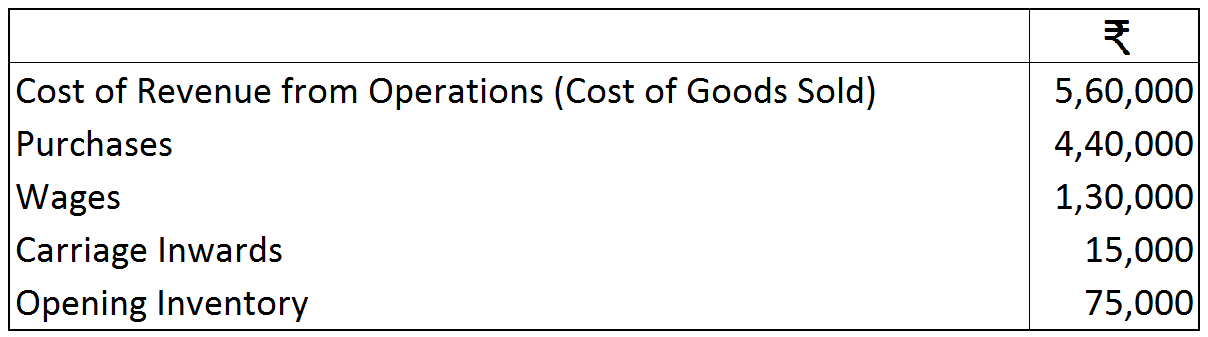

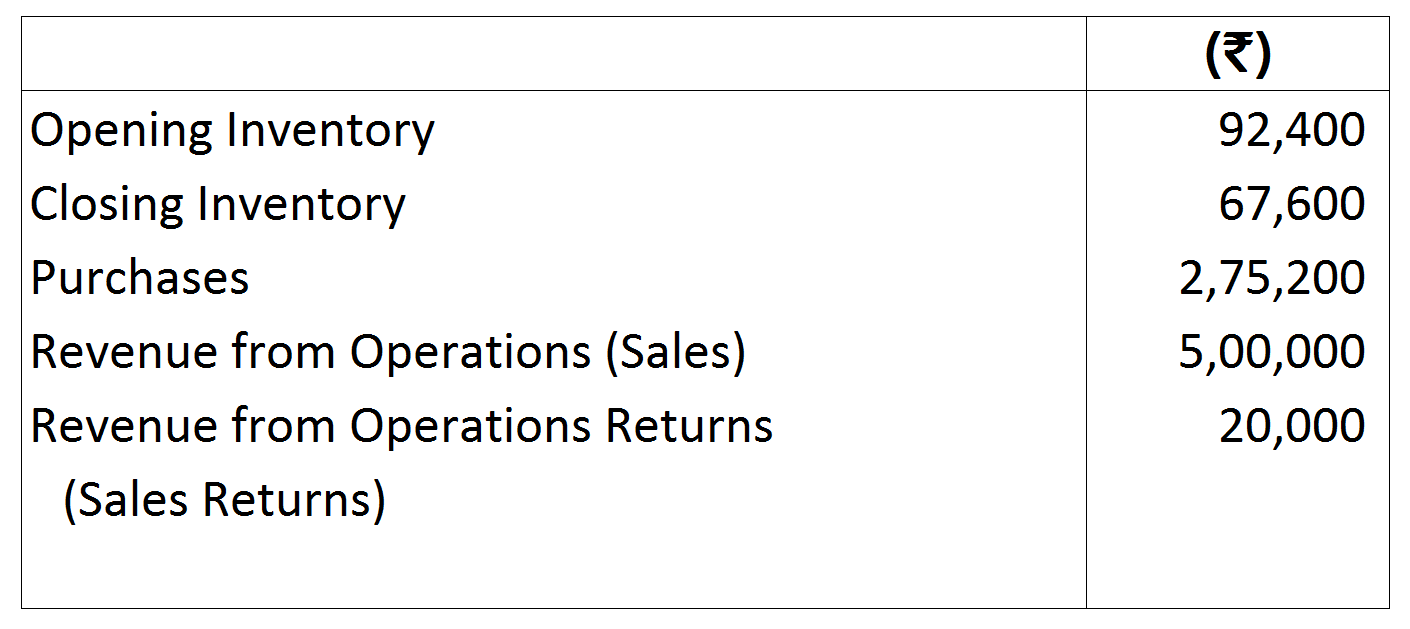

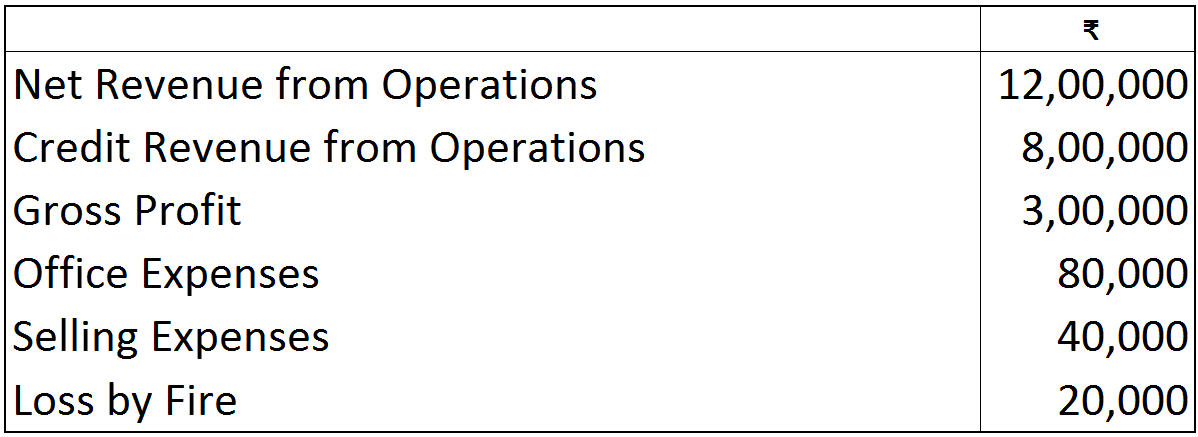

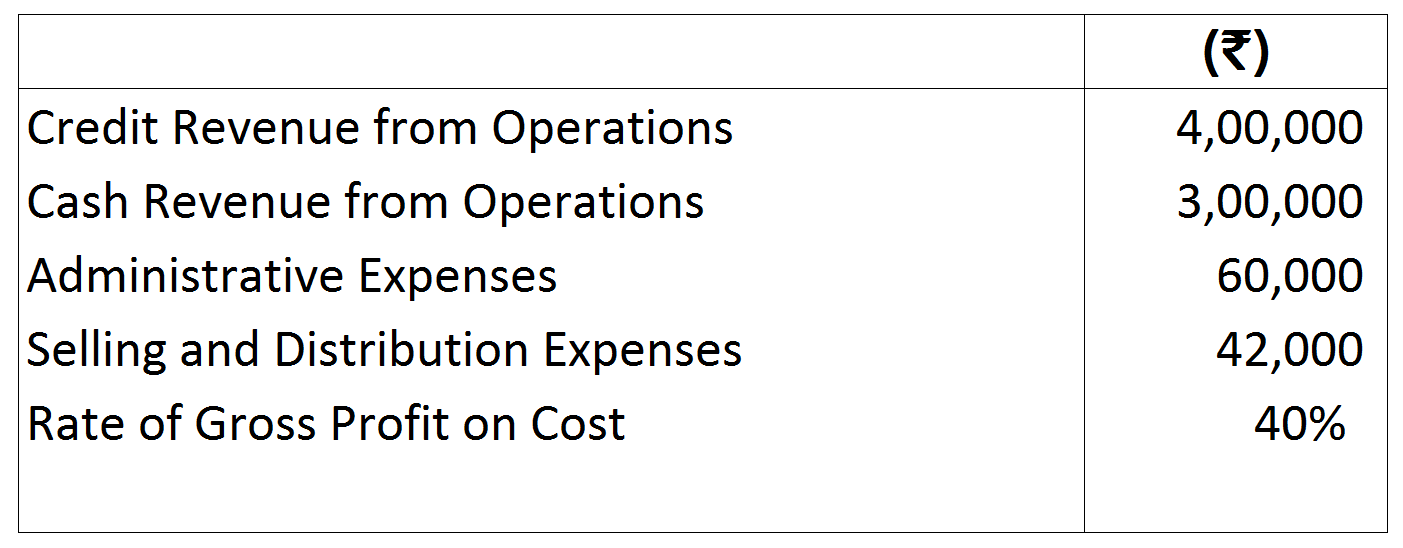

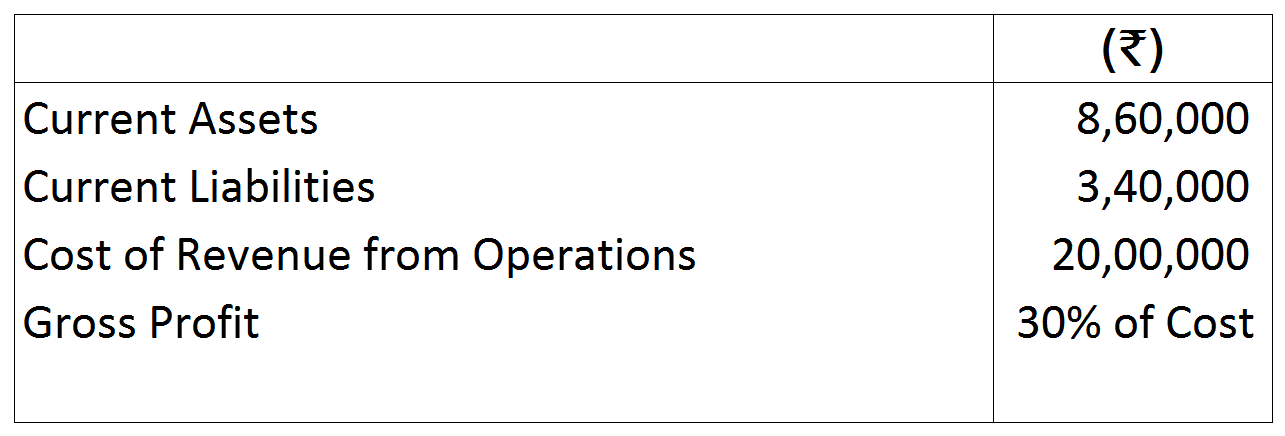

