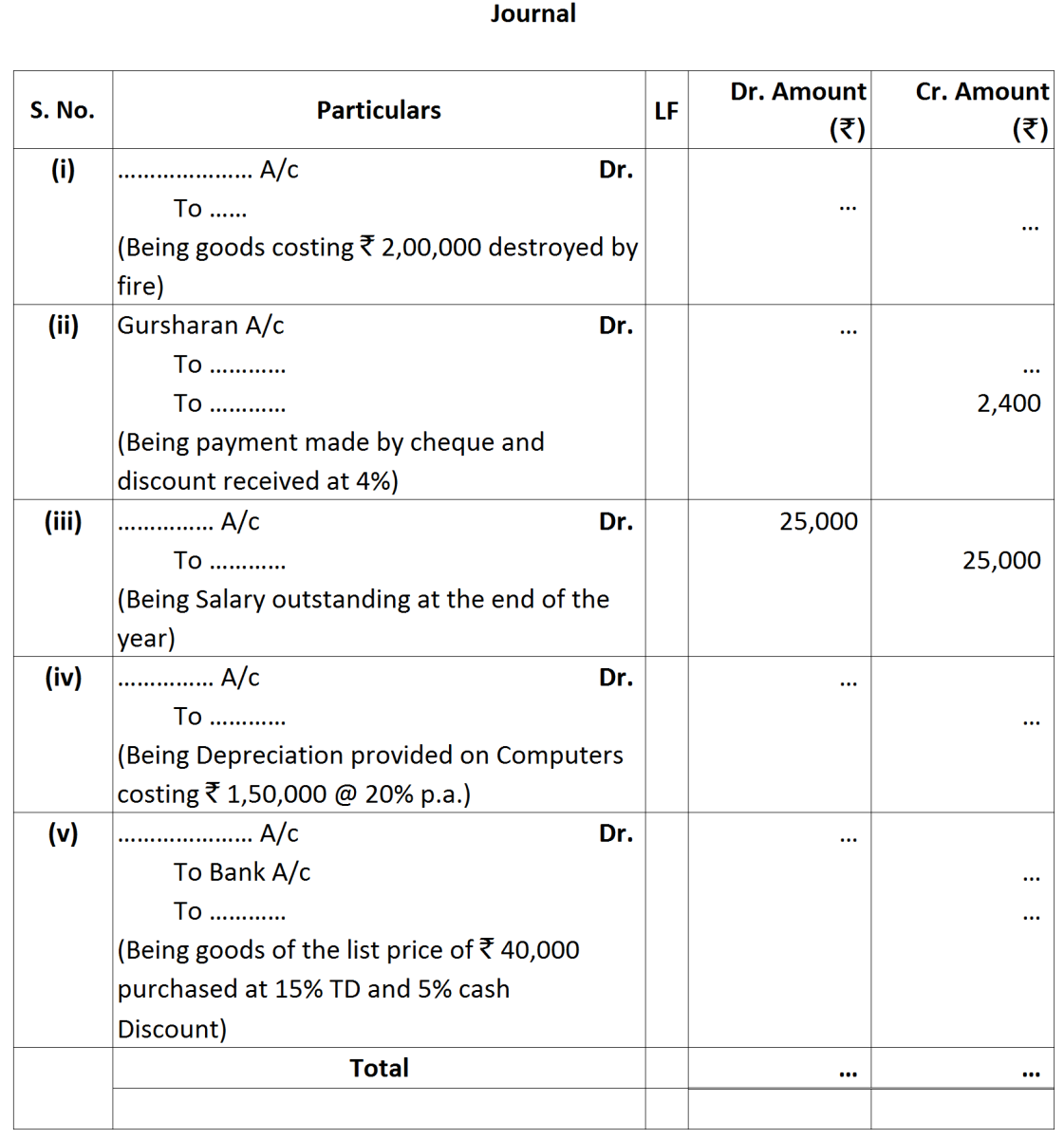

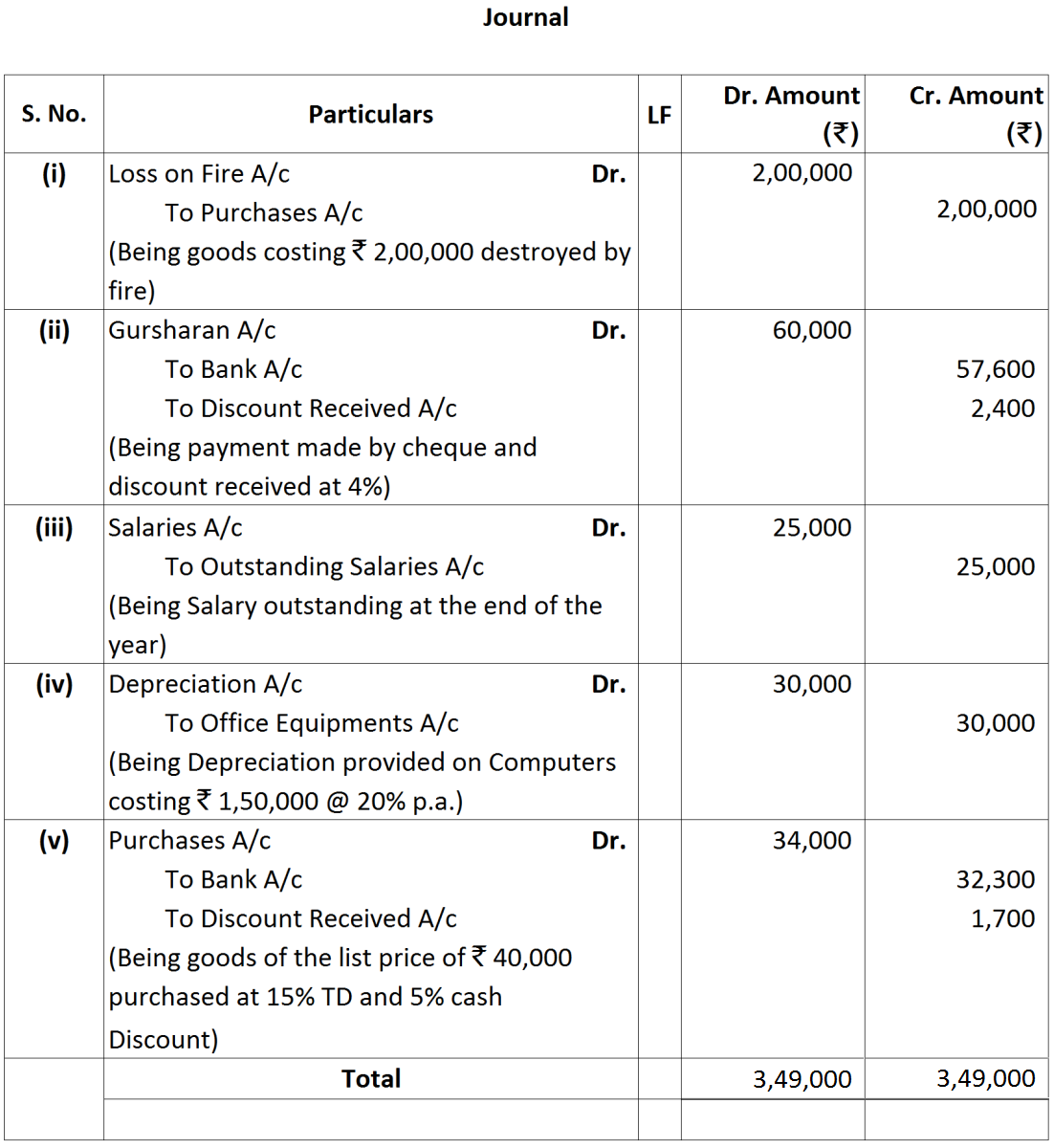

Question

Fill in the missing information in the following journal entries:

Working Note:

Working Note:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

a.

|

Started business with cash

|

₹ 1,20.000

|

|

b.

|

Purchased goods for cash

|

₹ 10,000

|

|

c.

|

Rent received

|

₹ 5,000

|

|

d.

|

Salary outstanding

|

₹ 2,000

|

|

e.

|

Prepaid Insurance

|

₹ 1,000

|

|

f.

|

Received interest

|

₹ 700

|

|

g.

|

Sold goods for cash (Costing ₹ 5,000)

|

₹ 7,000

|

|

h.

|

Goods destroyed by fire

|

₹ 500

|

|

Sundry Debtors

|

80,500

|

|

Bad debts

|

1,000

|

|

Provision for bad debts

|

5,000

|

|

Additional Information

|

|

|

Bad Debts

|

₹ 500

|

|

Machinery A/c

|

₹ 10,00,000

|

|

Provision for Depreciation A/c

|

₹4,05,000

|