Question 14 Marks

State giving reasons, which of the following transactions would improve, reduce or not change the Current Ratio, if Current Ratio of a company is 0.8 : 1:

- Cash paid to Trade Payables.

- Purchase of Stock-in-Trade on credit.

- Purchase of Stock-in-Trade for cash.

- Payment of Dividend payable.

- Bills Payable discharged.

- Bills Receivable endorsed to a creditor.

- Bills Receivable endorsed to a creditor dishonoured.

Answer

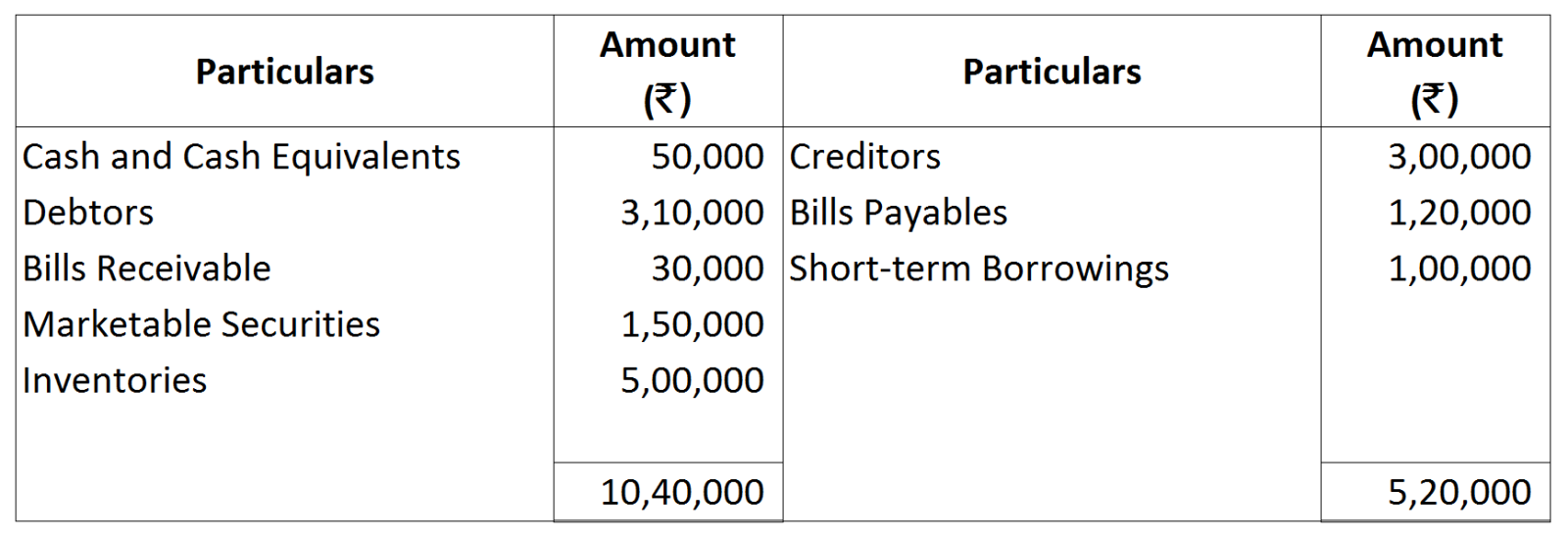

Current Ratio $=\frac{80,000}{1,00,000}=0.8:1$

View full question & answer→- Let’s assume Current Assets as ₹ 80,000 and Current Liabilities as ₹ 1,00,000

Current Ratio $=\frac{80,000}{1,00,000}=0.8:1$

- Cash paid to Trade Payables (say ₹ 50,000)

- Purchase of Stock-in-Trade for cash (say ₹ 50,000)

- Purchase of Stock-in-Trade for cash (say ₹ 50,000)

- Payment of Dividend (say ₹ 50,000)

- Bills Payable discharged (say ₹ 50,000)

- Bills Receivable endorsed to a Creditor (say ₹ 50,000)

- Bills Receivable endorsed to a Creditor dishonoured (say ₹ 50,000)