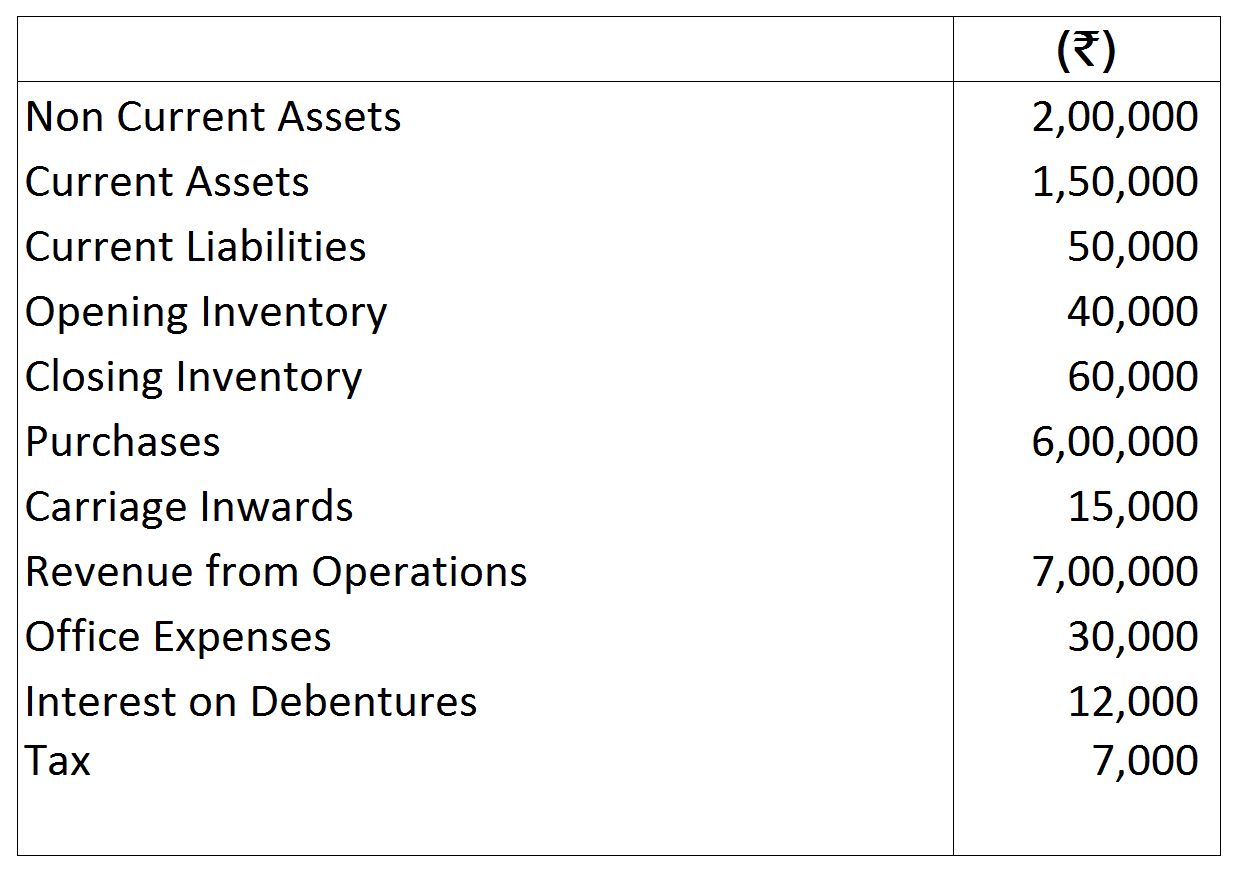

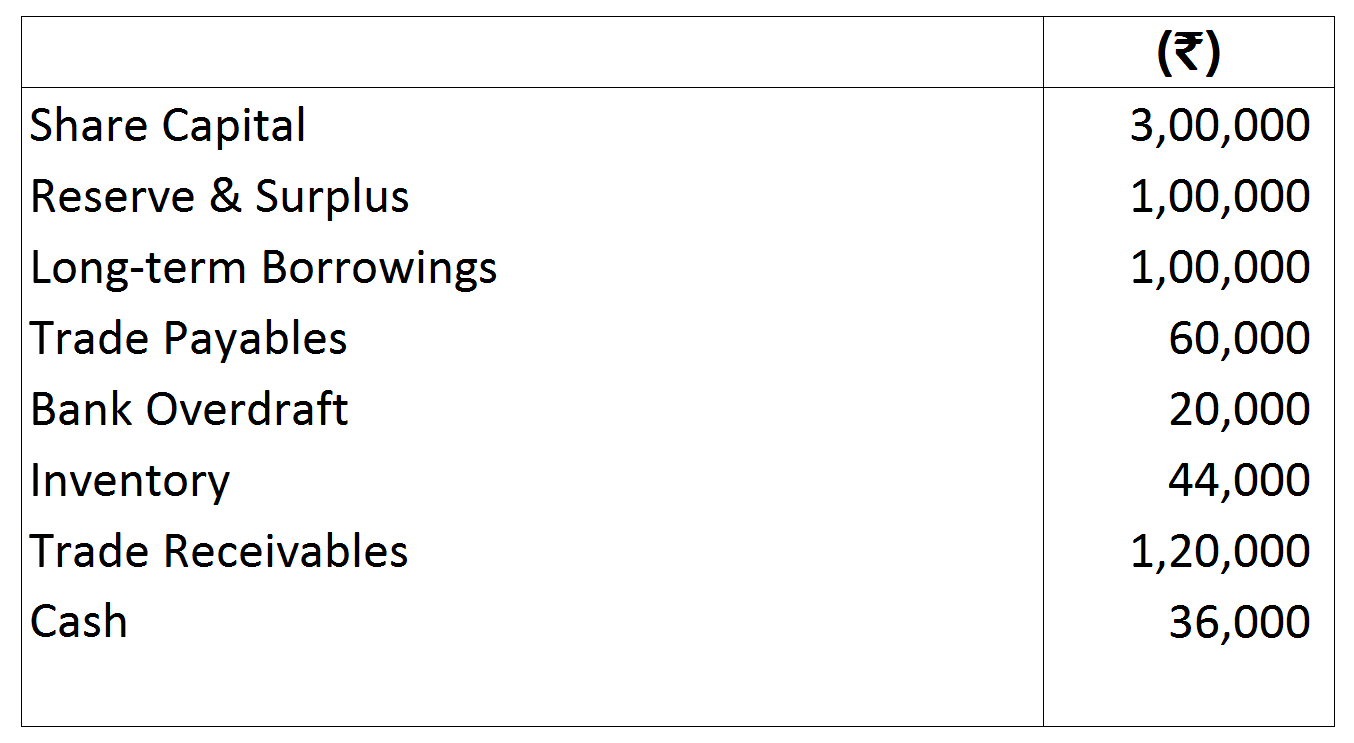

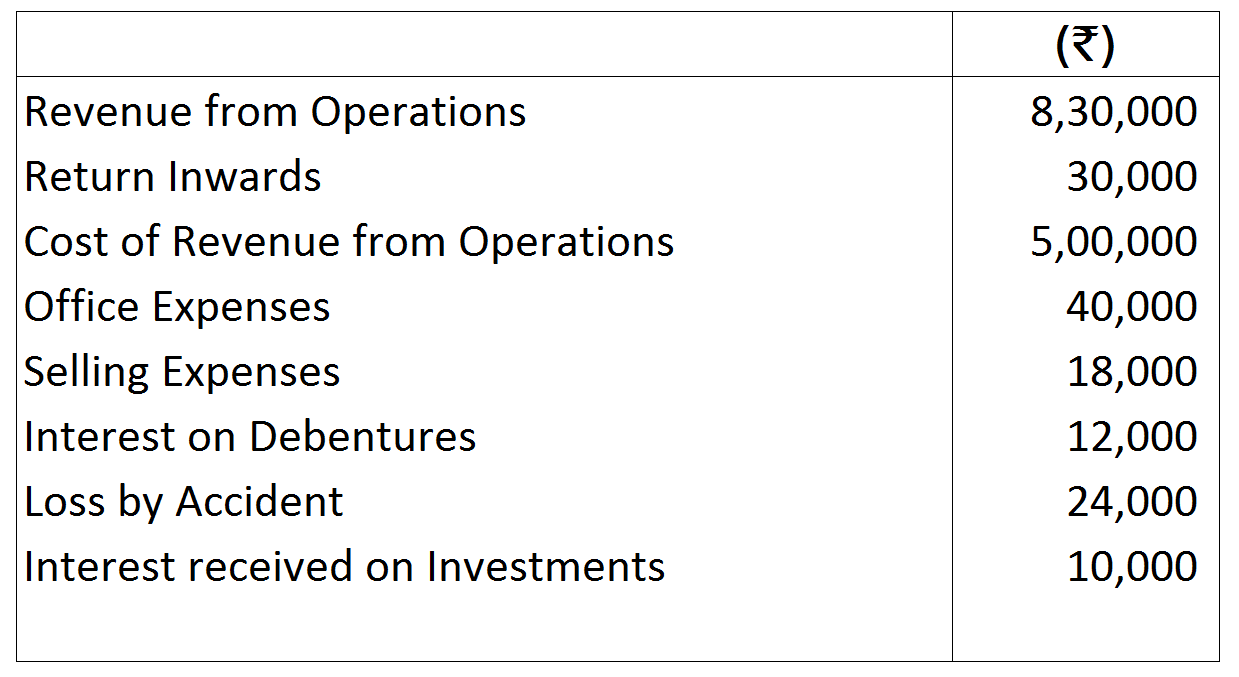

Question 16 Marks