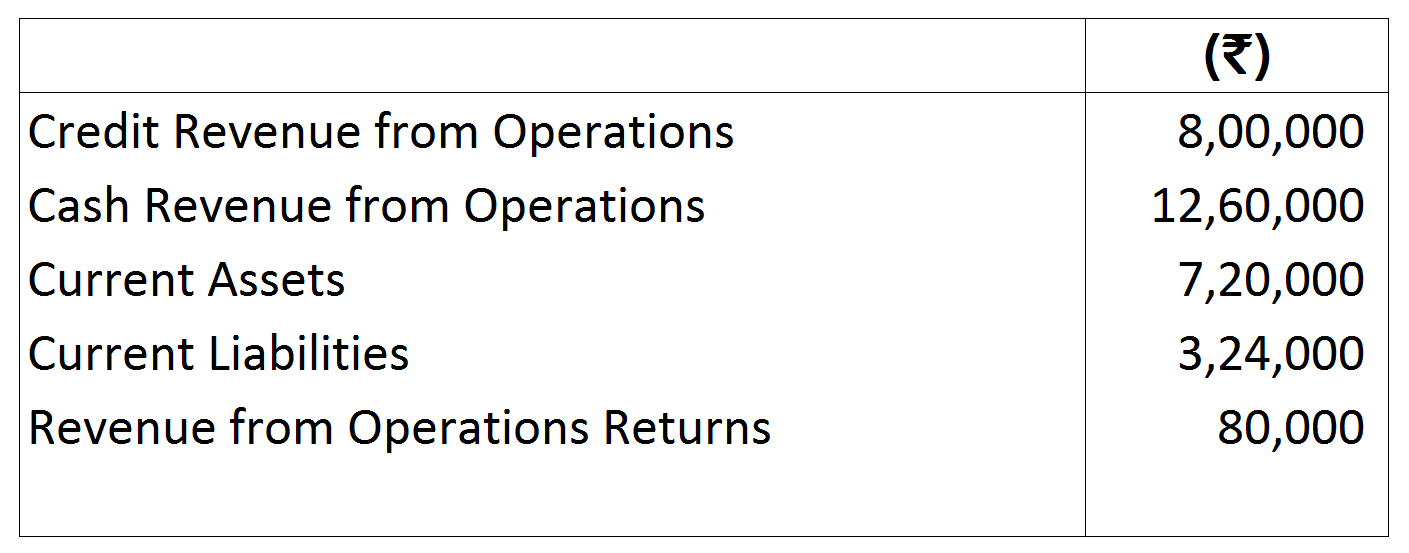

Question 13 Marks

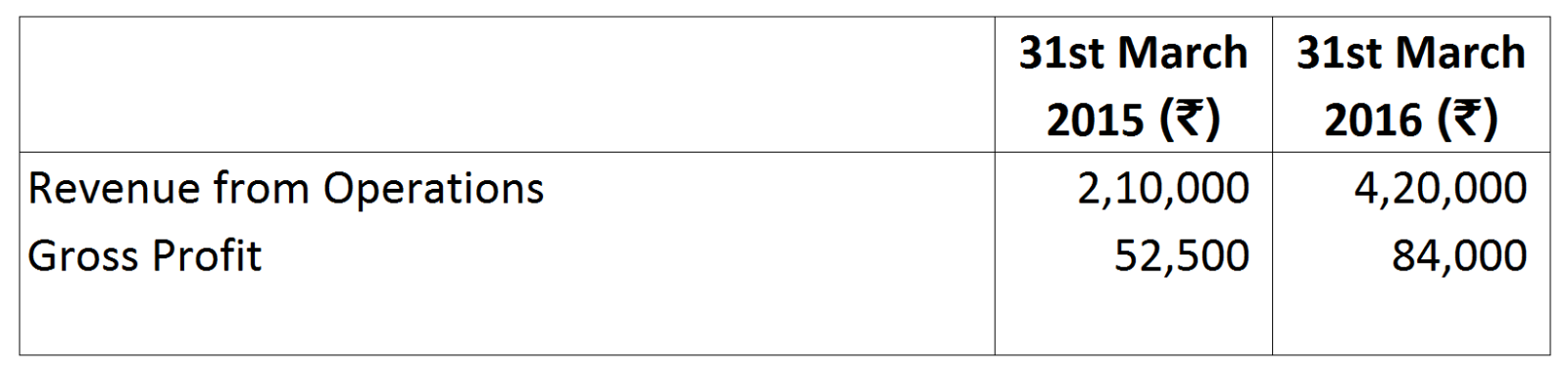

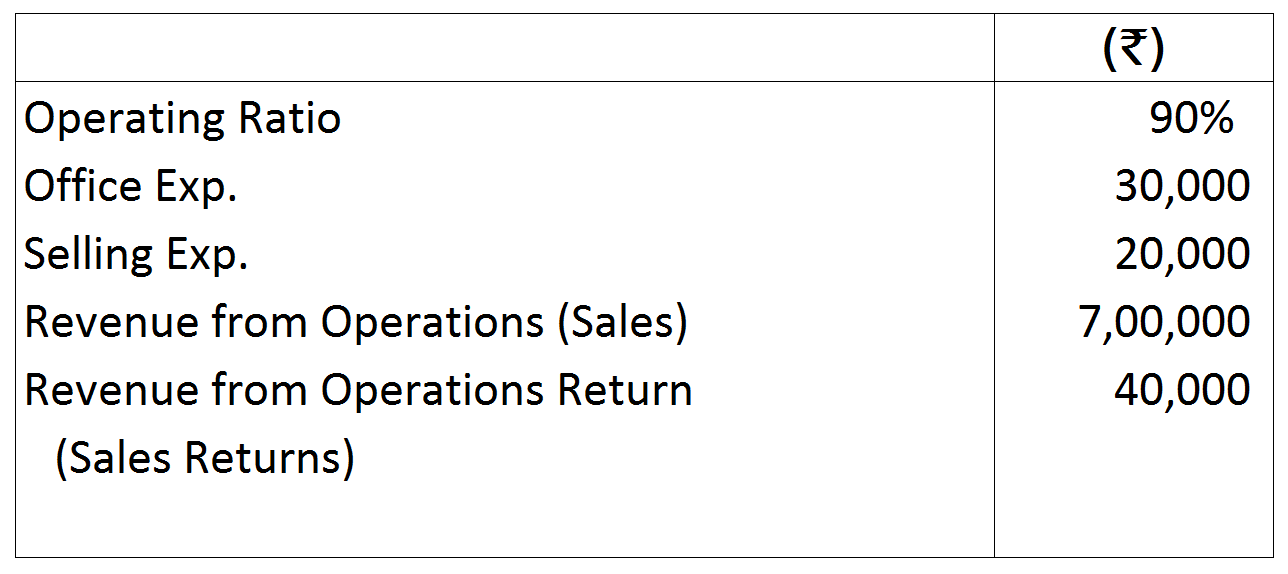

Calculate Cost of Goods Sold from the following information:

Answer

View full question & answer→Net Revenue from Operations = Revenue from Operations - Revenue from Operations Return

= ₹ 7,00,000 - ₹ 40,000 = ₹ 6,60,000

Operating Ratio $=\frac{\text{Cost of Revenue from Operations + Operating Expenses}}{\text{Net Revenue from Operations}}\times100$

Hence, Cost of Revenue from Operations + Operating Expenses = 90% of Net Revenue from Operations

= ₹ 7,00,000 - ₹ 40,000 = ₹ 6,60,000

Operating Ratio $=\frac{\text{Cost of Revenue from Operations + Operating Expenses}}{\text{Net Revenue from Operations}}\times100$

Hence, Cost of Revenue from Operations + Operating Expenses = 90% of Net Revenue from Operations

| Cost of Revenue from Operations+ ₹ 30,000 + ₹ 20,000 | = | 90% of ₹ 6,60,000 |

| Cost of Revenue from Operations+ ₹ 50,000 | = | ₹ 5,94,000 |

| Cost of Revenue from Operations | = | ₹ 5,94,000 - ₹ 50,000 |

| = | ₹ 5,44,000 |

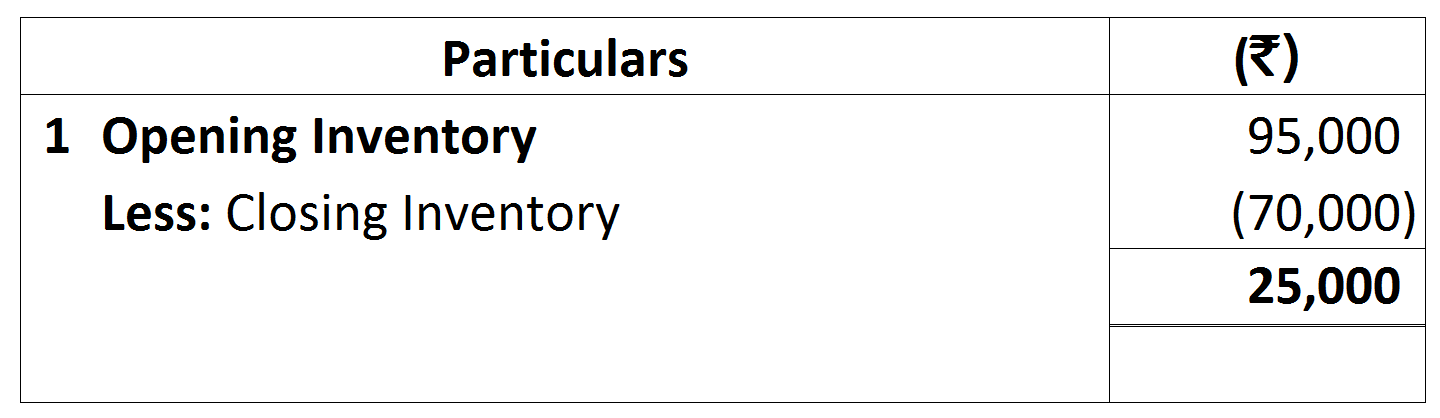

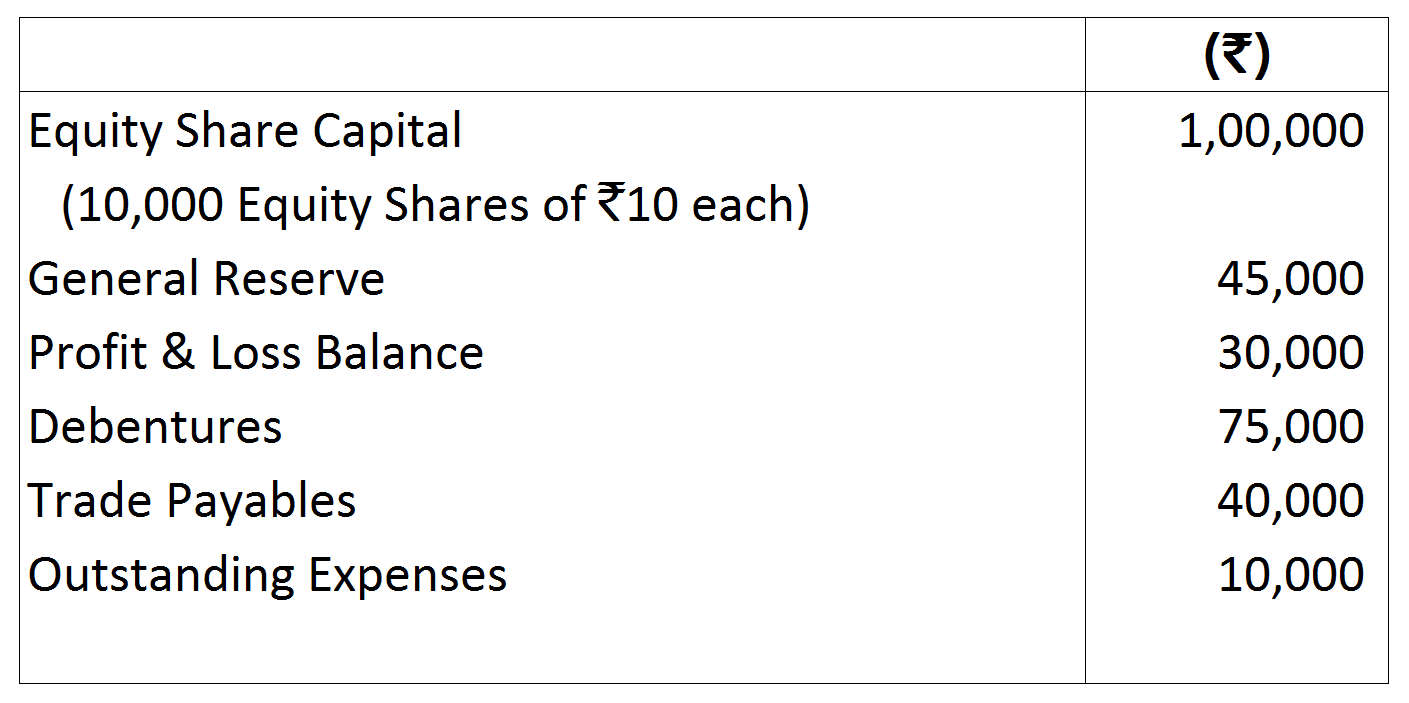

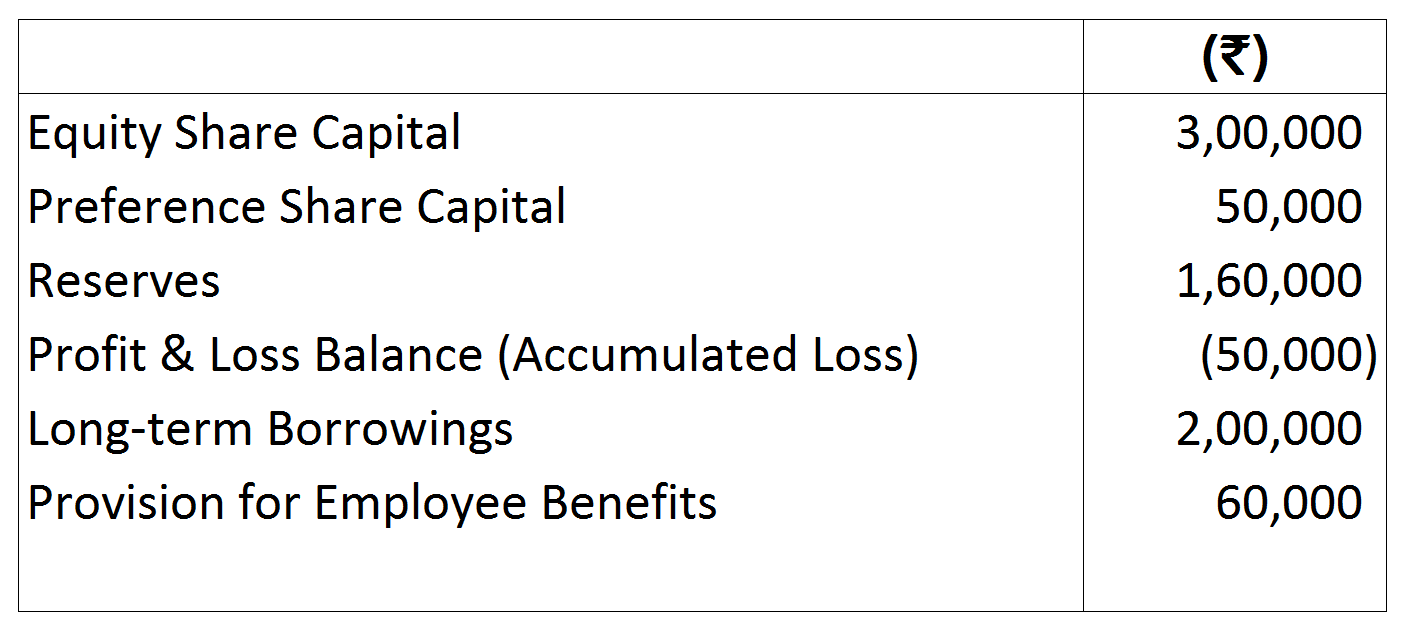

Notes to Accounts:

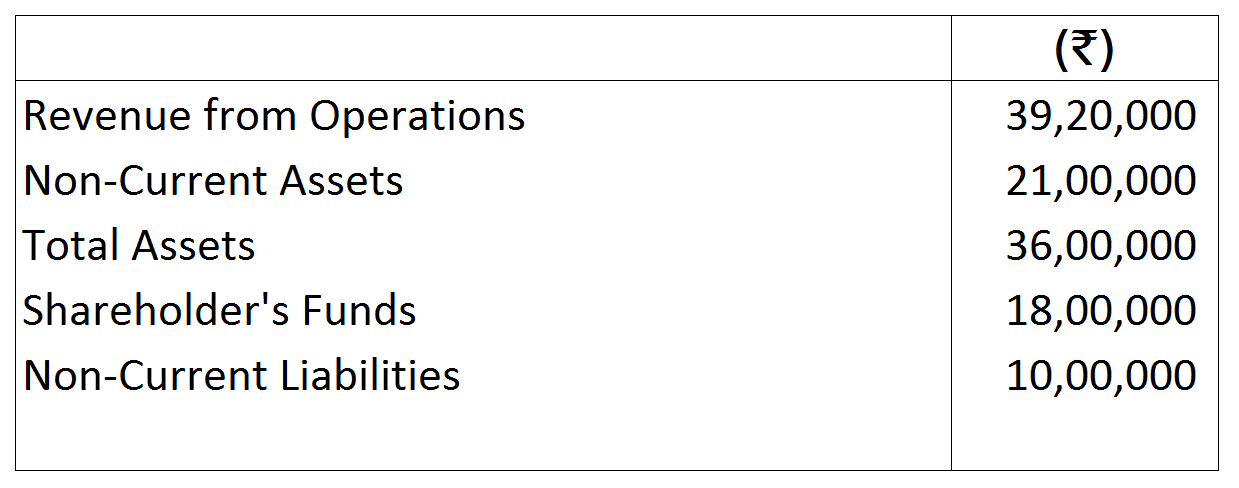

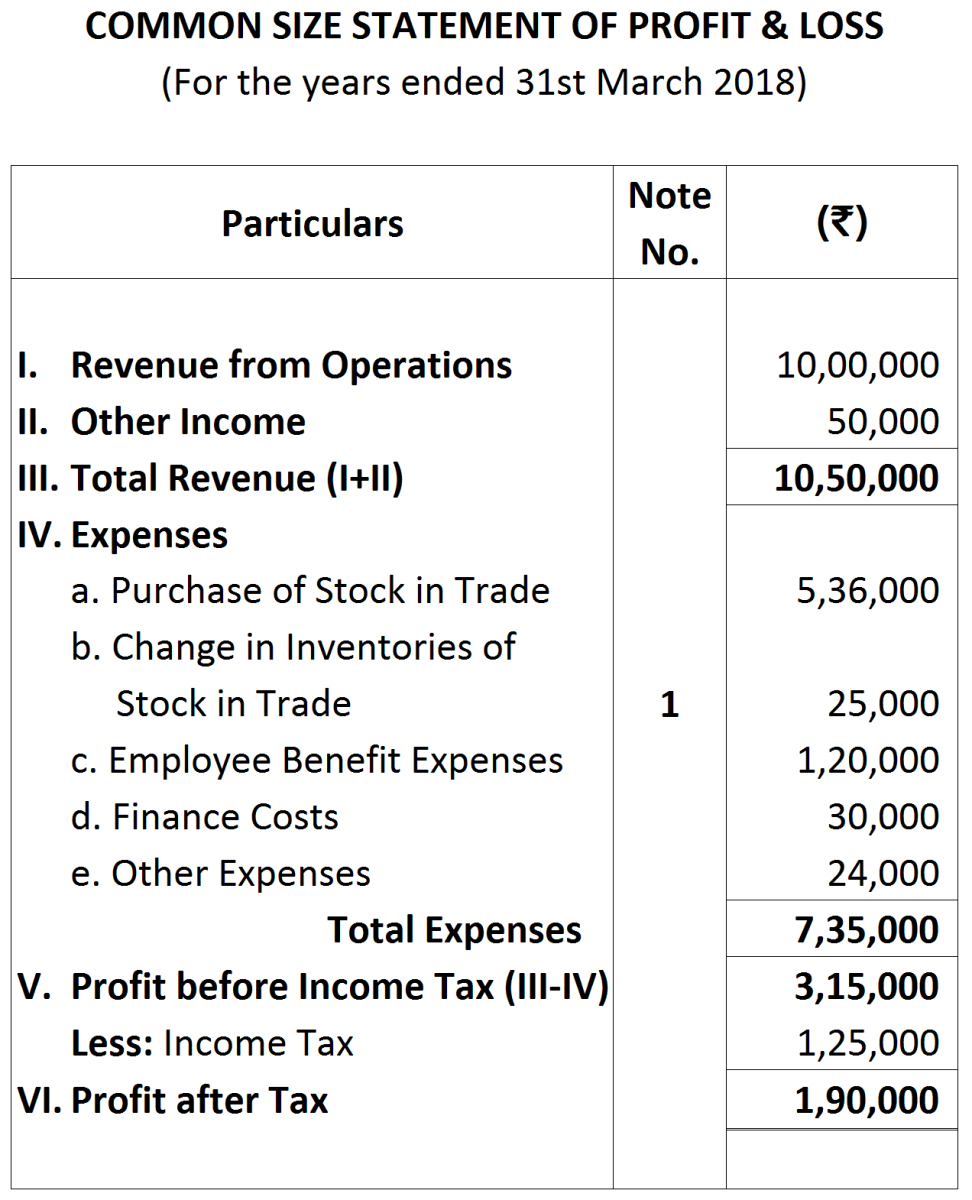

Notes to Accounts: