Question

From the following information, calculate Inventory Turnover Ratio:

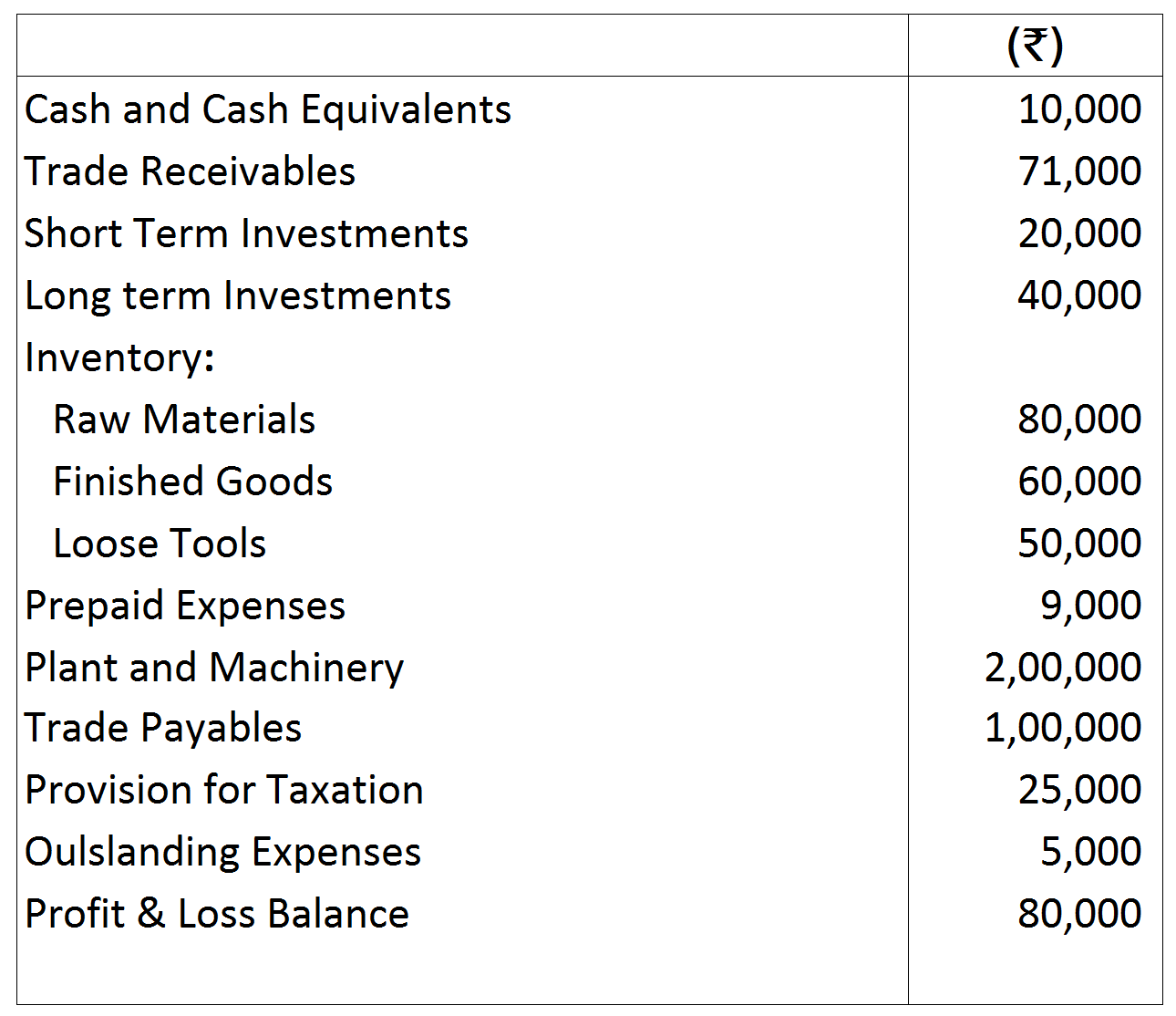

Operating Ratio and Working Capital Turnover Ratio: Opening Inventory ₹ 28,000; Closing Inventory ₹ 22,000; Purchases ₹ 46,000; Revenue from Operations, i.e., Net Sales ₹ 80,000; Return ₹ 10,000; Carriage Inwards ₹ 4,000; Office Expenses ₹ 4,000; Selling and Distribution Expenses ₹ 2,000; Working Capital ₹ 40,000.

Operating Ratio and Working Capital Turnover Ratio: Opening Inventory ₹ 28,000; Closing Inventory ₹ 22,000; Purchases ₹ 46,000; Revenue from Operations, i.e., Net Sales ₹ 80,000; Return ₹ 10,000; Carriage Inwards ₹ 4,000; Office Expenses ₹ 4,000; Selling and Distribution Expenses ₹ 2,000; Working Capital ₹ 40,000.

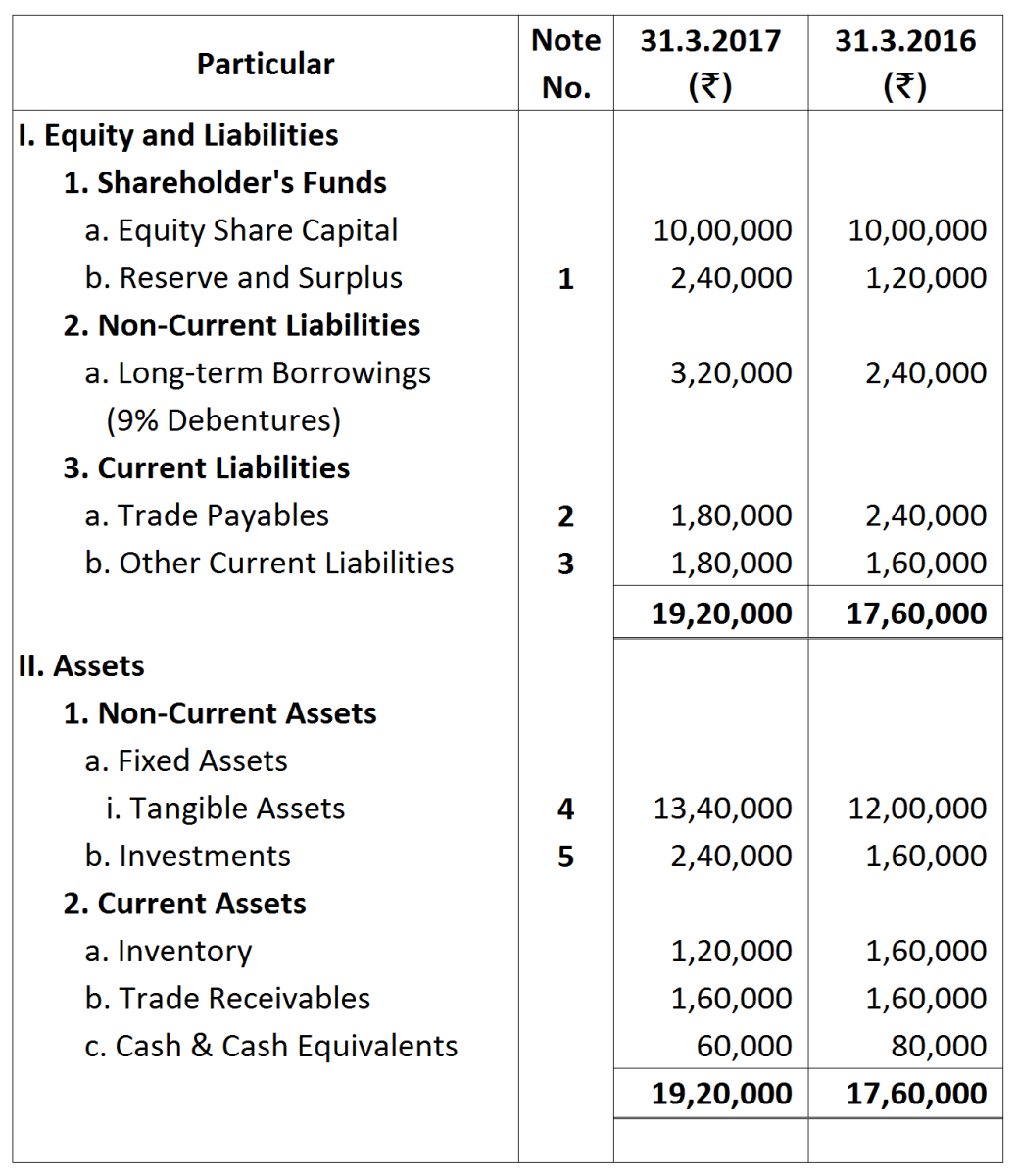

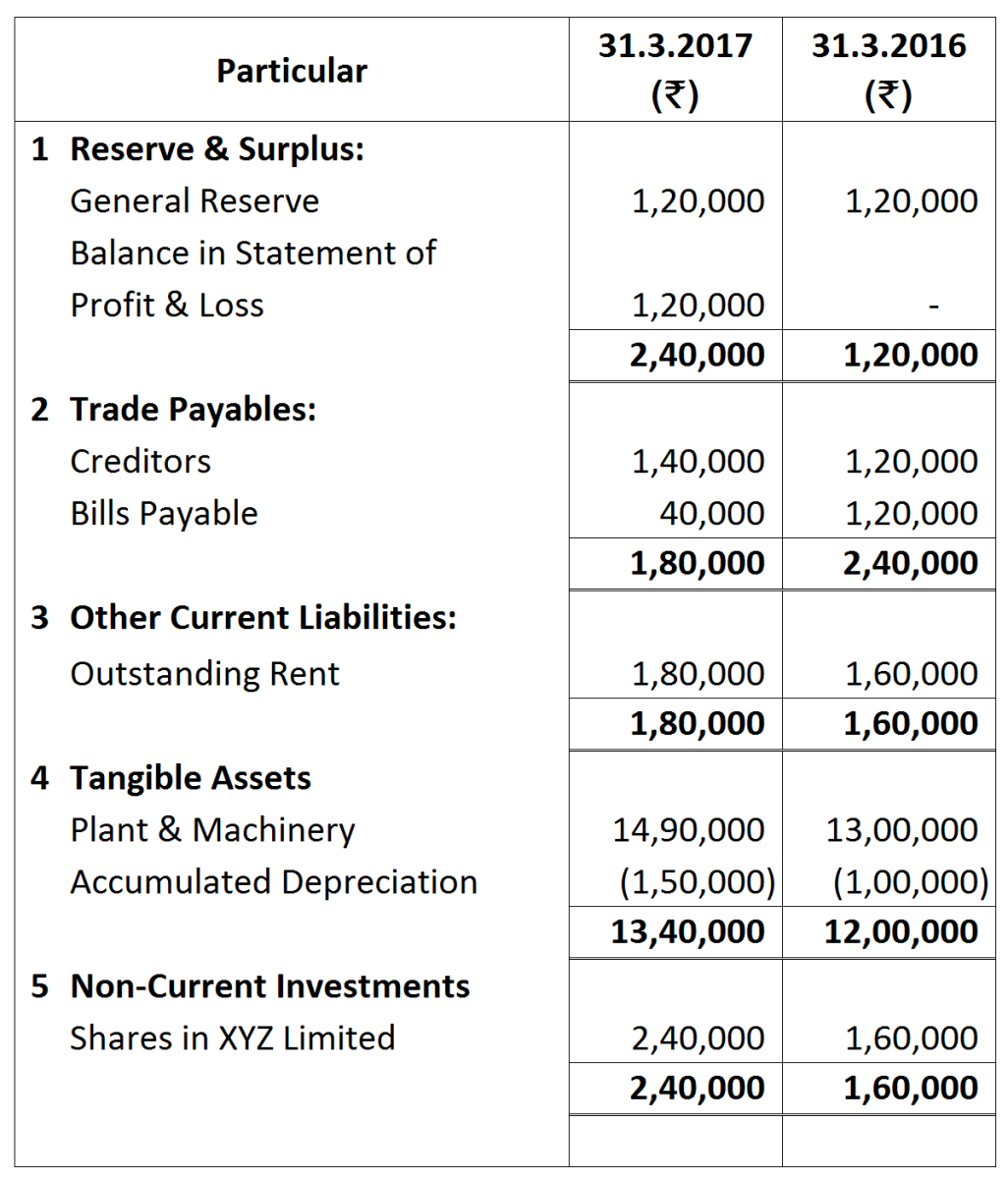

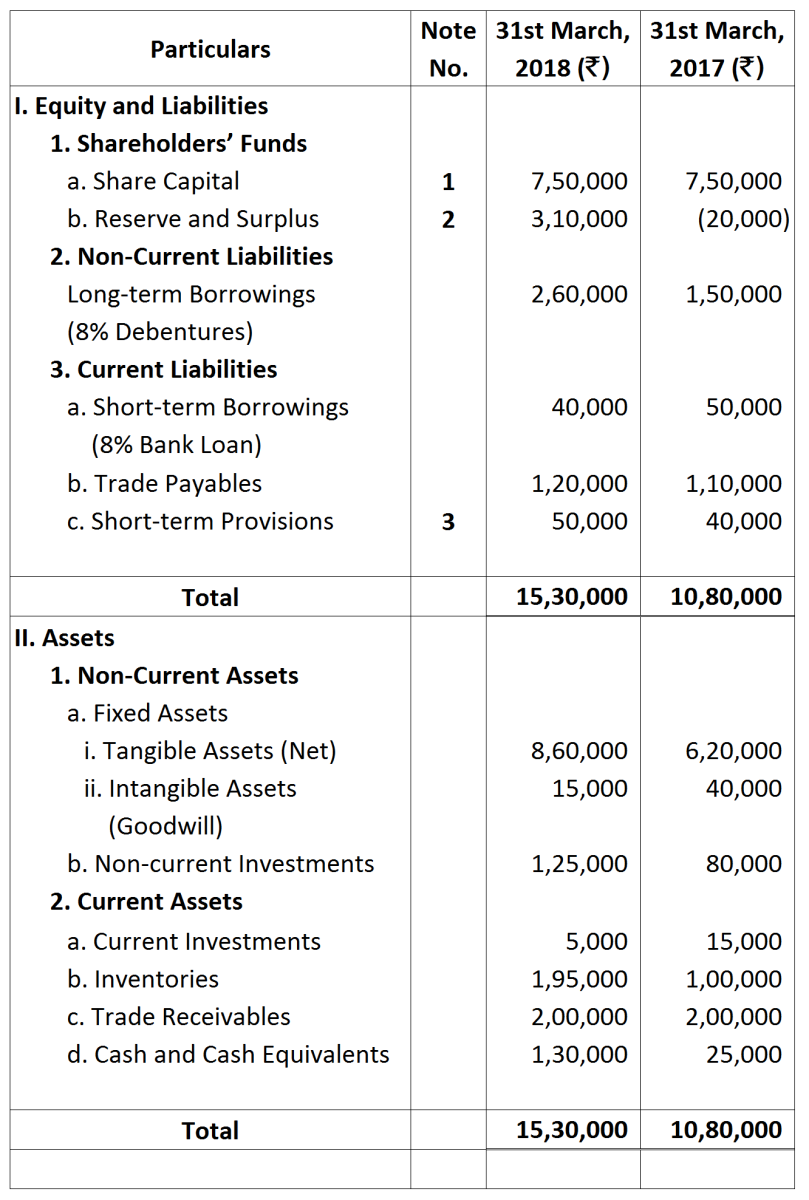

