Question

State giving reason, whether the Current Ratio will improve or decline or will have no effect in each one of the following transactions if Current Ratio is (I) 2.5 : 1, (II) 1 : 1, (III) 0.75 : 1.

- Paid ₹ 50,000 to a Creditor.

- Sale of goods at a loss of 10%.

- Sale of a fixed asset for ₹ 1,00,000 (Book Value ₹ 1,20,000).

- Payment of outstanding salaries.

- Received ₹ 25,000 from a Debtor of ₹ 30,000 in full settlement of his account.

- Bills payable discharged on maturity.

- Bills Receivable drawn on debtor.

- Purchased goods on credit.

- Issued debentures to the vendors of machinery.

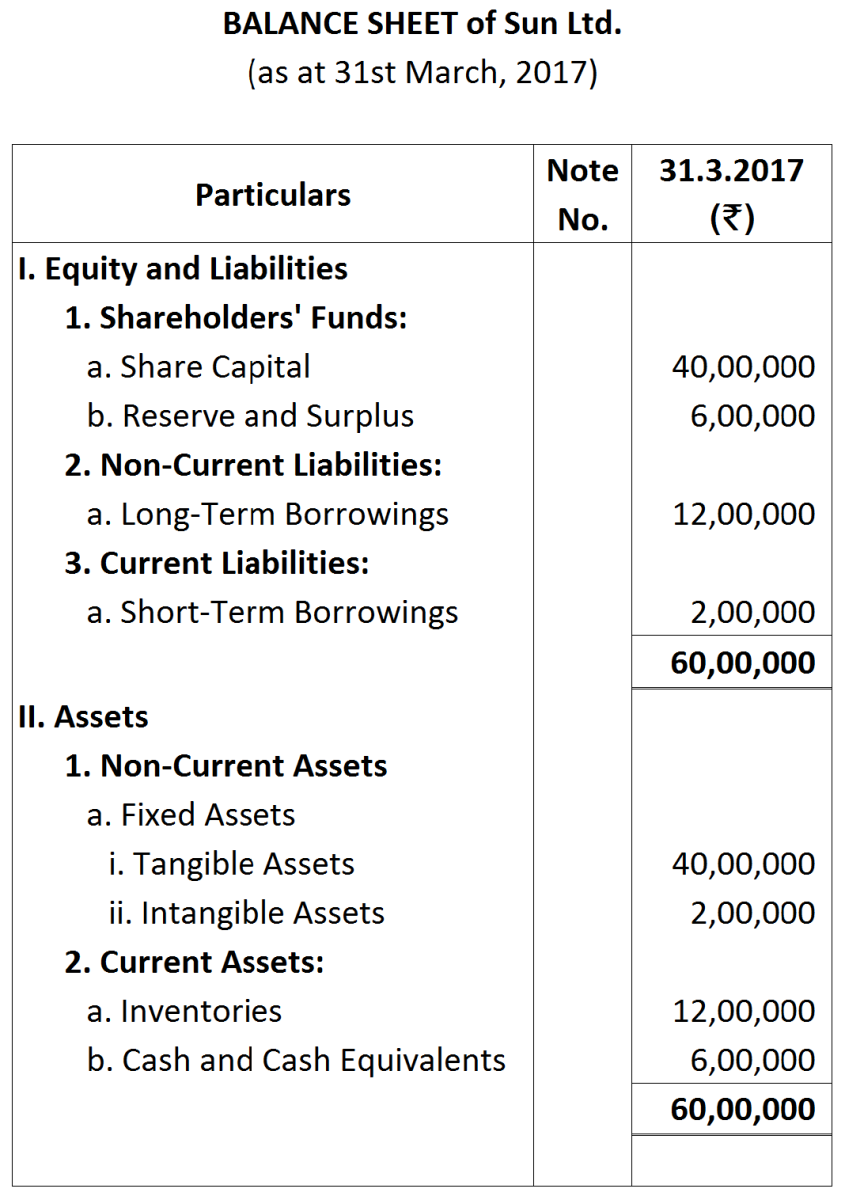

Debentures were redeemed on 1st April, 2017

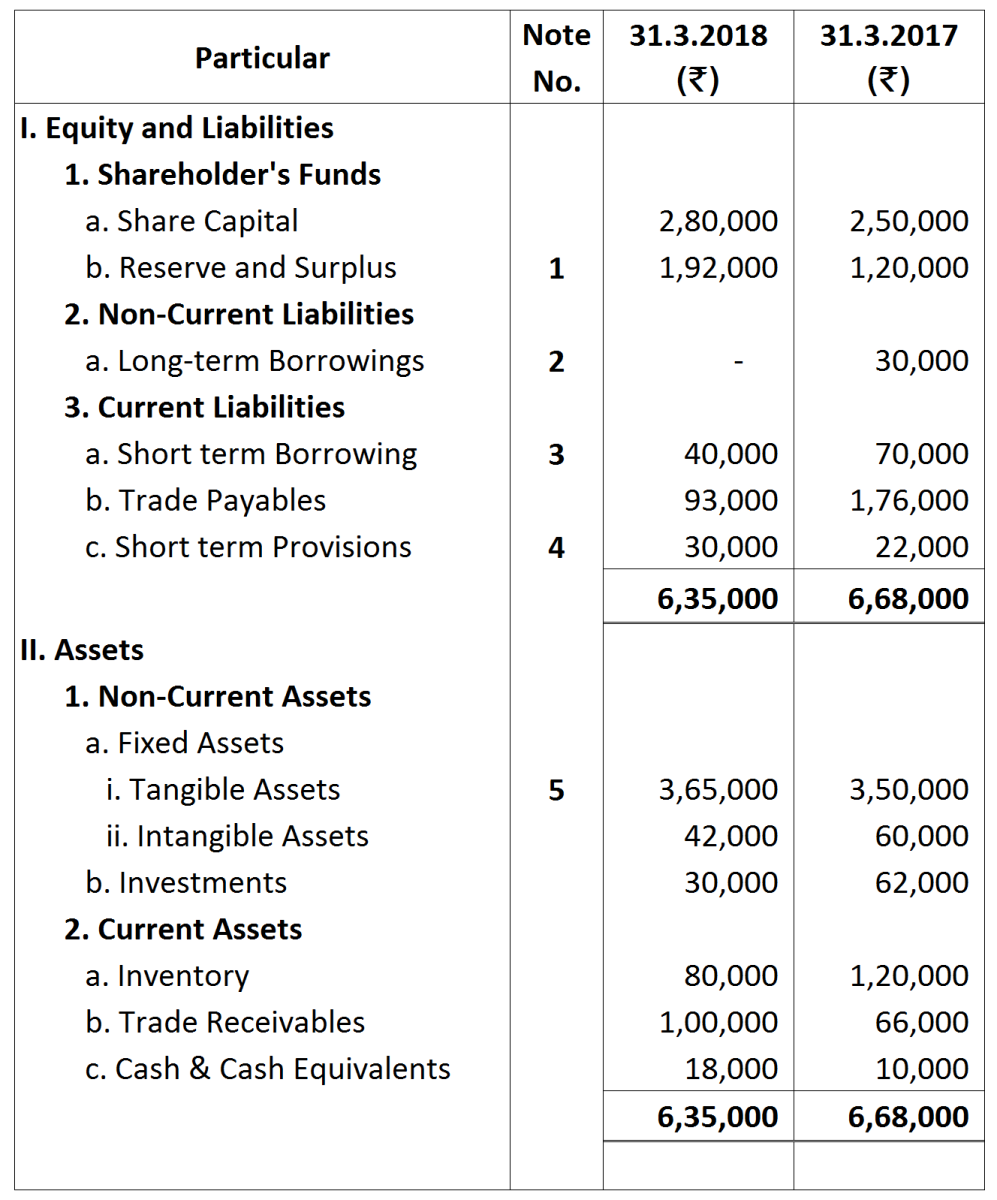

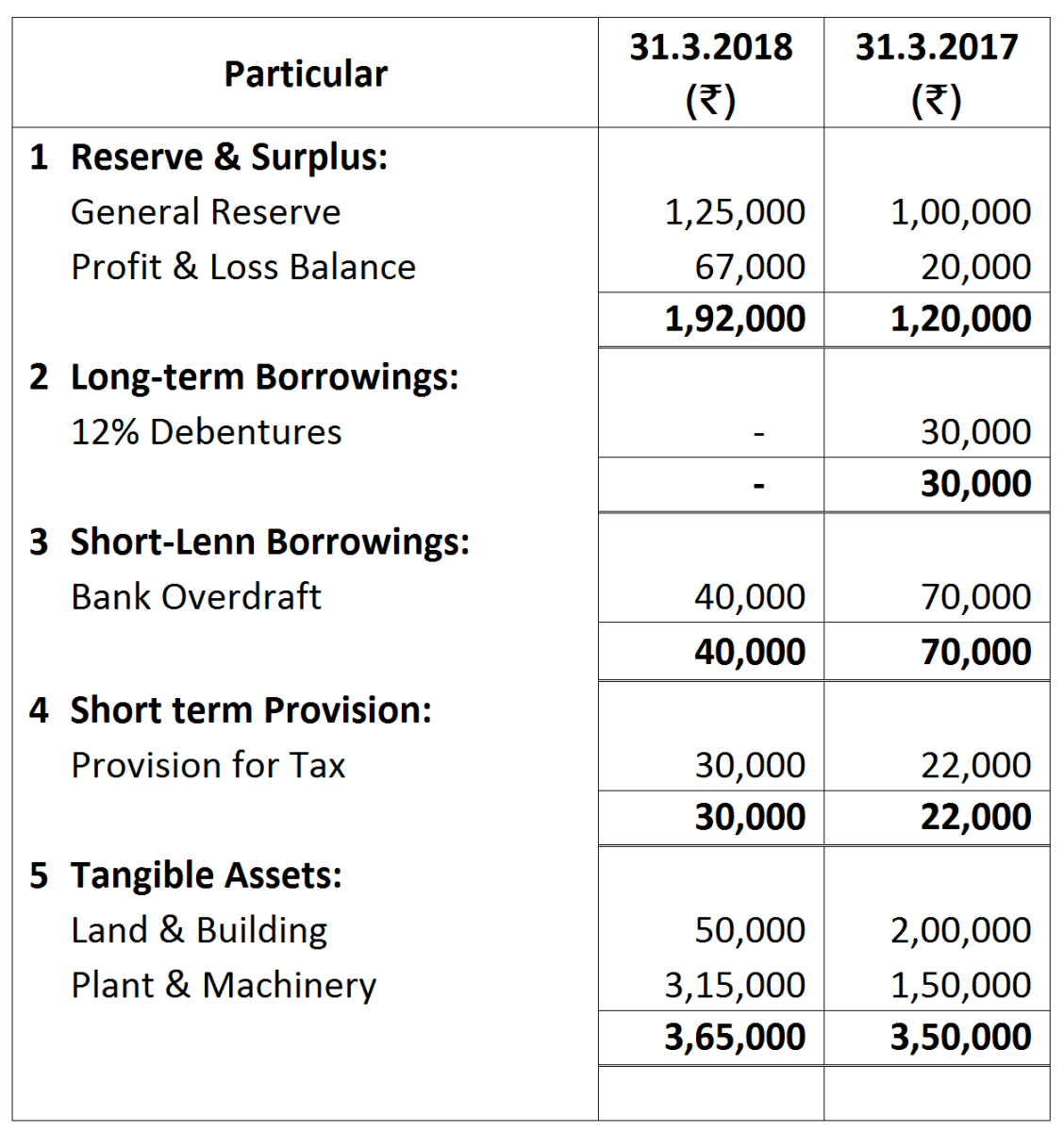

Debentures were redeemed on 1st April, 2017 From the above Common-size Balance Sheet as at 31st March, 2018, compute current Ratio, Quick Ratio, Total Assets to Debt Ratio, and Dept to Equity Ratio.

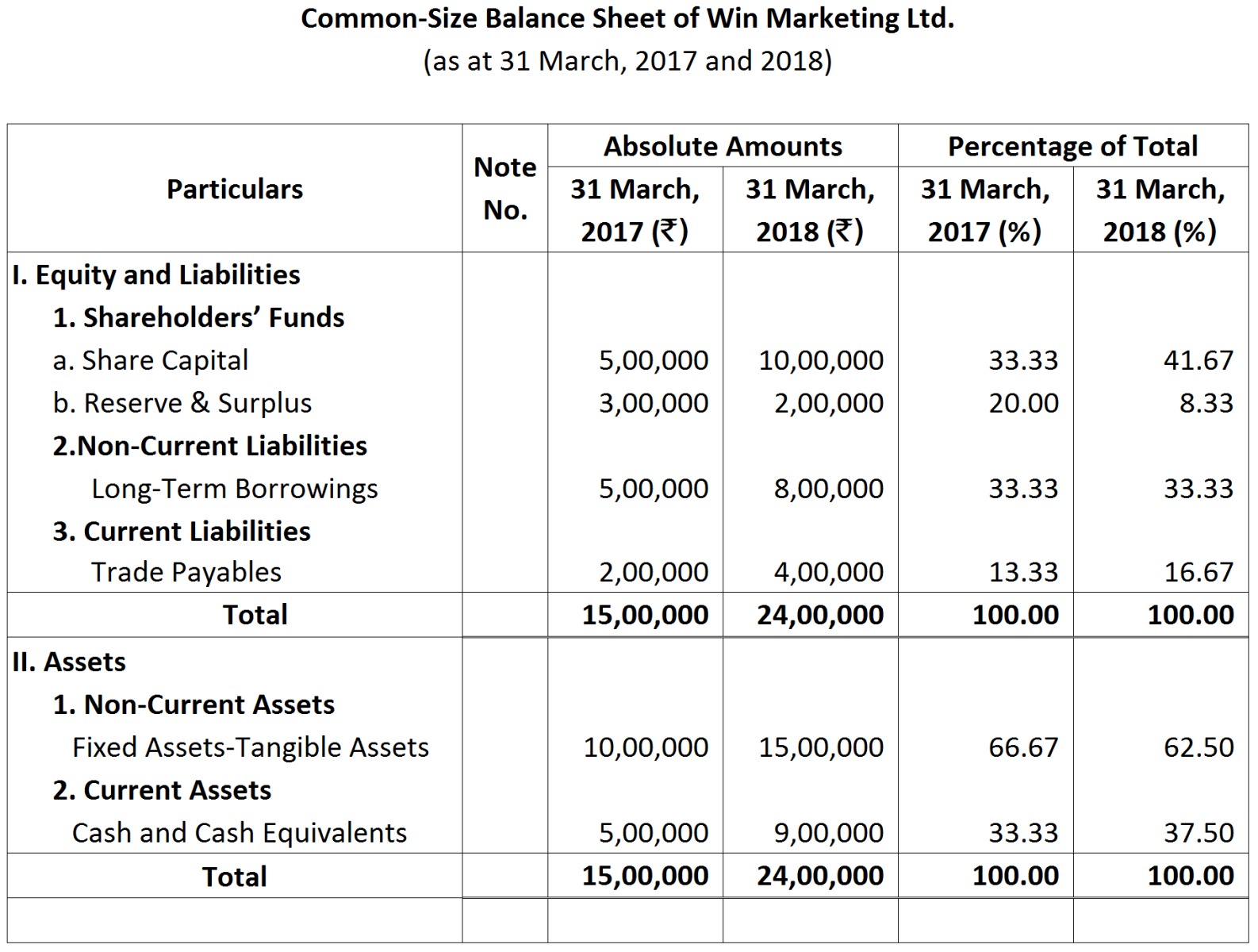

From the above Common-size Balance Sheet as at 31st March, 2018, compute current Ratio, Quick Ratio, Total Assets to Debt Ratio, and Dept to Equity Ratio.