Question

What do you understand by Grouping of Accounts?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| ₹ | |

| Debtors as on 1st April, 2017 | 20,400 |

| Cash received from debtors during the year (as per Cash Book) | 60,800 |

| Returns Inward | 5,400 |

| Bad Debts | 2,400 |

| Debtors as on 31st March, 2018 | 27,600 |

| Cash Sales (as per Cash Book) | 56,800 |

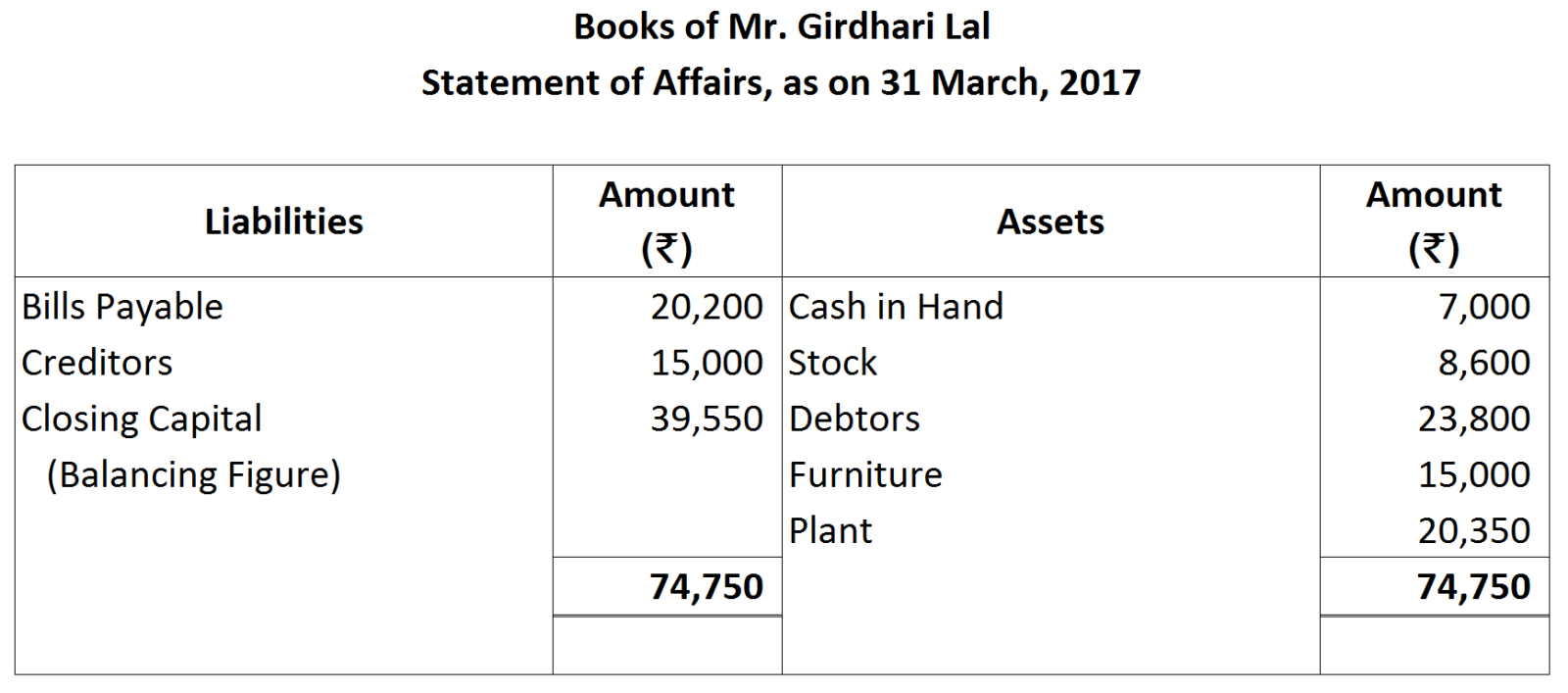

| ₹ | |

| Cash in hand | 7000 |

| Stock | 8,600 |

| Debtors | 23,800 |

| Furniture | 15,000 |

| Plant | 20,350 |

| Bills payable | 20,200 |

| Creditors | 15,000 |

| 2019 | |

| April 6 | Returned goods to Ramesh Brothers, Delhi purchased for ₹ 5,000 plus CGST and SGST @ 6% each |

| April 8 | Returned goods to Sohan Brothers, Meerut purchased for ₹ 10,000 plus IGST @ 12% |

| April 17 | Returned goods to Mahesh Brothers of ₹ 2,000 plus CGST and SGST @ 6% each |

|

2019

|

|

₹

|

||

|

March 1

|

Cash in Hand

|

12,750

|

||

|

|

Cash at Bank

|

72,400

|

||

|

March 4

|

Received from Asha cash ₹ 1,200 and a cheque for ₹ 3,200, allowed discount ₹ 400

|

|

||

|

March 7

|

Paid salary to staff by cheque

|

25,600

|

||

|

March 9

|

Withdrawn cash from bank for office use

|

21,900

|

||

|

March 12

|

Interest paid by bank on bank balance

|

1,200

|

||

|

March 16

|

Purchased furniture in cash

|

16,500

|

||

|

March 21

|

Paid Mohan & Co. by cheque, discount received ₹ 100

|

10,900

|

||

|

March 24

|

Proprietor withdrew from office cash for his personal use

|

11,600

|

||

|

March 29

|

Sold goods to Manoj for cash

|

14,800

|

||

|

March 31

|

Deposited office cash into bank

|

21,200

|

||

| ₹ | |

| Opening balance of debtors. | 1,80,000 |

| Opening balance of bills receivable. | 55,000 |

| Cash sales made during the year. | 95,000 |

| Credit sales made during the year. | 14,50,000 |

| Return inwards. | 78,000 |

| Cash received from debtors. | 10,25,000 |

| Discount allowed to debtors. | 55,000 |

| Bills receivable endorsed to creditors. | 60,000 |

| Cash received (bills matured). | 80,500 |

| Irrecoverable amount. | 10,000 |

| Closing balance of bills receivable on March 31, 2017. | 75,500 |