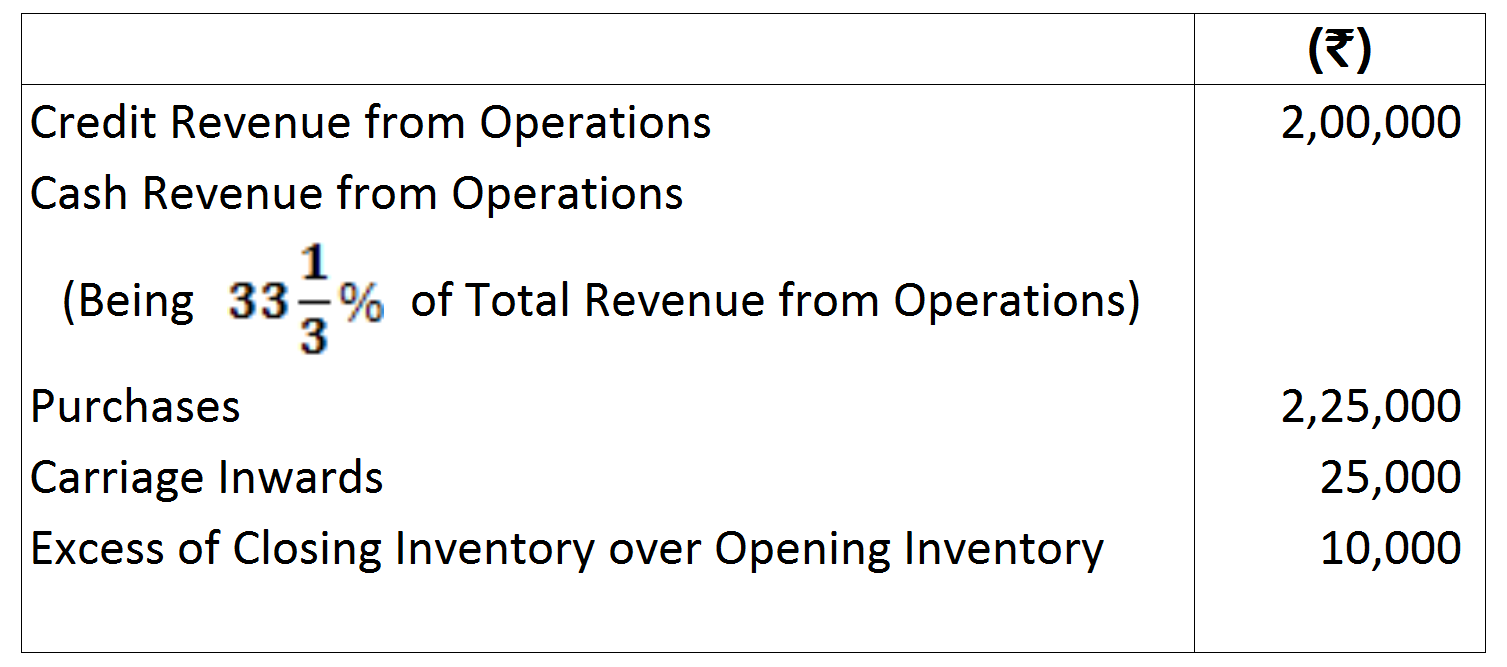

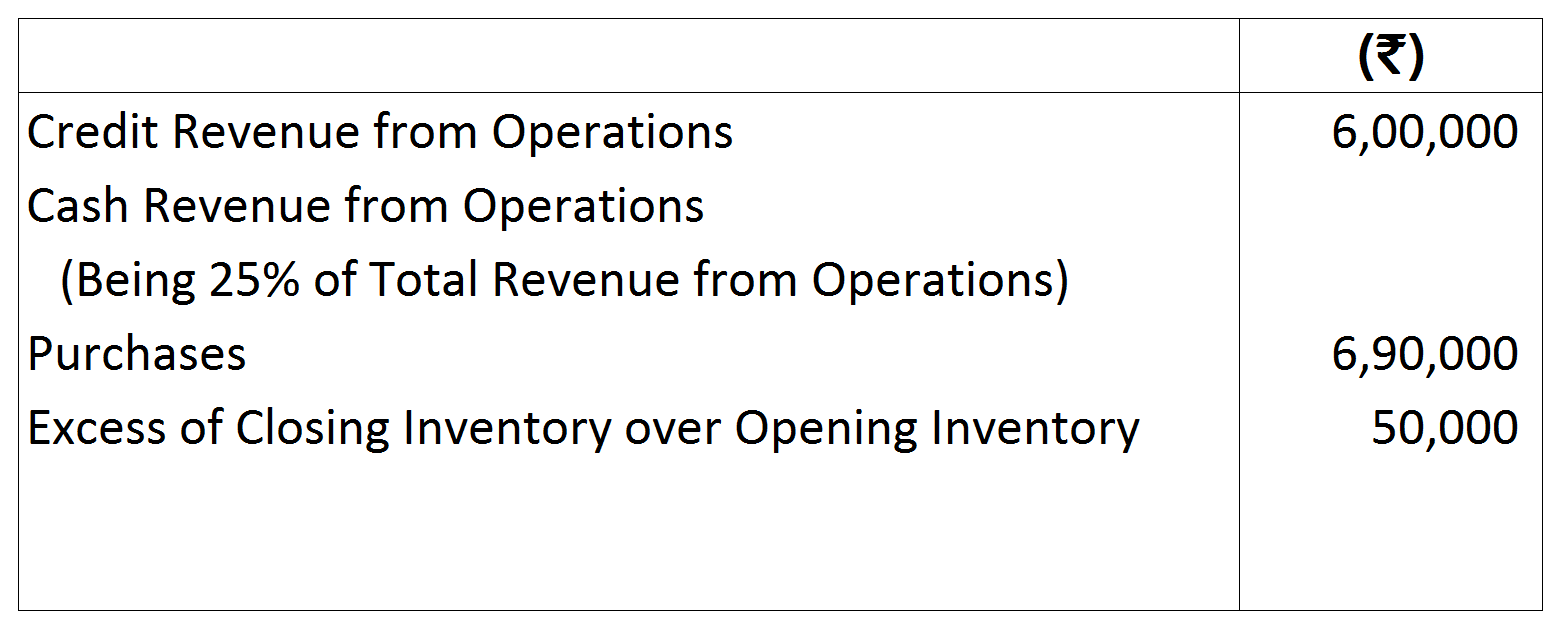

Calculate Gross Profit Ratio from the following data:

Answer

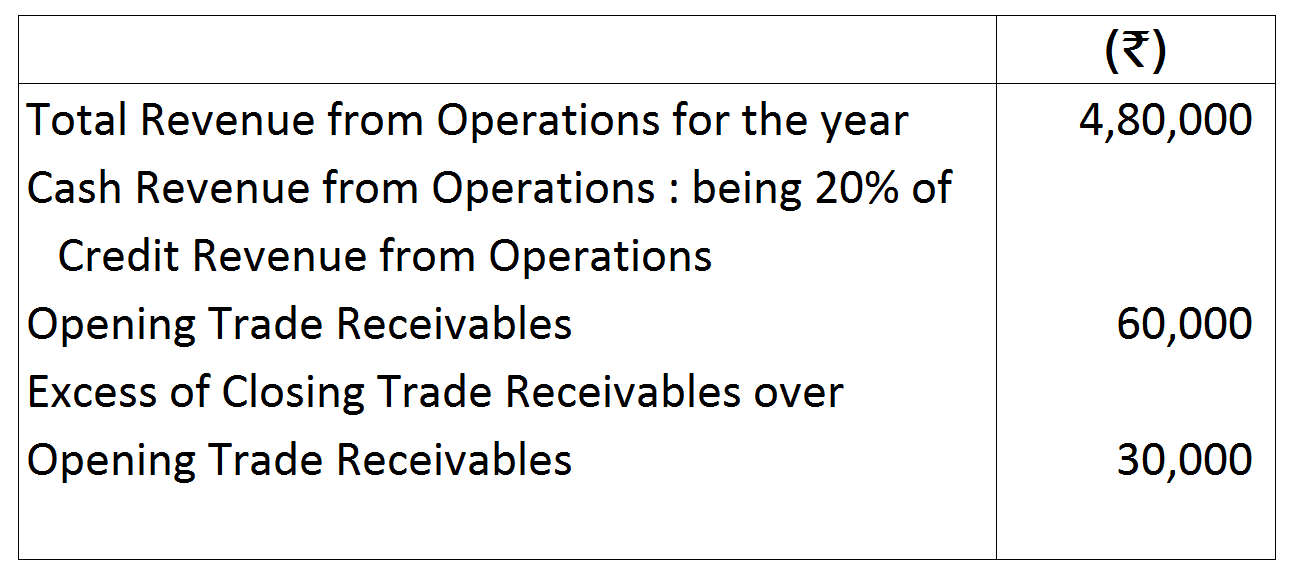

View full question & answer→If Total Revenue from Operations is ₹ 100, Cash Revenue from Operations will be $₹\ 33 \frac{1}{3}$ and Credit Revenue from Operations $₹\ 66 \frac{2}{3}$

Hence,

If Credit Revenue from Operations is $₹\ 66 \frac{2}{3}$ Total Revenue from Operations will be= ₹ 100

If Credit Revenue from Operations is ₹ 2,00,000

Total Revenue from Operations will be $=\frac{100}{66\frac{2}{3}}\times ₹\ 2,00,000$

$=100\times\frac{2}{200}\times ₹\ 2,00,000$

$=₹\ 3,00,000$

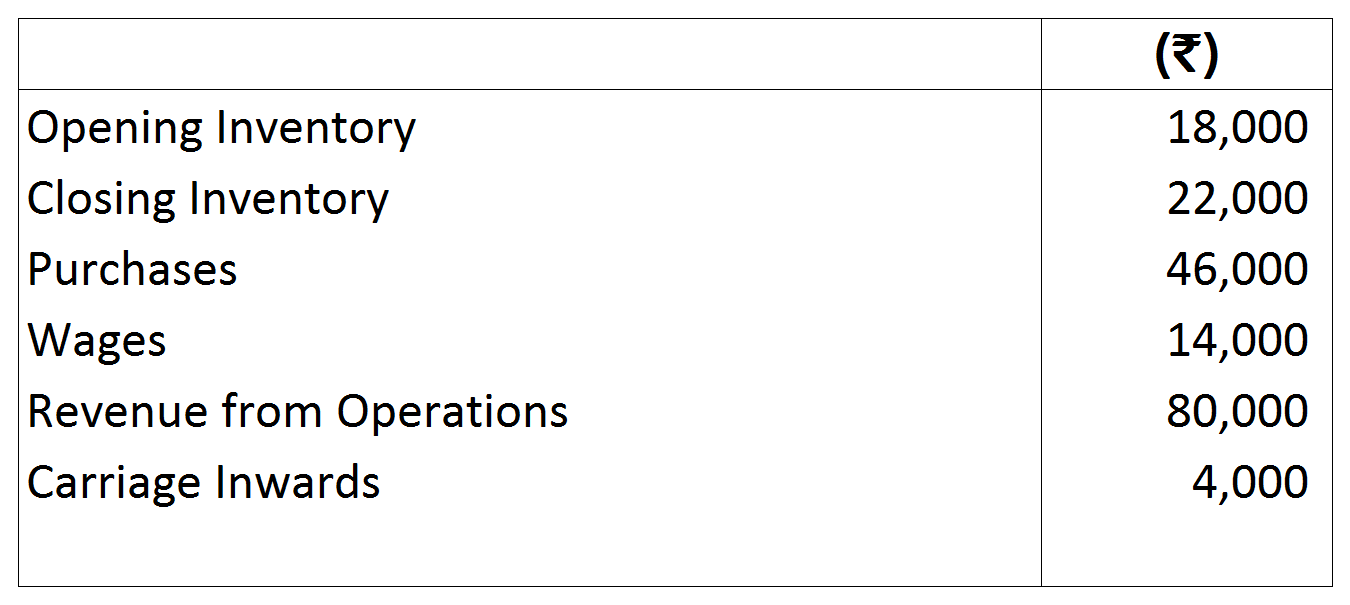

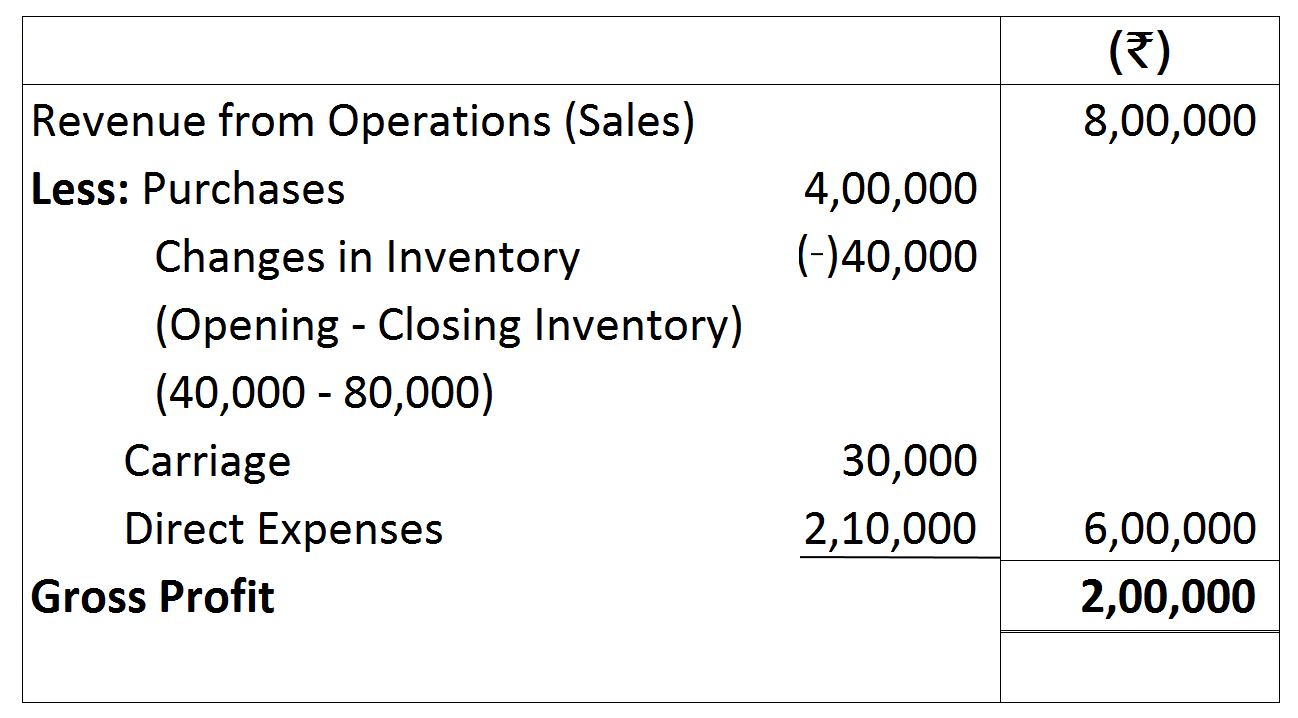

Cost of Revenue from Operations = Purchases + Carriage Inwards - Excess of Closing Inventory over Opening Inventory

