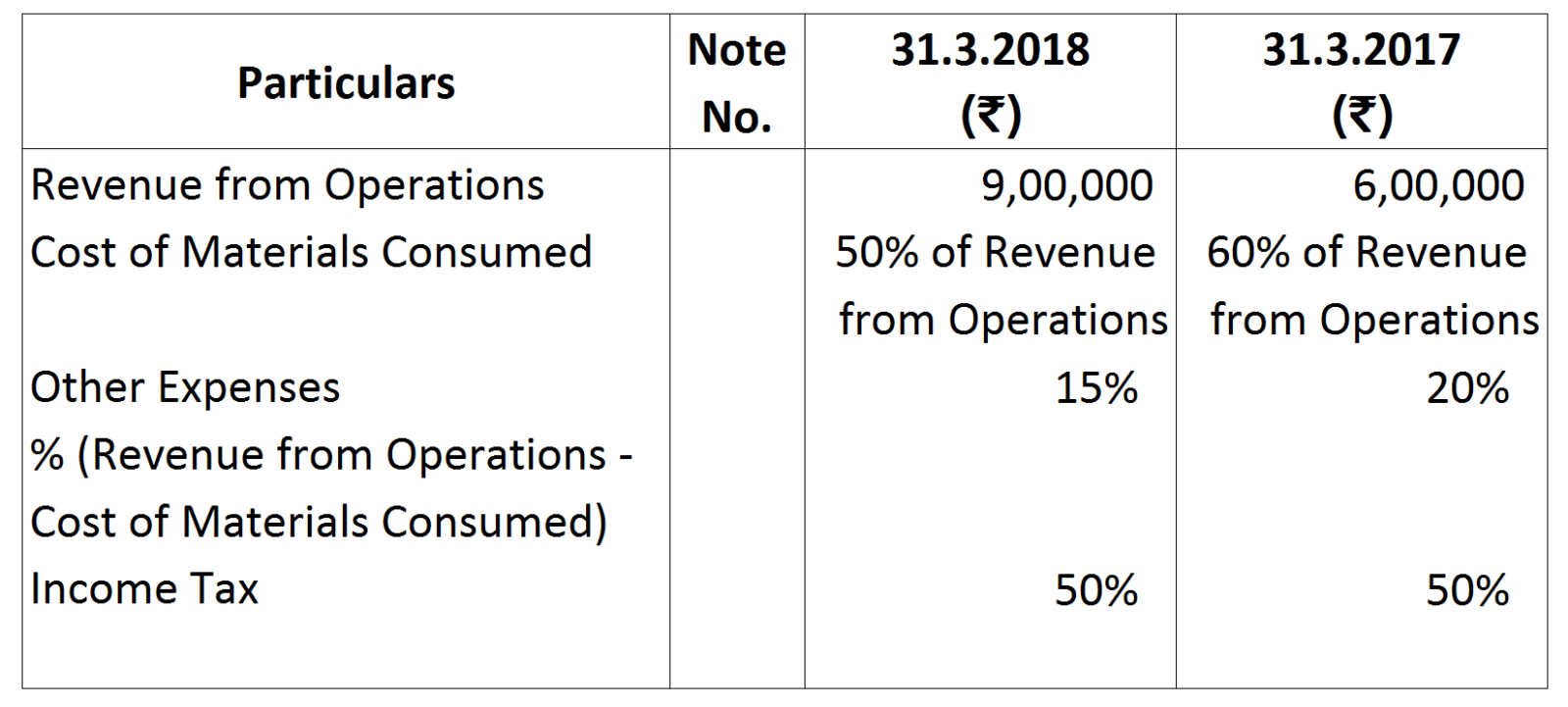

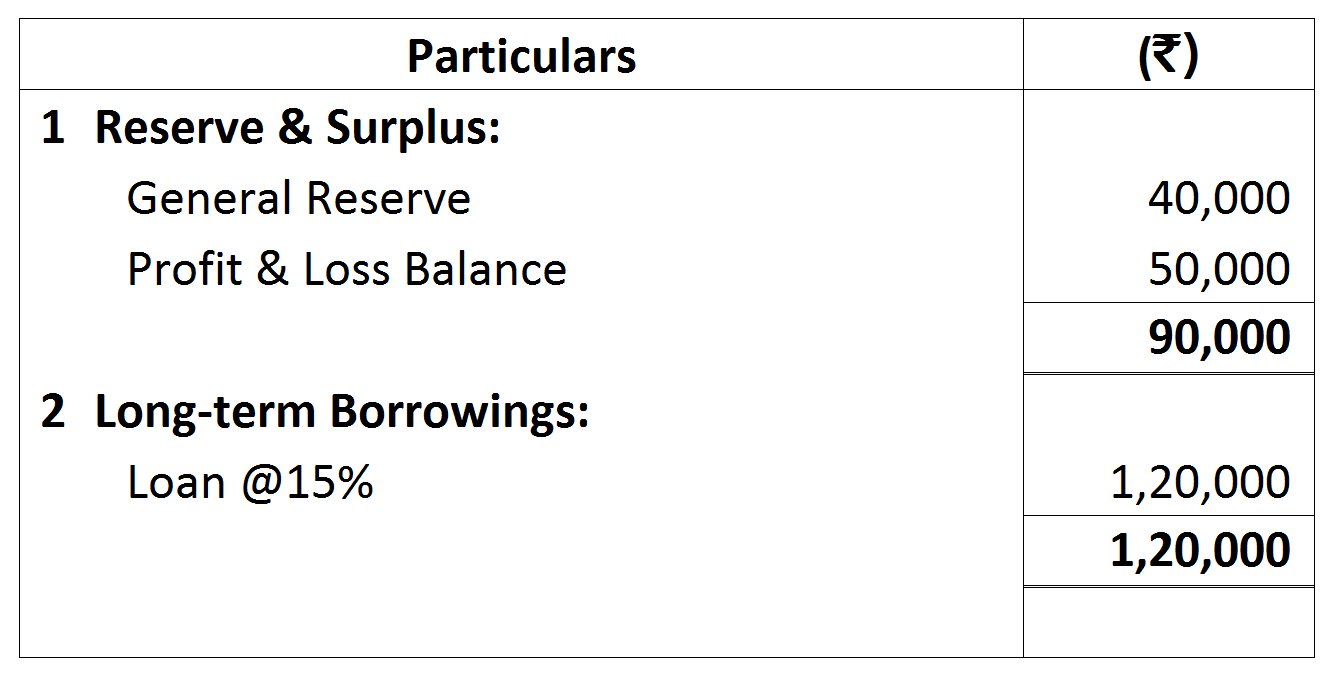

Other Information: