Question

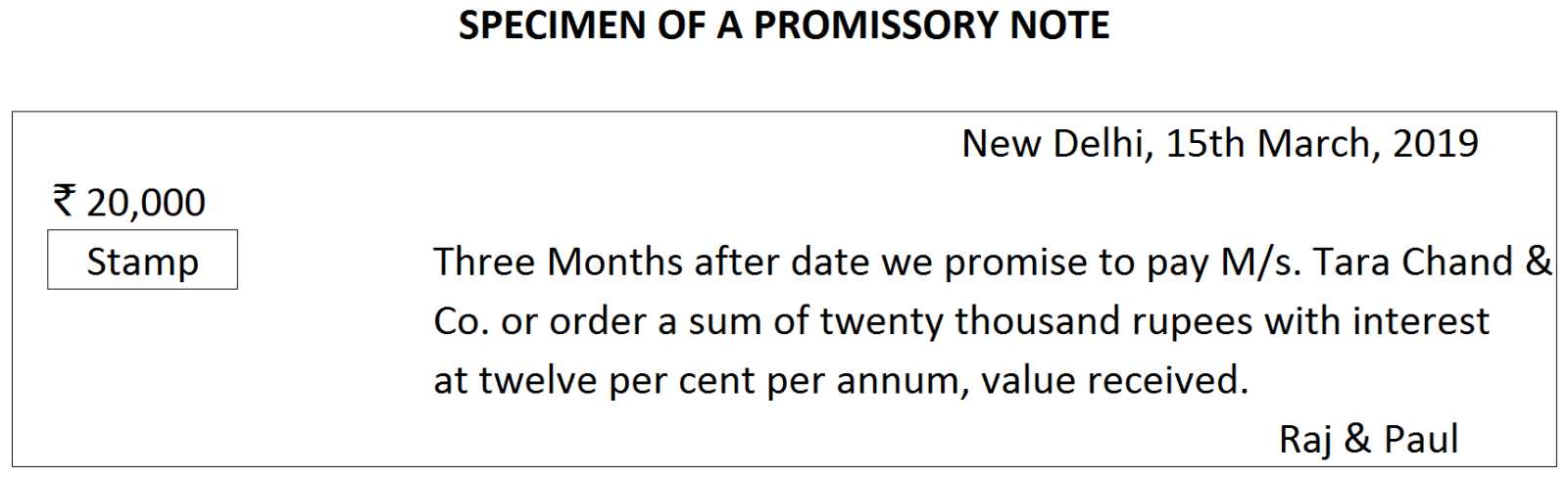

Prepare an imaginary specimen of a promissory note.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| 2019 | ₹ | |

| April 1 | Received for cash payment | 20,000 |

| April 2 | Paid for postage | 1,600 |

| April 5 | Paid for stationery | 1,000 |

| April 8 | Paid for advertisement | 2,000 |

| April 12 | Paid for wages | 800 |

| April 16 | Paid for carriage | 600 |

| April 20 | Paid for conveyance | 880 |

| April 25 | Paid for travelling expenses | 3,200 |

| April 27 | Paid for postage | 480 |

| April 28 | Paid for office cleaning | 400 |

| April 29 | Paid for courier | 800 |

| April 30 | Sent registered notice to landlord | 190 |