= ₹ 2,25,000 + ₹ 25,000 - ₹ 10,000

= ₹ 2,40,000

Gross Profit = Total Revenue from Operations - Cost of Revenue from Operations

= ₹ 3,00,000 - ₹ 2,40,000 = ₹ 60,000

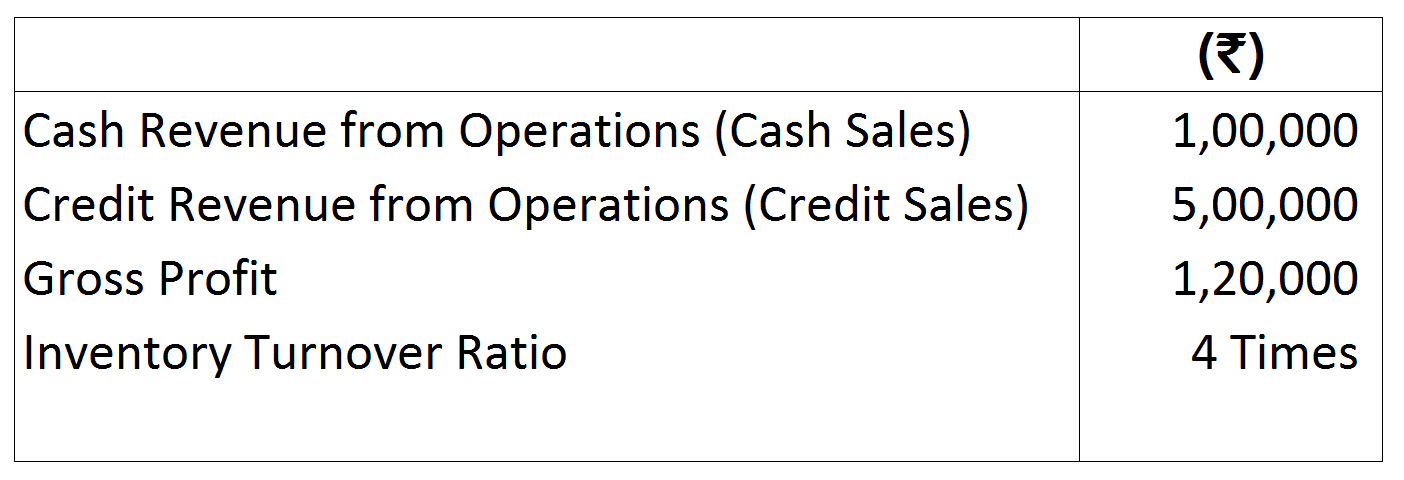

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations x}}\times100$

$=\frac{₹\ 60,000}{₹\ 3,00,000}\times100= 20 \%$

Hence,

If Credit Revenue from Operations is $₹\ 66 \frac{2}{3}$ Total Revenue from Operations will be= ₹ 100

If Credit Revenue from Operations is ₹ 2,00,000

Total Revenue from Operations will be $=\frac{100}{66\frac{2}{3}}\times ₹\ 2,00,000$

$=100\times\frac{2}{200}\times ₹\ 2,00,000$

$=₹\ 3,00,000$

Cost of Revenue from Operations = Purchases + Carriage Inwards - Excess of Closing Inventory over Opening Inventory

= ₹ 2,25,000 + ₹ 25,000 - ₹ 10,000

= ₹ 2,40,000

Gross Profit = Total Revenue from Operations - Cost of Revenue from Operations

= ₹ 3,00,000 - ₹ 2,40,000 = ₹ 60,000

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations x}}\times100$

$=\frac{₹\ 60,000}{₹\ 3,00,000}\times100= 20 \%$

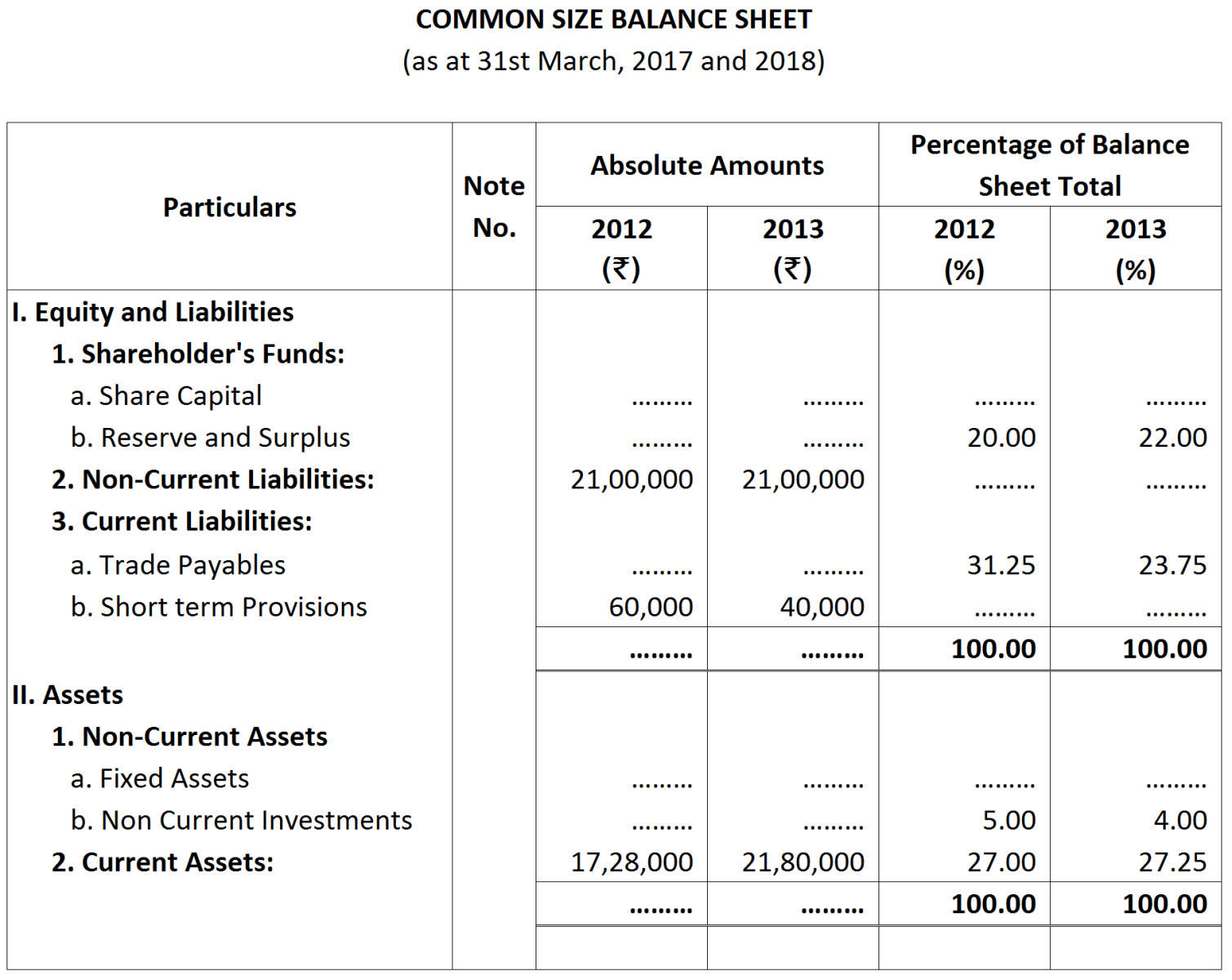

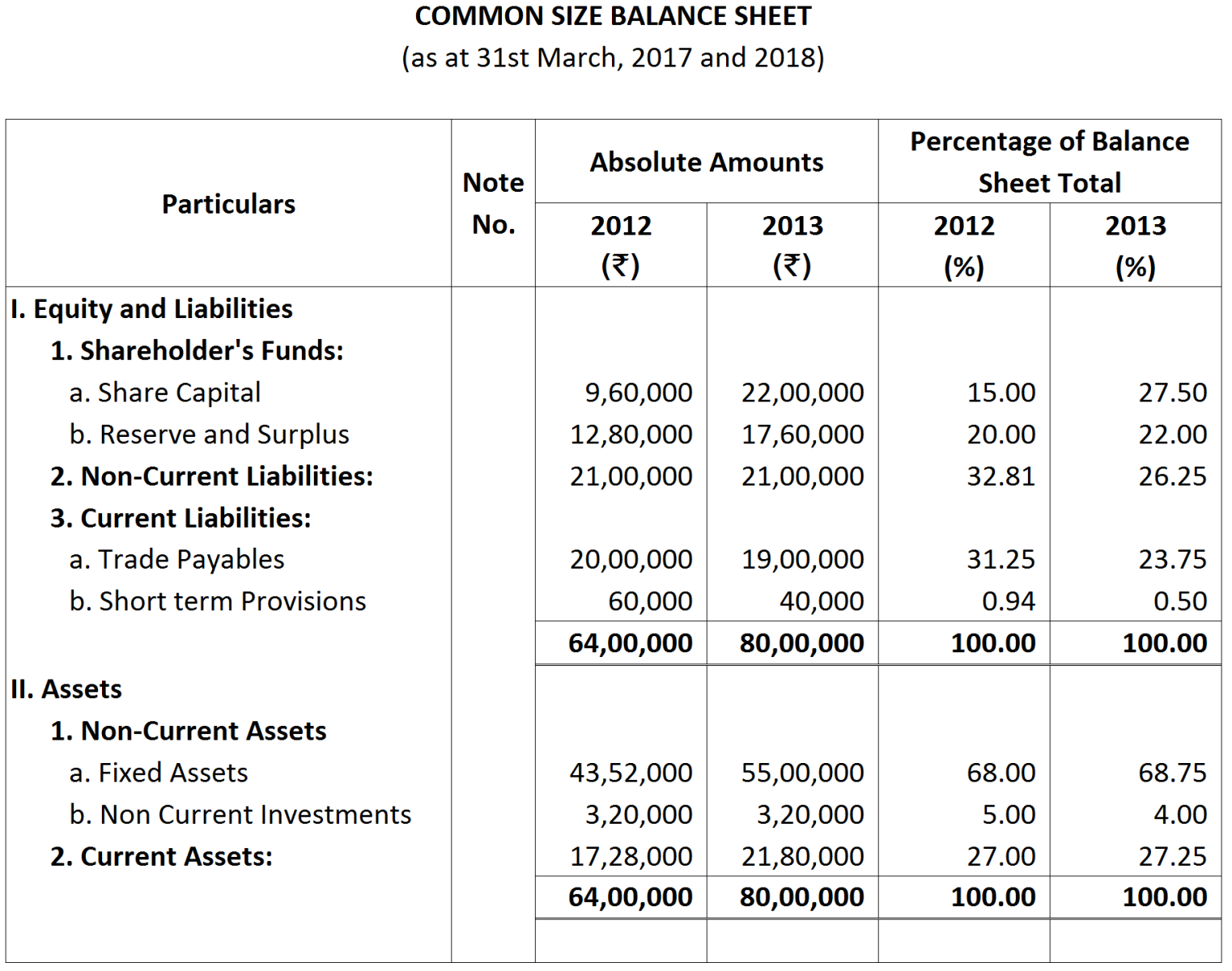

Note:

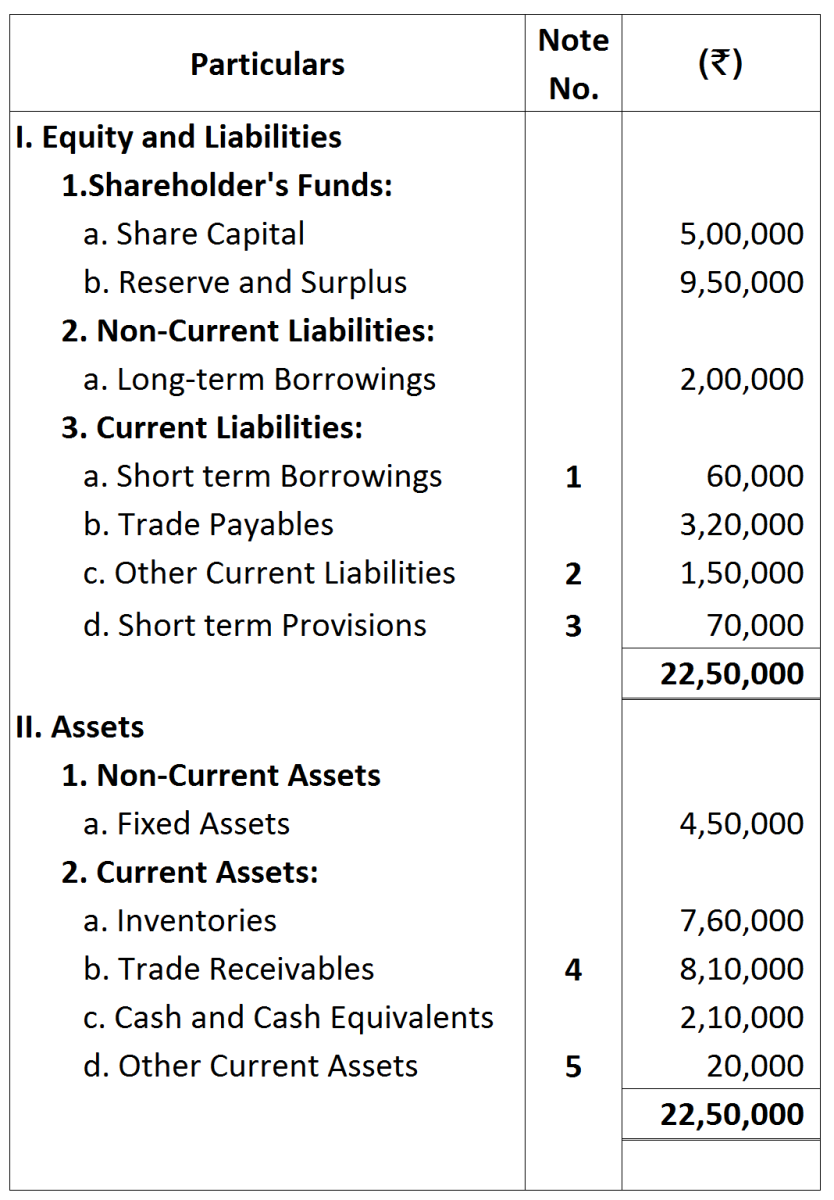

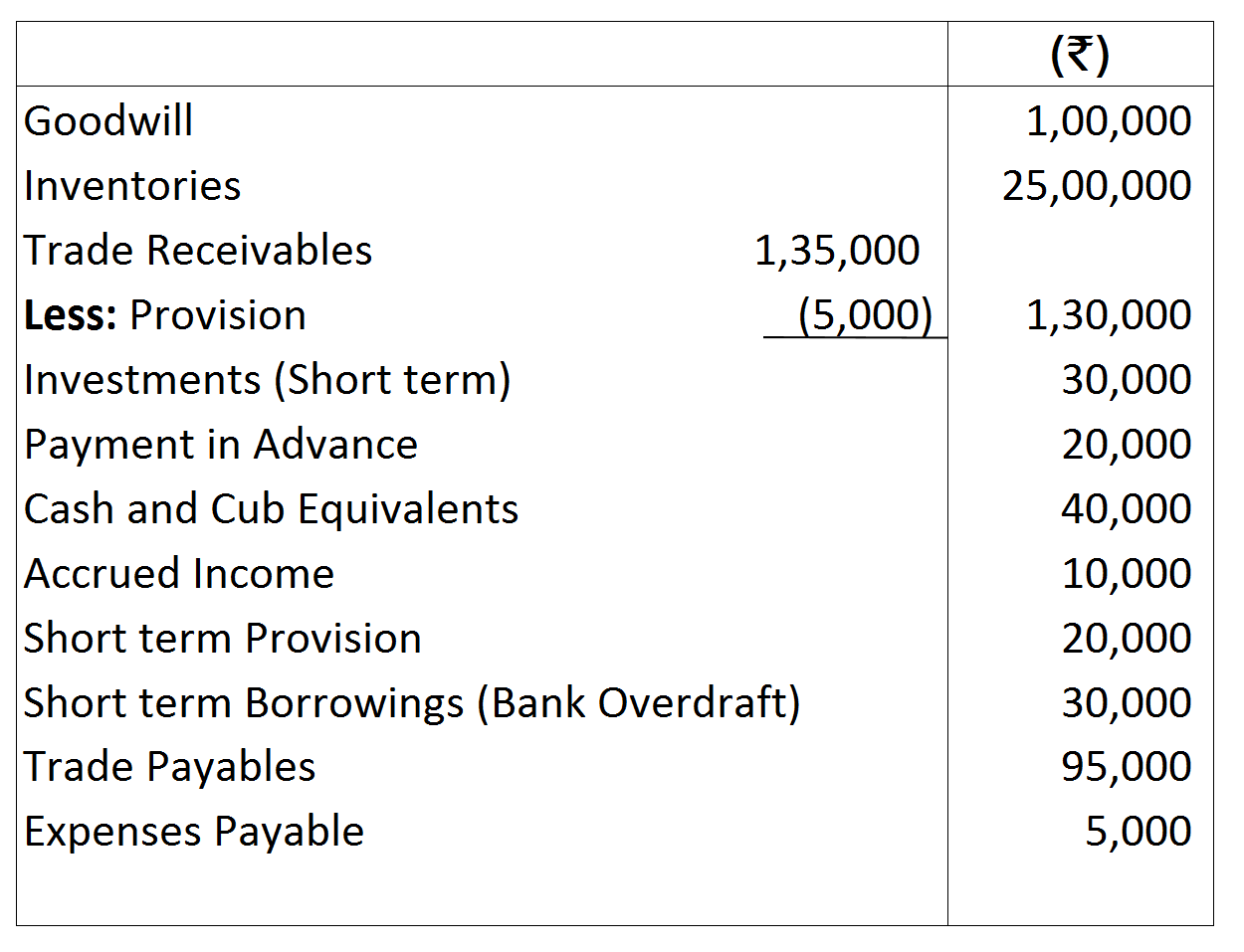

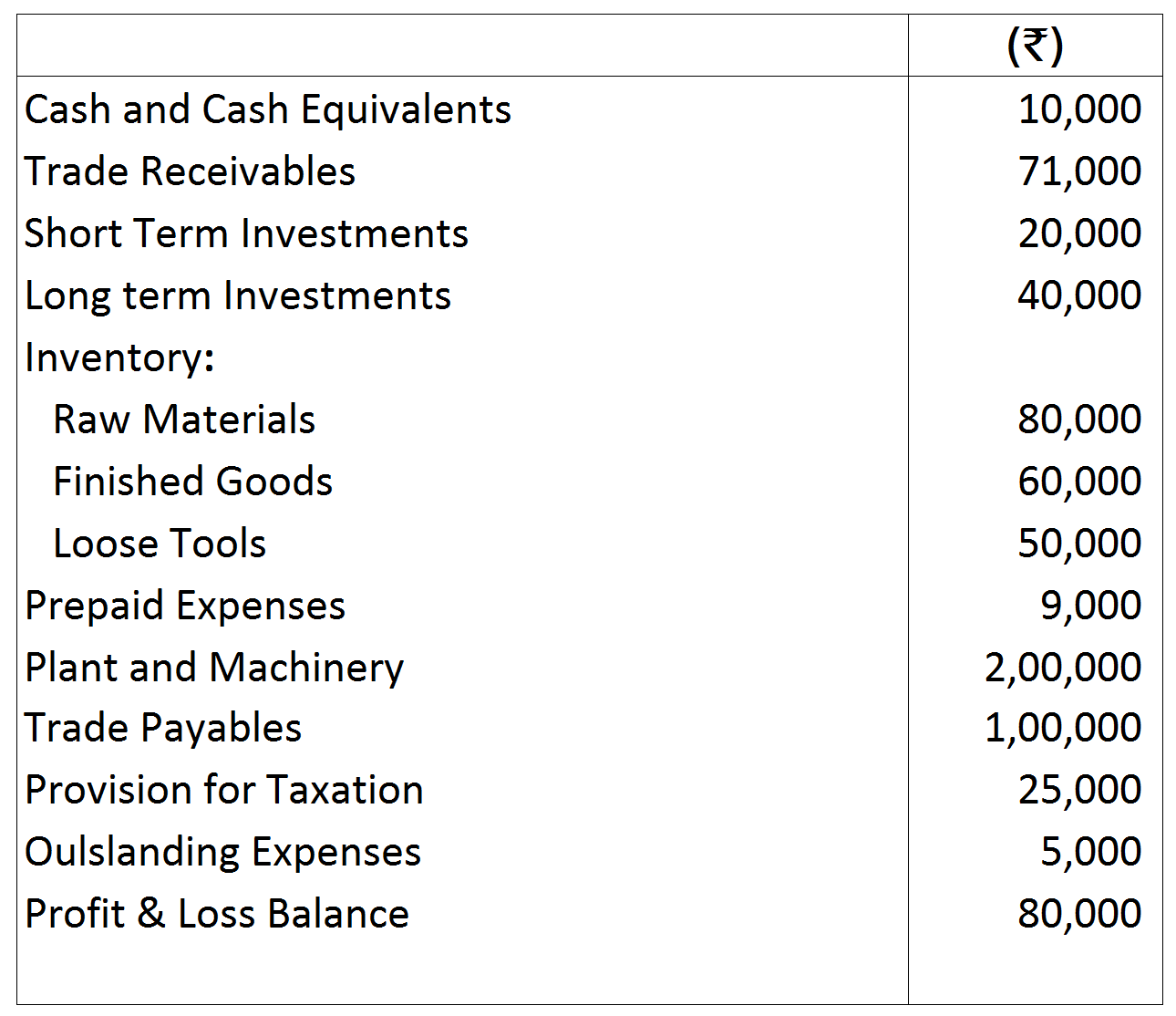

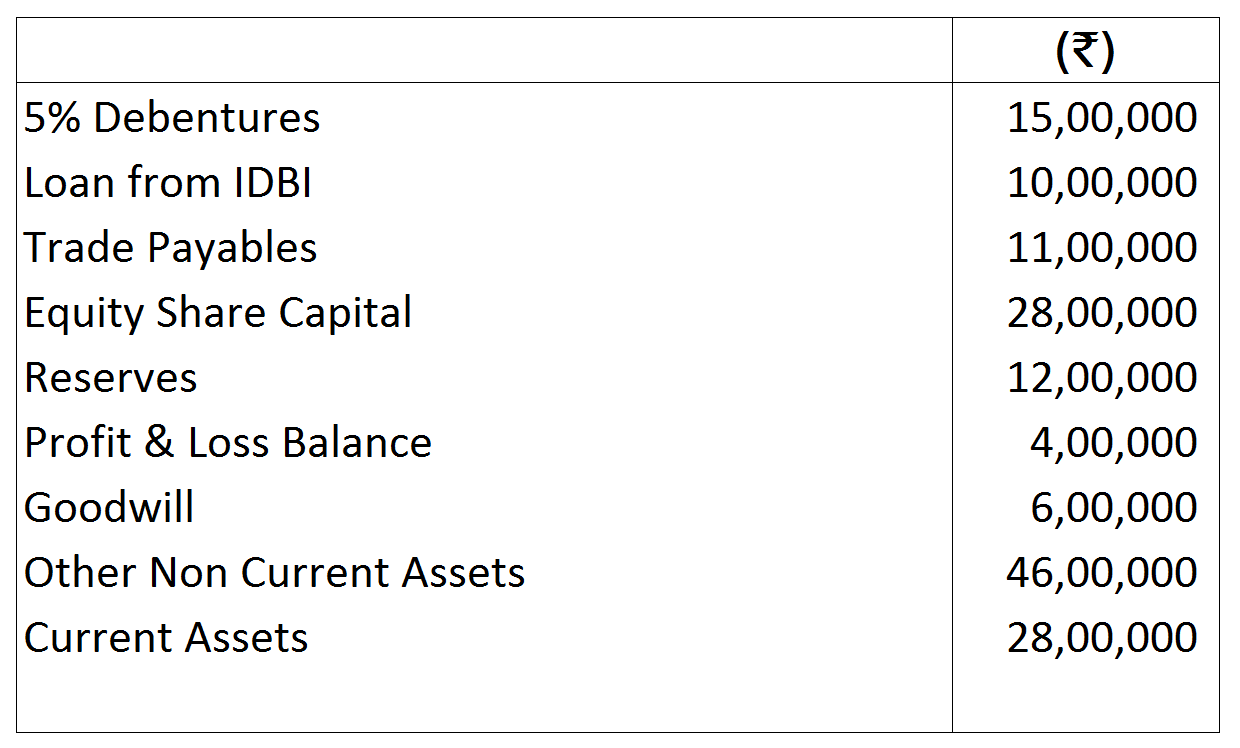

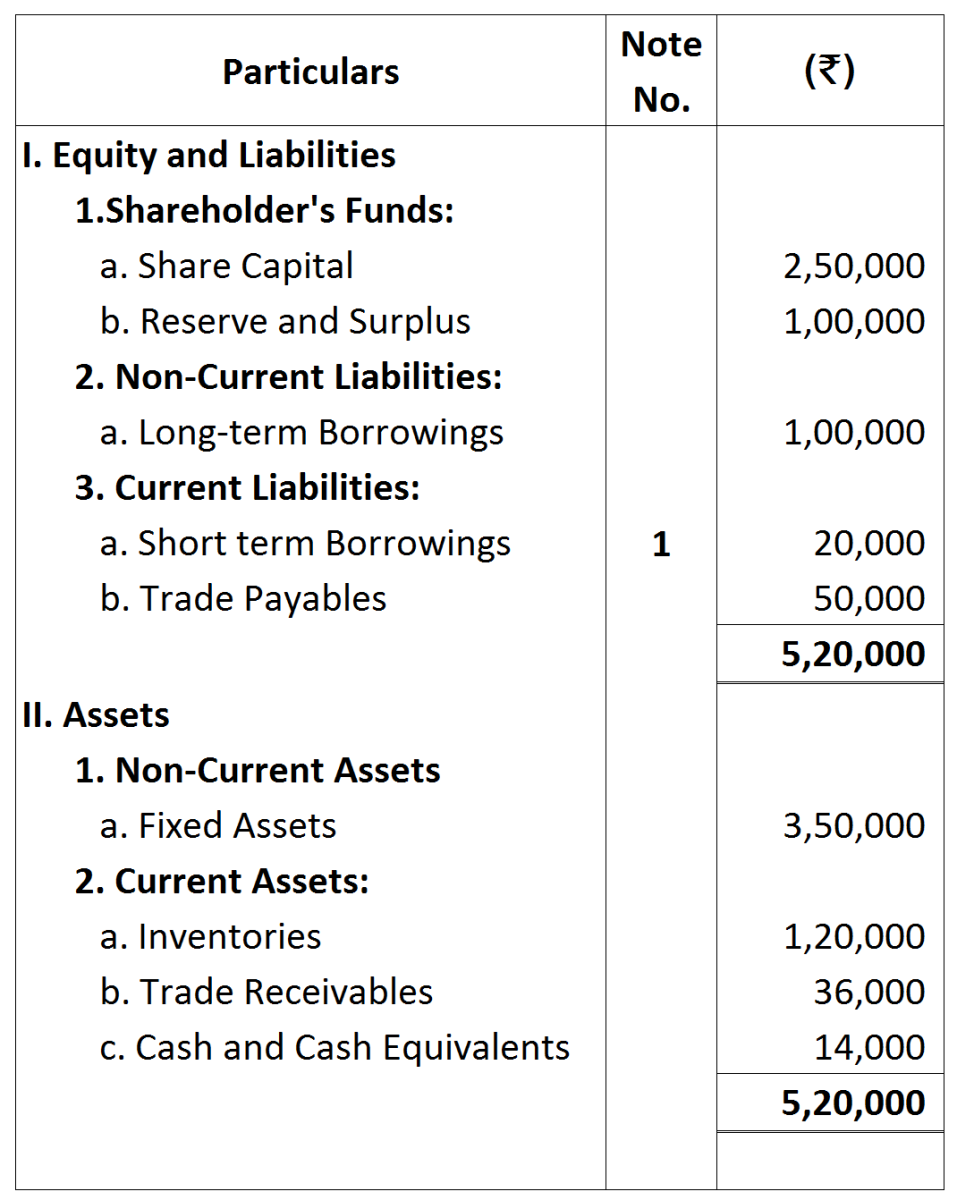

Note: Throw light on the short-term financial position of the Company with the help of suitable ratios.

Throw light on the short-term financial position of the Company with the help of suitable ratios.