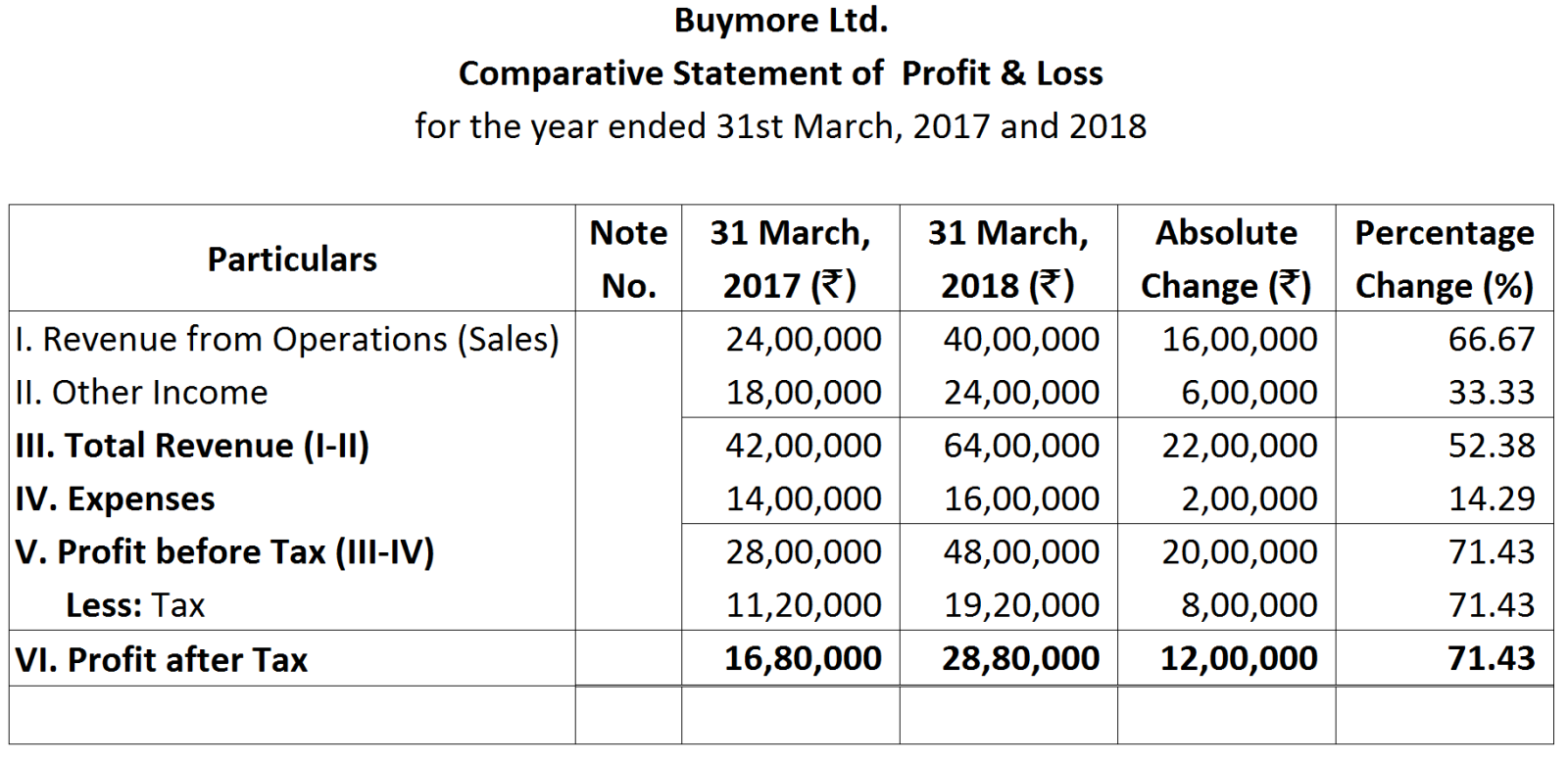

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio.

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio.