Question

Explain the factors which necessiated systematic accounting.

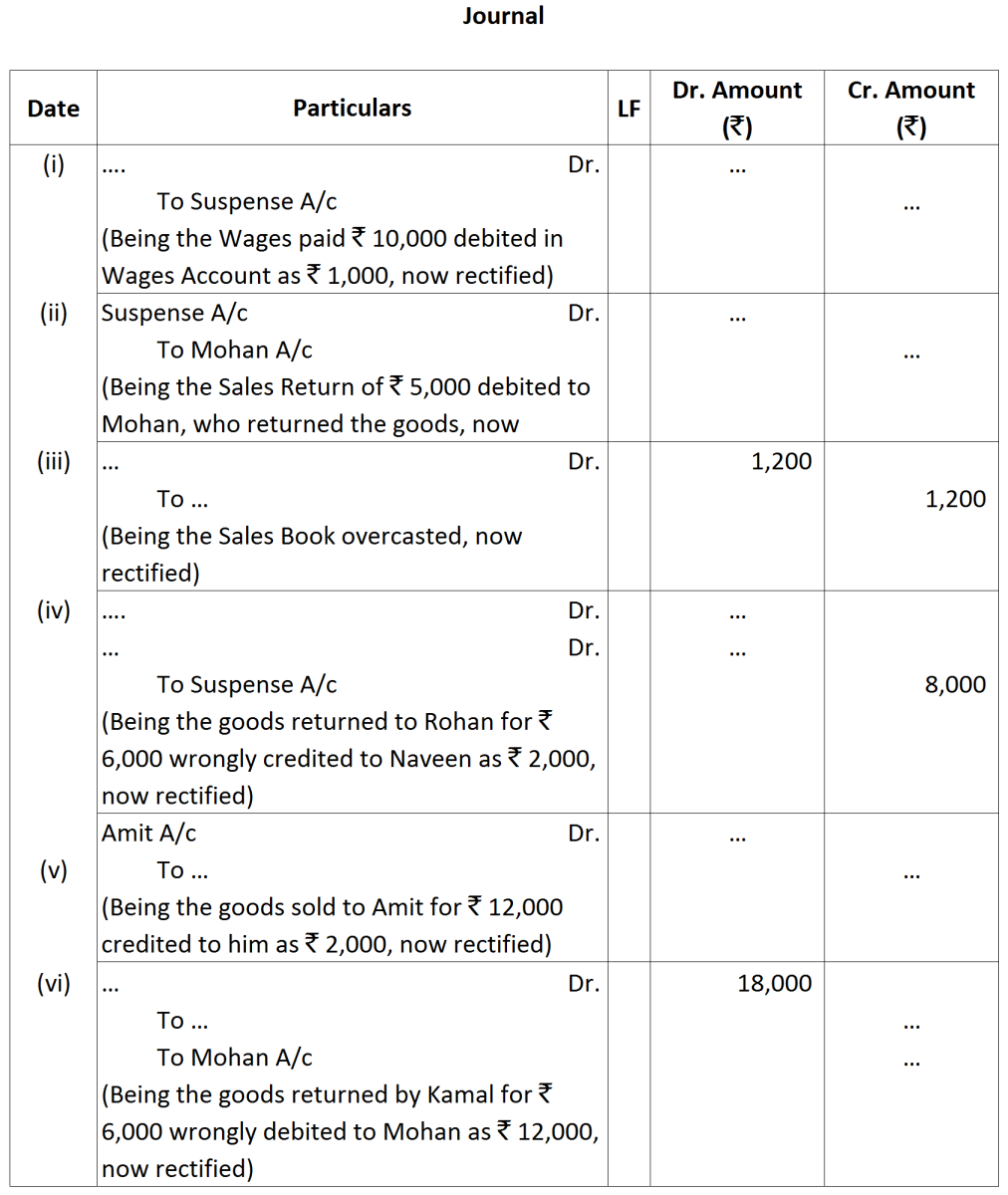

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| 2017 | |

| Jan. 1 | Assets: Cash in hand ₹ 20,000; Debtors: Sri Gopal ₹ 15,000, Poonam & Co. ₹ 30,000; Stock ₹ 1,75,000, Machinery ₹ 1,20,000; Furniture ₹ 40,000 |

| Liabilities: Bank Overdraft ₹ 33,000; Creditors: Niranjan Lal ₹ 24,000, Bombay Trading Co. ₹ 16,000 | |

| Jan. 2 | Purchased from Manohar Lal & Sons goods of the list price of ₹ 20,000 at 10% trade discount |

| Jan. 5 | Returned to Manohar Lal & sons goods of the list price of ₹ 2,000 |

| Jan. 10 | Issued a Cheque to Manohar Lal & Sons in full settlement of their account |

| Jan. 12 | Sold to Sri Gopal, goods worth ₹ 25,000 |

| Jan. 15 | Received Cash ₹ 10,000 and a Cheque for ₹ 8,000 from Sir Gopal. The Cheque was immediately sent to bank |

| Jan. 16 | Withdrew for personal use: Cash ₹ 5,000 and goods ₹ 3,000 |

| Jan. 17 | Accepted a bill for 45 days drawn by Niranjan Lal for the amount due to him |

| Jan. 18 | Acceptance received from Poonam & Co. for the amount due from them payable after 30 days |

| Jan. 19 | Sold to Raghubir Brothers, goods valued ₹ 16,000 |

| Jan. 20 | Cash purchases ₹ 15,000 |

| Jan. 22 | Withdrew from bank fo office use ₹ 10,000 |

| Jan. 23 | Purchased from Bombay Trading Co., goods valued ₹ 24,000 |

| Jan. 24 | Sri Gopal returned goods worth ₹ 2,000 |

| Jan. 25 | Received from Raghubir Brothers ₹ 10,000 |

| Jan. 27 | Accepted a bill for ₹ 25,000 for 1 month drawn by Bombay Trading Co |

| Jan. 27 | Paid Rent by Cheque ₹ 2,800 |

| Received Commission in Cash ₹ 800 | |

| Jan. 31 | Paid salaries ₹ 5,000 |

| March 1 | Purchased furniture on credit from Kuber Furniture Store for ₹ 15,000. |

| March 5 | Goods for ₹ 6,000 given away as charity. |

| March 12 | Goods worth ₹ 8,000 and Cash ₹ 4,000 were stolen by an employee. |

| March 15 | Arun who owed us ₹ 20,000 was declared insolvent and nothing was received from him. |

| March 18 | Proprietor withdrew for his personal use cash ₹ 5,000 and goods worth ₹ 10,000. |

| March 31 | Provide interest on capital of ₹ 5,00,000 at 6% p.a. for full year. |

| March 31 | Out of the rent paid this year, ₹ 5,000 is related to the next year. |

| March 31 | Salaries due to clerks ₹ 12,000. |

|

2017

|

|

|

Jan. 1

|

Assets: Cash in hand ₹ 8,500; Cash at Bank ₹ 1,40,000; Stock of goods ₹ 2,20,000; Due from Manohar Lal ₹ 30,000 and Deep Chand ₹ 24,000; Furniture and Equipment ₹ 3,00,000.

|

|

Liabilities: Due to Sunil ₹ 15,000.

|

|

|

Jan. 2

|

Withdrawn from bank ₹ 20,000.

|

|

Jan. 4

|

Paid salaries ₹ 22,000.

|

|

Jan. 6

|

Sold goods to Surya Narain:

|

|

60 metres silk @ ₹ 150 per metre

|

|

|

100 metres cotton @ ₹ 70 per metre

|

|

|

Less: Trade Discount @ $12\frac{1}{2}\%$

|

|

|

Jan. 8

|

Surya Narain returned 40 metres Cotton.

|

|

Jan. 9

|

Received full payment from Manohar Lal by cheque, sent it to bank, Discount allowed 3%.

|

|

Jan. 10

|

Purchased from Ganga Parshad:

|

|

300 metres cotton @ ₹ 60 per metre

|

|

|

500 metres silk @ ₹ 120 per metre

|

|

|

Less: Trade Discount 10%.

|

|

|

Jan. 12

|

Sold goods to Vinita for cash ₹ 16,000.

|

|

Jan. 13

|

Accepted a bill for ₹ 25,000 for 30 days drawn by Ganga Parshad.

|

|

Jan. 15

|

Gave cheque to Ganga Parshad for ₹ 45,000, discount allowed by him ₹ 200.

|

|

Jan. 18

|

Paid to Sunil ₹ 14,850 after receiving discount of 1%.

|

|

Jan. 20

|

Mr. Keshav Chand took away 5 metres silk costing ₹ 100 per metre for his personal use.

|

|

Jan. 24

|

Paid rent by cheque ₹ 2,000.

|

|

Jan. 25

|

Received from Surya Narain ₹ 11,000 in full settlement of his account.

|

|

Jan. 27

|

Old newspapers sold for cash ₹ 400.

|

|

Jan. 27

|

Paid for stationery and postage ₹ 500.

|

|

Jan. 28

|

Sold 400 metres silk @ ₹ 160 per metre to Sh. Ganesh Chand.

|

|

Jan. 31

|

Received cash ₹ 40,000 from Sh. Ganesh Chand and also received a B/R from him for the balance amount due from him for 2 months.

|