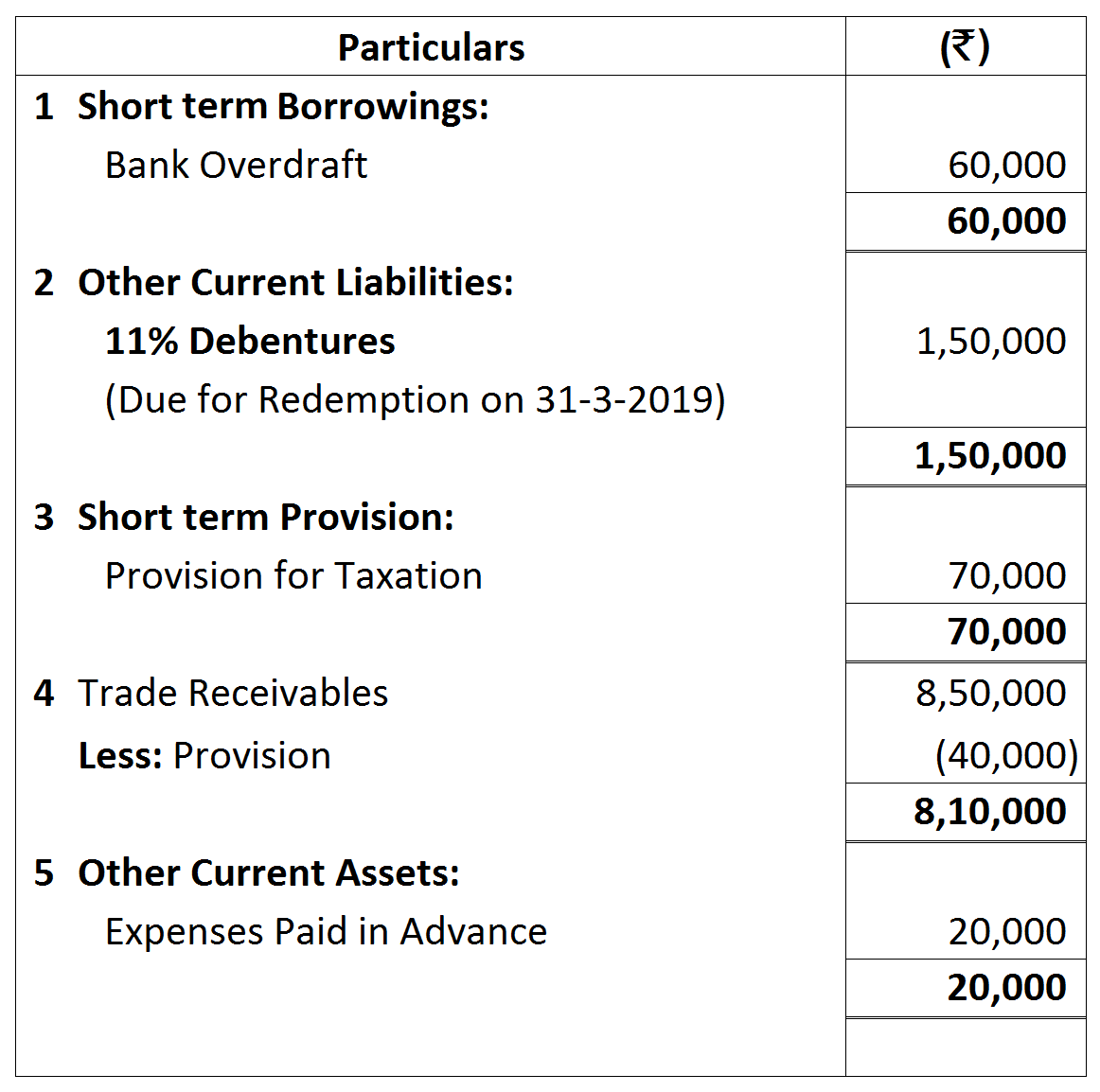

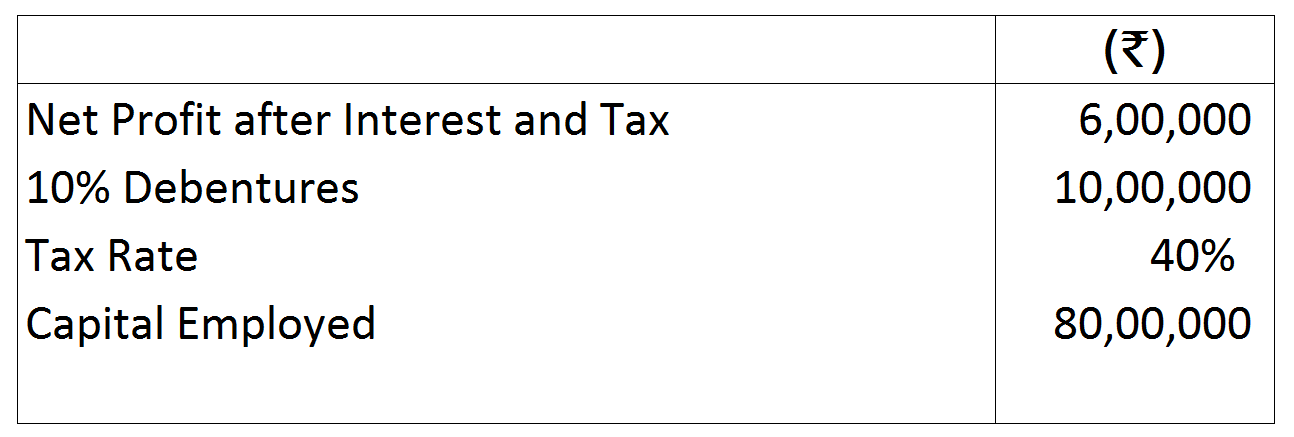

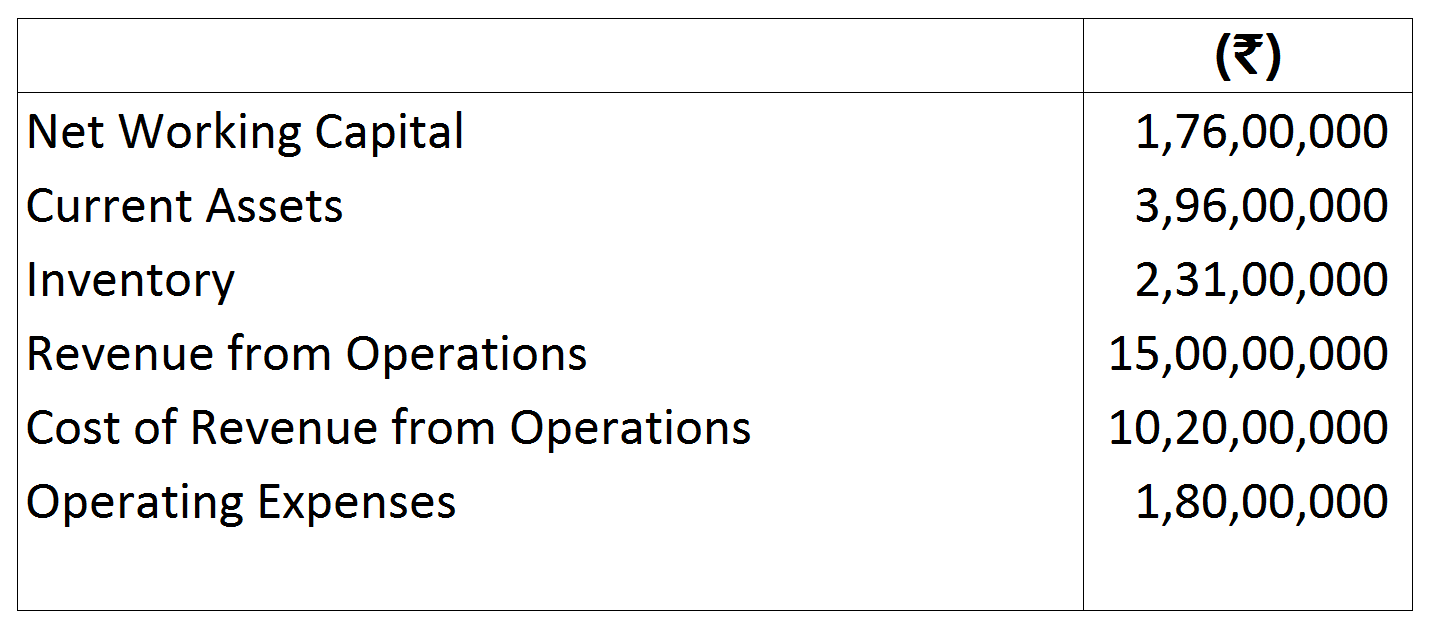

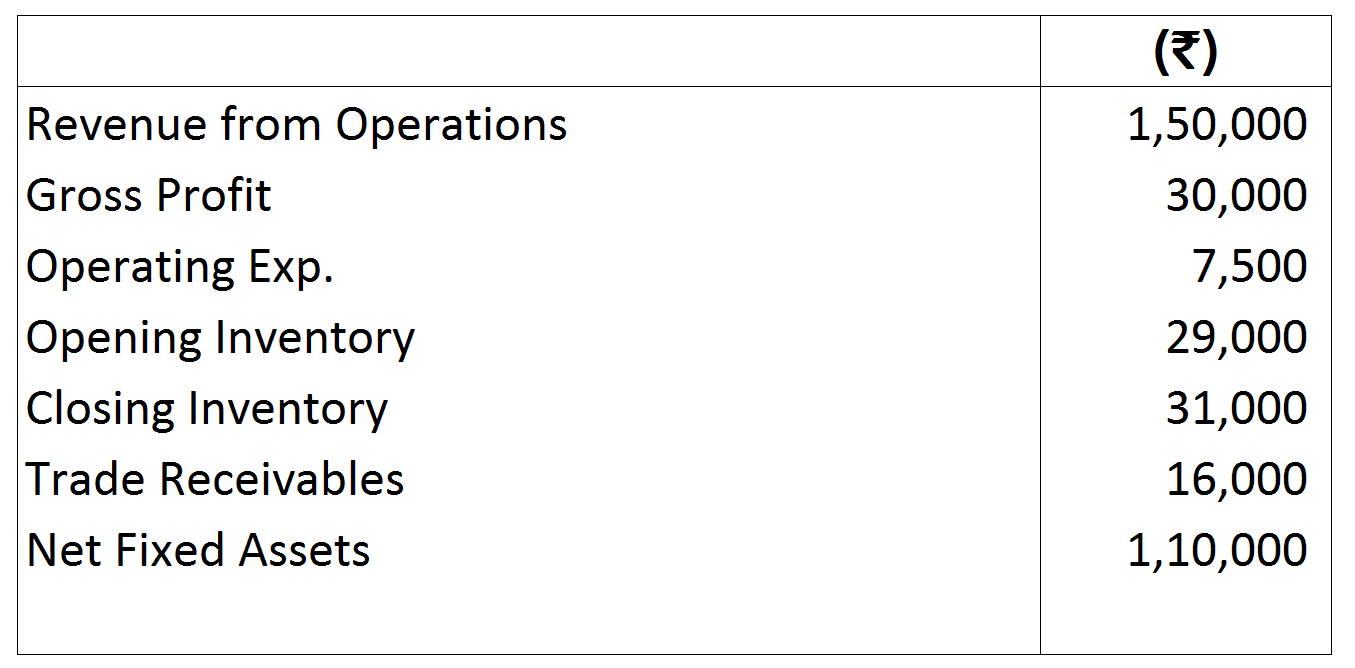

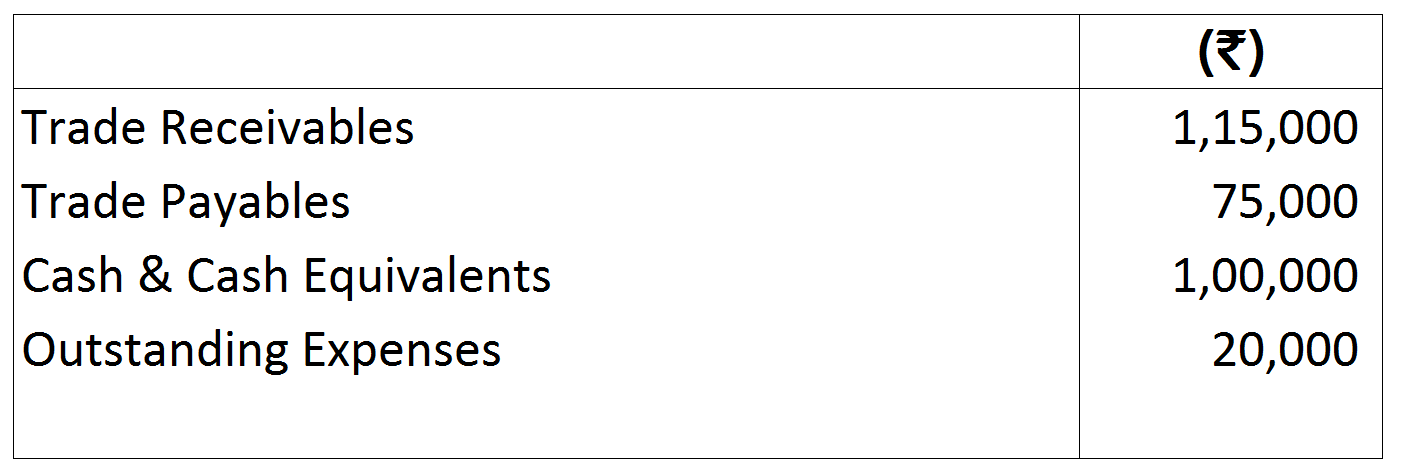

Other Informations:

Other Informations: