MCQ 11 Mark

At a price below the equilibrium price, there is:

- AExcess supply.

- ✓Excess demand.

- CCeiling.

- DFlooring.

Answer

View full question & answer→Correct option: B.

Excess demand.

50 questions · timed · auto-graded

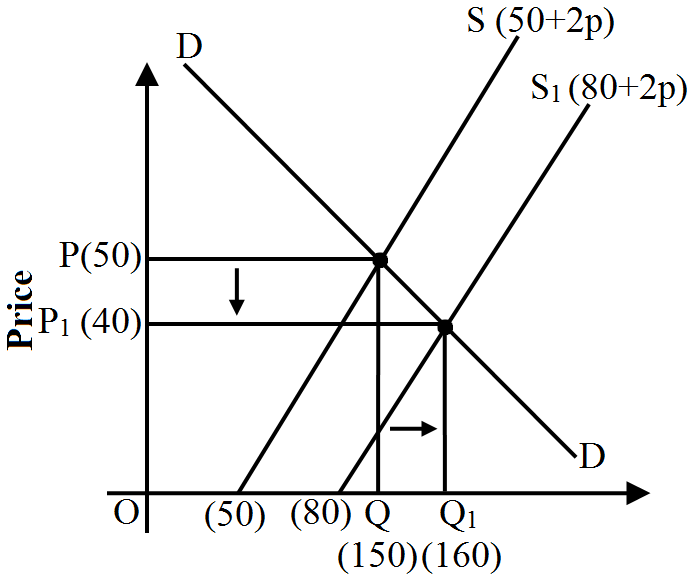

Demand curve remain unchanged, if there is a decrease in supply, supply curve and equilibrium point will shift leftwards. As a result, equilibrium price will increase and equilibrium quantity will decrease

Both $AR$ and $MR$ curves are downward sloping under monopolistic competition because a firm can sell more commodity by lowering the price. The $MR$ curve is half of $AR$ curve, i.e. $AR > MR.$