Question 16 Marks

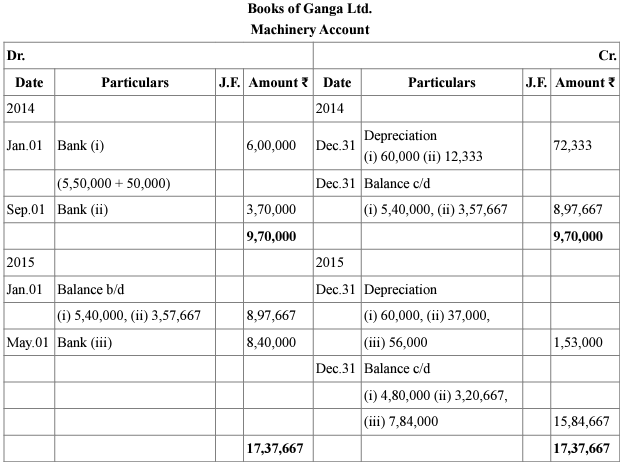

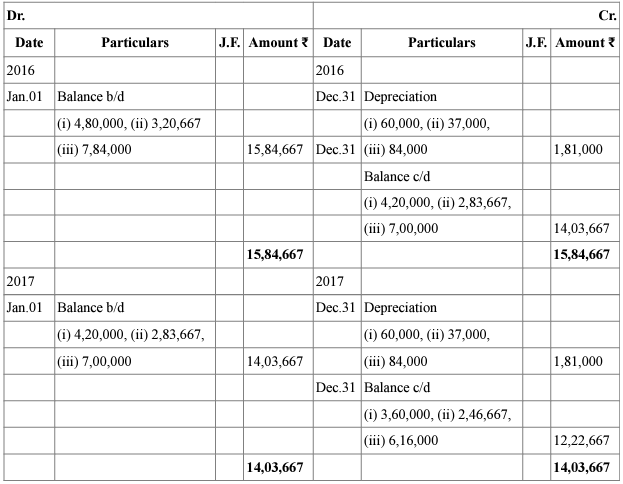

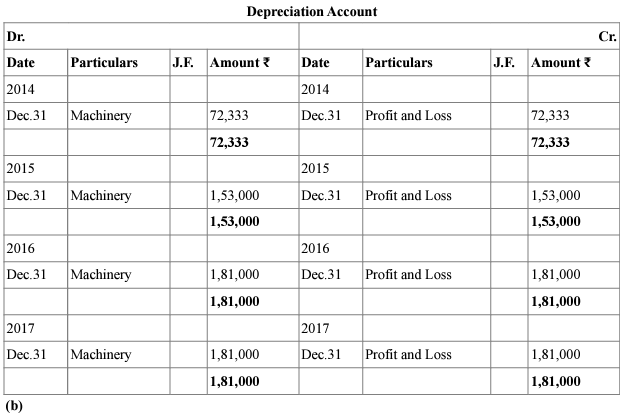

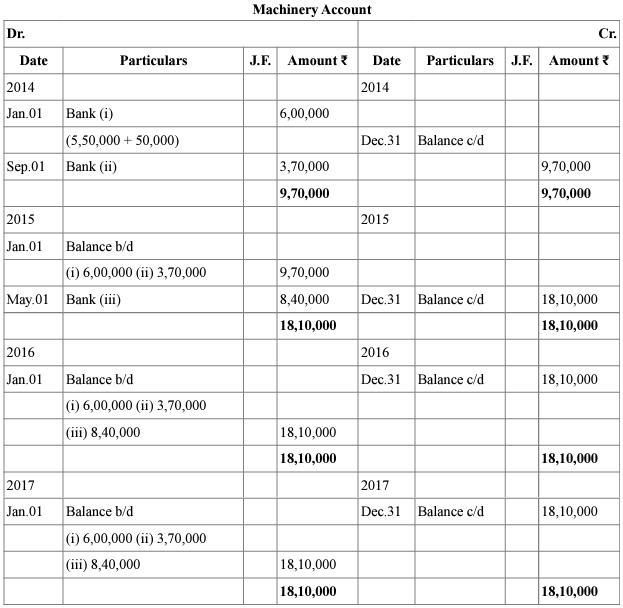

Ganga Ltd. purchased a machinery on January 01,2014 for ₹ $5,50,000$ and spent ₹ 50,000 on its installation. On September 01, 2014 it purchased another machine for ₹ $3,70,000$. On May 01,2015 it purchased another machine for $₹ 8,40,000$ (including installation expenses). Depreciation was provided on machinery @10\% p.a. on original cost method annually on December 31. Prepare:

i. Machinery account and depreciation account for the years 2014, 2015, 2016 and 2017.

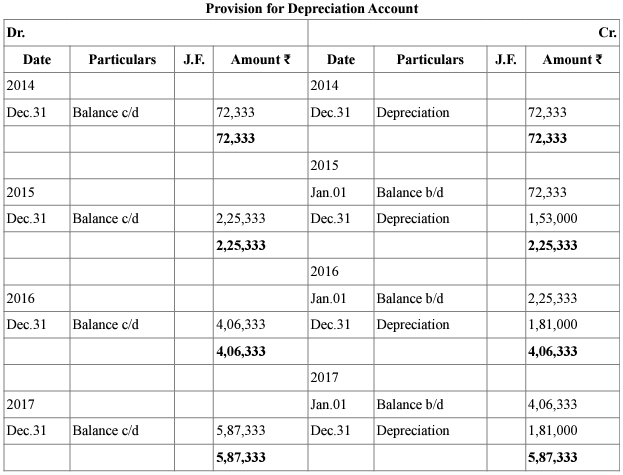

ii. If depreciation is accumulated in provision for Depreciation account then prepare machine account and provision for depreciation account for the years 2014, 2015,2016 and 2017.

View full question & answer→i. Machinery account and depreciation account for the years 2014, 2015, 2016 and 2017.

ii. If depreciation is accumulated in provision for Depreciation account then prepare machine account and provision for depreciation account for the years 2014, 2015,2016 and 2017.