Question 12 Marks

The decrease in monetary value of an asset over time due to use, wear and tear or obsolescence is called depreciation. The simplest and most commonly used method of computing depreciation is straight line or linear method of depreciation. In this method the depreciation amount is the same for every year over the useful life of the asset i.e., the depreciation amount charged until the asset gets reduced to zero, value or its salvage value at the end of its useful life. In linear depreciation method the annual depreciation of an asset is found by dividing the total depreciation by the number of year in its estimated useful life.

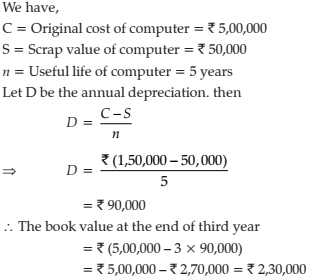

Q. 1. A mainframe computer whose cost is ₹ 5,00,000 will depreciate to a scrap value of ₹ 50,000 in 5 years. Using linear method of depreciation, find the book value of computer at the end of third year.

Q. 2. An asset costing ₹ $1,50,000$ is expected to have a useful life of 5 years and scrap value of ₹ 30,000 . Find the annual depreciation charge and the depreciation rate by using the linear depreciation method.

Q. 1. A mainframe computer whose cost is ₹ 5,00,000 will depreciate to a scrap value of ₹ 50,000 in 5 years. Using linear method of depreciation, find the book value of computer at the end of third year.

Q. 2. An asset costing ₹ $1,50,000$ is expected to have a useful life of 5 years and scrap value of ₹ 30,000 . Find the annual depreciation charge and the depreciation rate by using the linear depreciation method.

Answer

View full question & answer→(1)

(2) we have,

C = Original cost of asset = ₹ 150,000

S = Scrap value / salvage value = ₹ 30,000

n = Useful life = 5 years

the annual depreciation charge, D is given by

$\begin{aligned} & D=\frac{C-S}{n} \\ \Rightarrow \quad D & =\frac{1,50,000-30,000}{5}\end{aligned}$

$\Rightarrow$ D = ₹ 24,000

Now, Depreciation Rate

$

\begin{array}{l}

=\frac{\text { Annual Depreciation }}{\text { Cost of the asset }- \text { Salvage value }} \times 100 \\

=\frac{24,000}{1,50,000-30,000} \times 100 \\

=\frac{24,000}{12,000} \times 100 \\

=20 \%

\end{array}

$

(2) we have,

C = Original cost of asset = ₹ 150,000

S = Scrap value / salvage value = ₹ 30,000

n = Useful life = 5 years

the annual depreciation charge, D is given by

$\begin{aligned} & D=\frac{C-S}{n} \\ \Rightarrow \quad D & =\frac{1,50,000-30,000}{5}\end{aligned}$

$\Rightarrow$ D = ₹ 24,000

Now, Depreciation Rate

$

\begin{array}{l}

=\frac{\text { Annual Depreciation }}{\text { Cost of the asset }- \text { Salvage value }} \times 100 \\

=\frac{24,000}{1,50,000-30,000} \times 100 \\

=\frac{24,000}{12,000} \times 100 \\

=20 \%

\end{array}

$