Question

Correct the following errors: (1) without Suspense Account and (2) with Suspense Account:

i. Sales Book has been totalled ₹ 8,000 short.

ii. Goods of ₹ 1,500 returned by Shivam & Co., have not been recorded.

iii. Goods purchased of ₹ 2,500 was posted to debit of the supplier, Ram.

iv. Furniture purchased from Pink & Co., of ₹ 10,000 has been entered in Purchases Book.

v. Cash received from Aniket ₹ 3,500 has not been posted in his account. Also prepare Suspense Account.

i. Sales Book has been totalled ₹ 8,000 short.

ii. Goods of ₹ 1,500 returned by Shivam & Co., have not been recorded.

iii. Goods purchased of ₹ 2,500 was posted to debit of the supplier, Ram.

iv. Furniture purchased from Pink & Co., of ₹ 10,000 has been entered in Purchases Book.

v. Cash received from Aniket ₹ 3,500 has not been posted in his account. Also prepare Suspense Account.

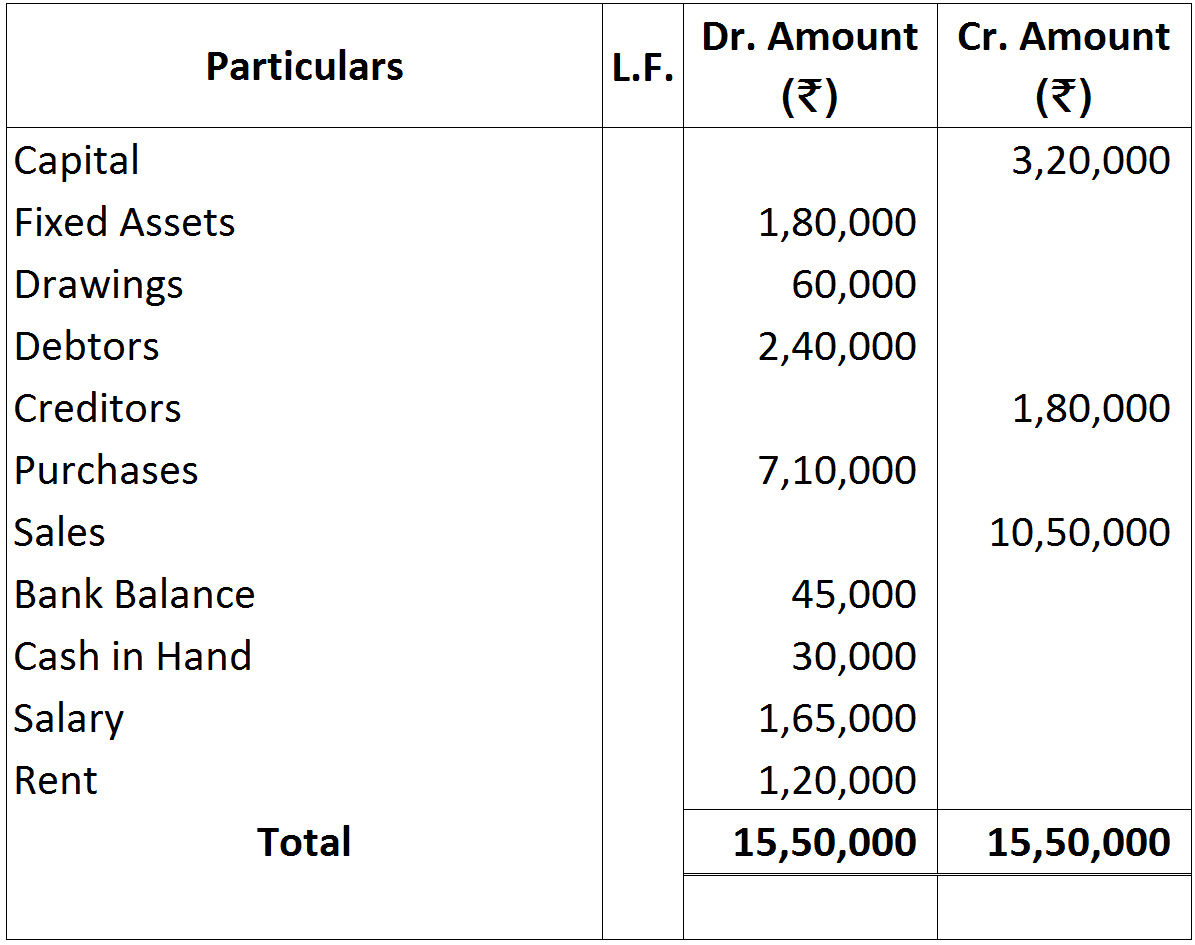

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded:

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded: