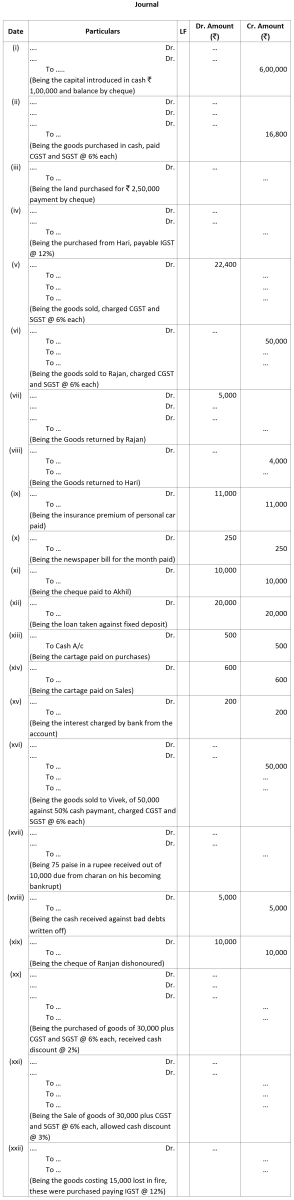

Question

On the basis of the narrations, fill in the missing values:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2017

|

|

|

March 4

|

Purchased building for ₹ 1,50,000 and incurred expenses of ₹ 10,000 on its purchase.

|

|

March 10

|

Satish who owed us ₹ 20,000 is declared insolvent and 60 paise per ₹ is received from his estate.

|

|

March 15

|

Paid ₹ 500 for repairing the office furniture.

|

|

March 18

|

Proprietor withdrew for his personal use cash ₹ 5,000 and goods worth ₹ 2,000.

|

|

March 20

|

Purchased the following items for business: Iron Safe ₹ 15,000; Filing Cabinet ₹ 5,000; Computer ₹ 12,000; Postage ₹ 200 and Stationery ₹ 150

|

|

March 28

|

Paid electricity charges ₹ 1,600.

|

|

March 31

|

Charge depreciation on Machinery @ 10% for one year (Machinery ₹ 75,000).

|

|

March 31

|

Outstanding wages at the end of the year ₹ 6,000.

|

|

2017

|

|

(₹)

|

|

March 1

|

Cash in Hand

|

1,20,000

|

|

March 2

|

Bought machinery for ₹ 60,000 and paid carriage

|

2,000

|

|

March 4

|

Bought goods for ₹ 25,000 and paid carriage

|

1,000

|

|

March 5

|

Bought goods from Ravi Das

|

15,000

|

|

March 6

|

Cash received from sale of Motor bike

|

5,000

|

|

March 8

|

Sold goods for cash less 5% cash discount

|

20,000

|

|

March 10

|

Sold goods

|

40,000

|

|

March 12

|

Paid to Ravi Das on account

|

10,000

|

|

March 15

|

Bought goods from Suresh for cash less 4% cash discount

|

30,000

|

|

March 20

|

Paid to Ravi Das

|

4,500

|

|

Discount received

|

500

|

|

|

March 25

|

Cash collected from Ashok (Debtor)

|

10,000

|

|

March 28

|

Purchased postal stamps

|

500

|

|

March 28

|

Salary paid to accountant

|

15,000

|

|

2019

|

Particular

|

₹

|

|

Jan-1

|

Bought computer for resale for cash vide Cash Memo No. 512*

|

7,200

|

|

Jan-8

|

Salary paid for the month of December, 2018

|

10,000

|

|

Jan-10

|

Sold computer for cash vide Cash Memo No. 64*

|

12,000

|

|

Jan-15

|

Withdraw cash from bank for office use vide cheque No. 13456

|

1,700

|

|

|

₹

|

|

Furniture Account

|

50,000

|

|

Provision for Depreciation on Furniture Account

|

22,000

|