Question

What is Depreciation? What is the need for providing Depreciation?

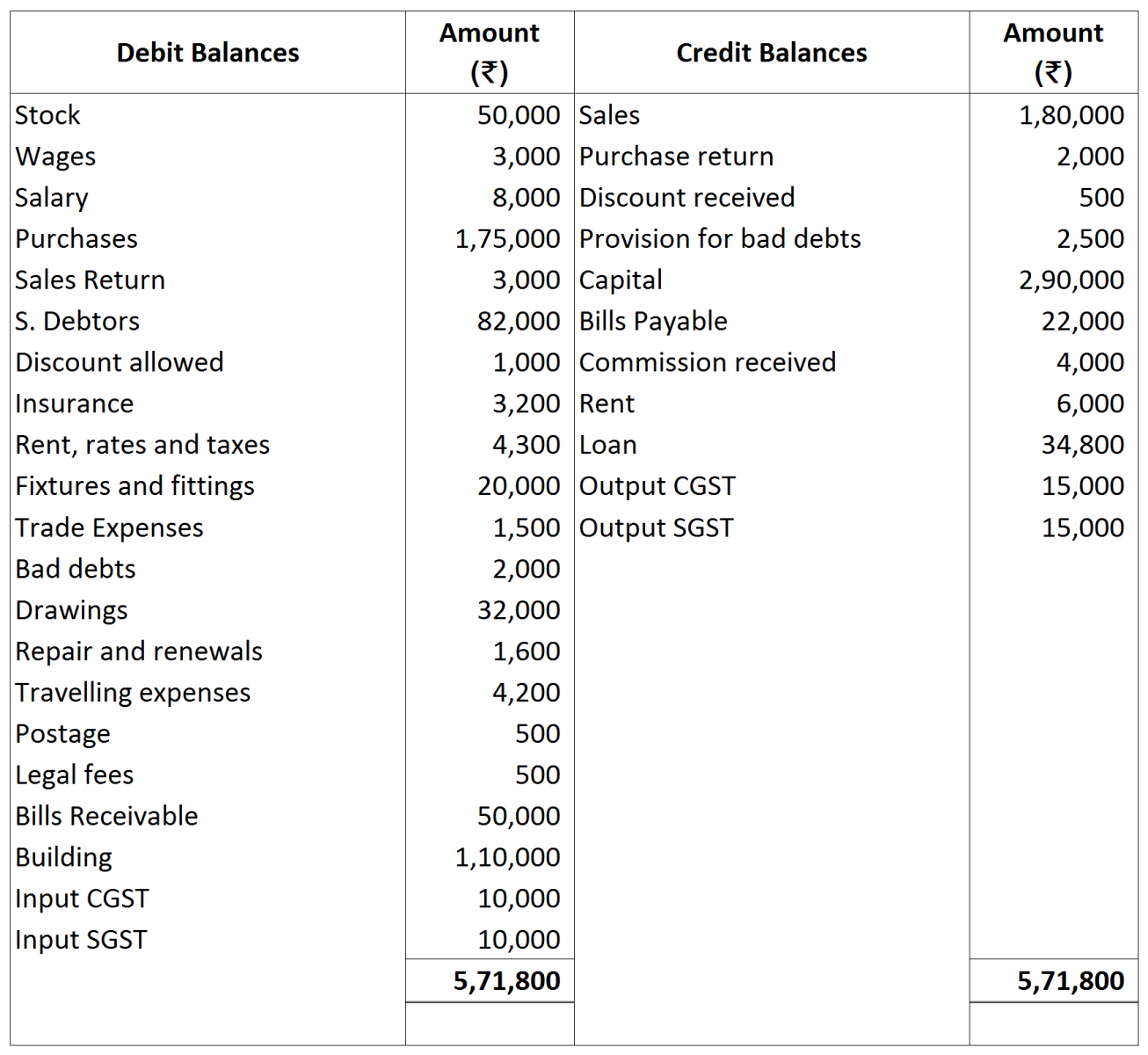

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

1st July, 2017

|

₹ 5,000

|

|

30th June, 2018

|

₹ 6,000

|

|

30th June, 2019

|

₹ 5,500

|

| 2019 | ₹ | |

| Jan. 1 | Opened a Bank Account and Deposited ........ | 12,500 |

| Purchased Goods against Cash Payment* ........ | 20,000 | |

| Purchased furniture for Shop* ........ | 5,000 | |

| Sold goods to R. Raman, Kolkata* ........ | 5,000 | |

| Jan. 2 | Bought goods from Man Mohan, Delhi** ........ | 10,000 |

| Jan. 3 | Bought stationery and paid by cash ........ | 1,000 |

| Jan. 5 | Received cash from R. Raman ........ | 5,300 |

| Discount allowed to him ........ | 300 | |

| Jan. 6 | Sold goods to Bimal, Kolkata* ........ | 7,500 |

| Jan. 8 | Bimal returned part of the goods supplied on the 6th instant ........ | 1,500 |

| Jan. 10 | Paid cash into bank ........ | 1,000 |

| Jan. 12 | Paid wages ........ | 1,500 |

| Jan. 13 | Bought on credit from the Union Furniture Co., Kolkata office desk* ........ | 1,500 |

| Jan. 19 | Paid wages ........ | 1,500 |

| Jan. 21 | Paid to Man Mohan by cheque ........ | 10,700 |

| Discount received ........ | 500 | |

| Jan. 21 | Sold goods to Ramesh, Guwahati including IGST** ........ | 6,720 |

| Jan. 22 | Received cheque from Bimal ........ | 6,000 |

| Jan. 23 | Bought goods from Man Mohan, Delhi** ........ | 7,000 |

| Jan. 24 | Drew by cheque for personal use ........ | 2,000 |

| Jan. 27 | Paid wages ........ | 1,500 |

| Jan. 31 | Rent due to landlord* ........ | 1,000 |