Question

Fill in the missing figures assuming CGST @ 9% and SGST @ 9%:

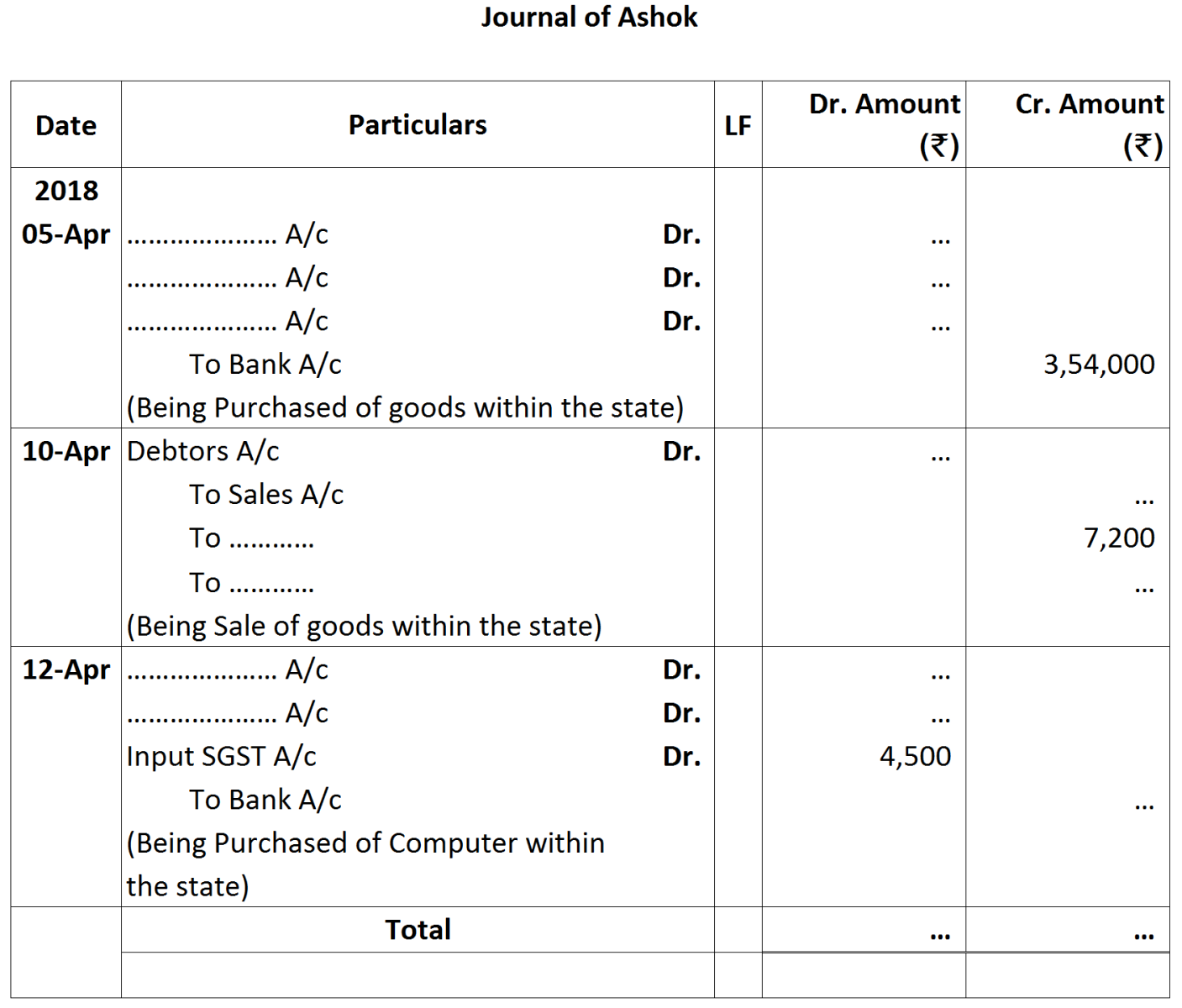

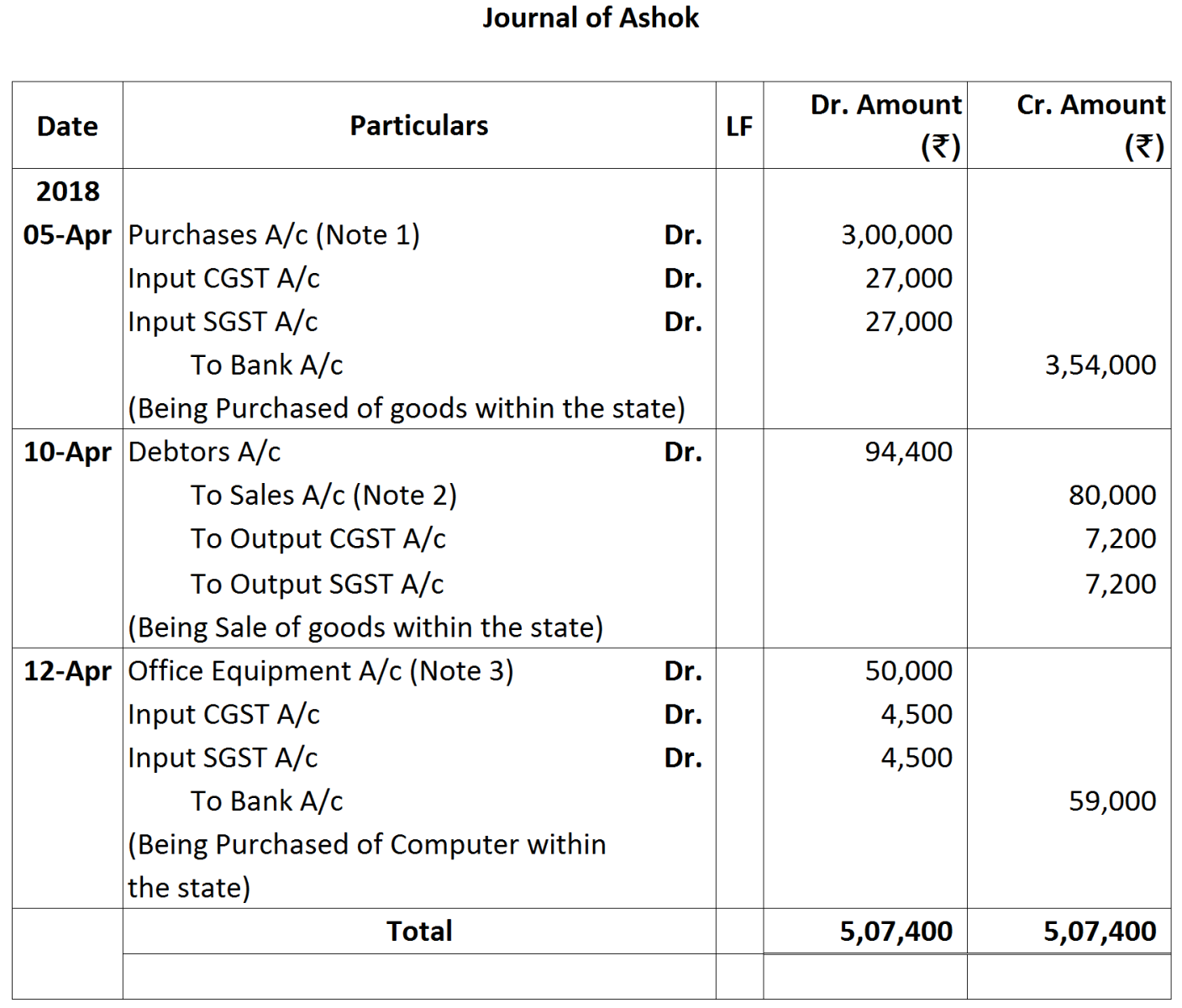

$3,54,000\times\frac{100}{118}=₹\ 3,00,000$

$3,54,000\times\frac{100}{118}=₹\ 3,00,000$Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

1.

|

Purchased goods from Karunakaran of Chennai for ₹ 1,00,000.

(IGST @18%) |

|

2.

|

Sold goods to Ganeshan of Bengaluru for ₹ 1,50,000.

(CGST @ 6% and SGST @ 6%) |

|

3.

|

Sold goods to S. Nair of Kerala for ₹ 2,60,000.

(IGST @18%) |

|

4.

|

Purchased a Machinery for ₹ 80,000 from Surya Ltd. against cheque.

(CGST @ 9% and SGST @ 9%) |

|

5.

|

Paid rent ₹ 30,000 by cheque.

(CGST @ 6% and SGST @ 6%) |

|

6.

|

Purchased goods from Ram Mohan Rai of Bengaluru for ₹ 2,00,000.

(CGST @ 6% and SGST @ 6%) |

|

7.

|

Paid insurance premium ₹ 10,000 by cheque.

(CGST @ 9% and SGST @ 9%) |

|

8.

|

Received commission ₹ 20,000 by cheque which is deposited into bank.

(CGST @ 9% and SGST @ 9%) |

|

9.

|

Payment made of balance amount of GST.

|

|

1.

|

Purchased goods for ₹ 2,00,000 and payment made by cheque.

|

|

2.

|

Sold goods for ₹ 1,60,000 to Devki Nandan & Sons.

|

|

3.

|

Purchased goods for ₹ 50,000 on credit.

|

|

4.

|

Paid for printing and stationery ₹ 4,000.

|

|

5.

|

Received for commission ₹ 5,000.

|

|

6.

|

Output GST adjusted against Input GST.

|

|

2019

|

|

₹

|

|

April 2

|

Bought office furniture

|

20,000

|

|

April 5

|

Purchased goods

|

16,000

|

|

April 8

|

Purchased goods from Ramesh, Chandigarh

|

11,000

|

|

April 12

|

Sold goods to Sameer, Delhi

|

21,000

|

|

April 13

|

Purchased stationery for cash

|

1,800

|

|

April 13

|

Paid to Ramesh in cash on account*

|

10,000

|

|

|

Discount allowed by him*1,000

|

|

|

April 17

|

Withdrawn cash for office use*

|

4,000

|

|

April 18

|

Sen of Chandigarh sold goods to S.K. Gupta

|

30,000

|

|

April 19

|

Cash received from Sameer on account*

|

20,000

|

|

|

Allowed him discount*

|

1,000

|

|

April 20

|

Sold to Raj Banwari, Delhi

|

40,000

|

|

April 28

|

Cash sales

|

1,400

|

|

April 30

|

Paid salary by cheque*

|

8,000

|

|

April 30

|

Paid rent by cheque

|

5,000

|

|

April 30

|

Paid telephone expenses by cheque

|

2,000

|

|

April 30

|

Paid cash into bank*

|

2,000

|