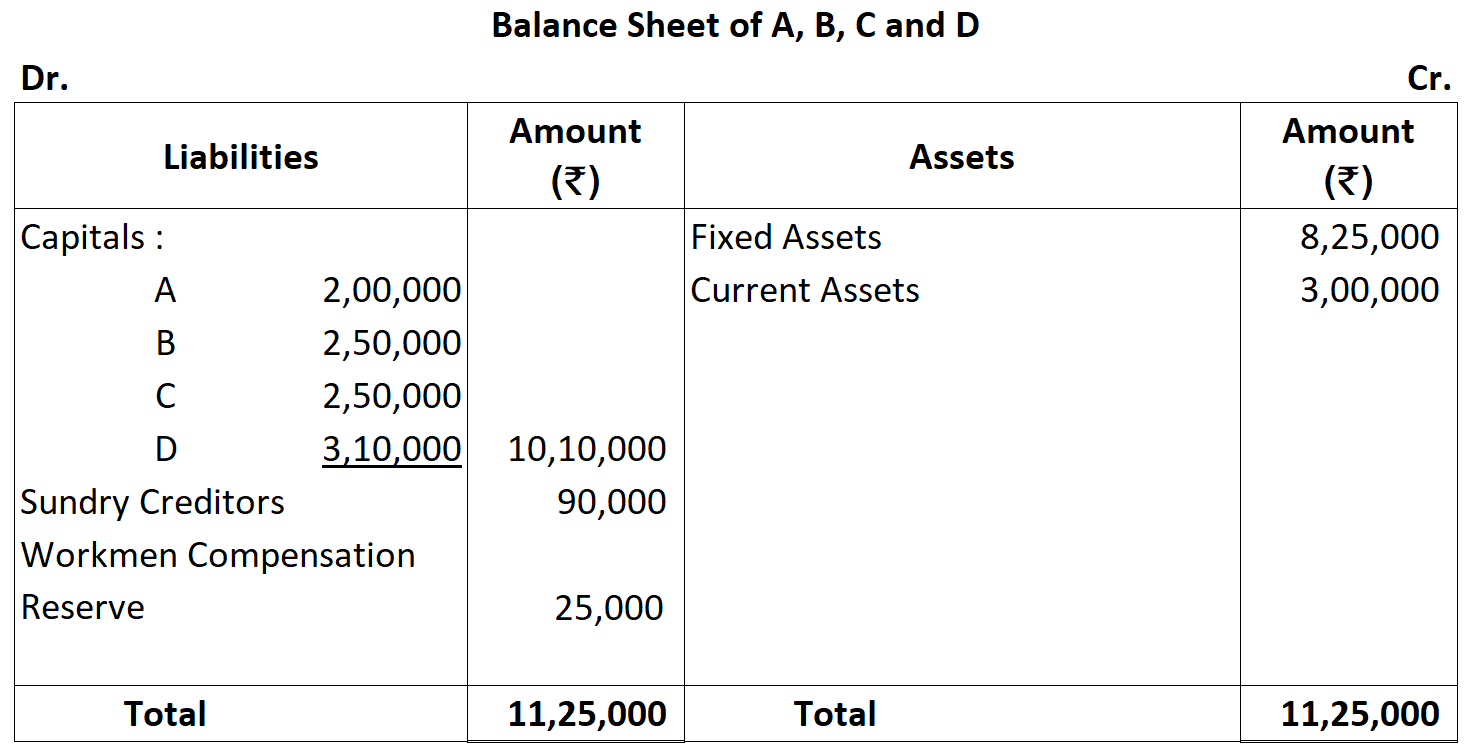

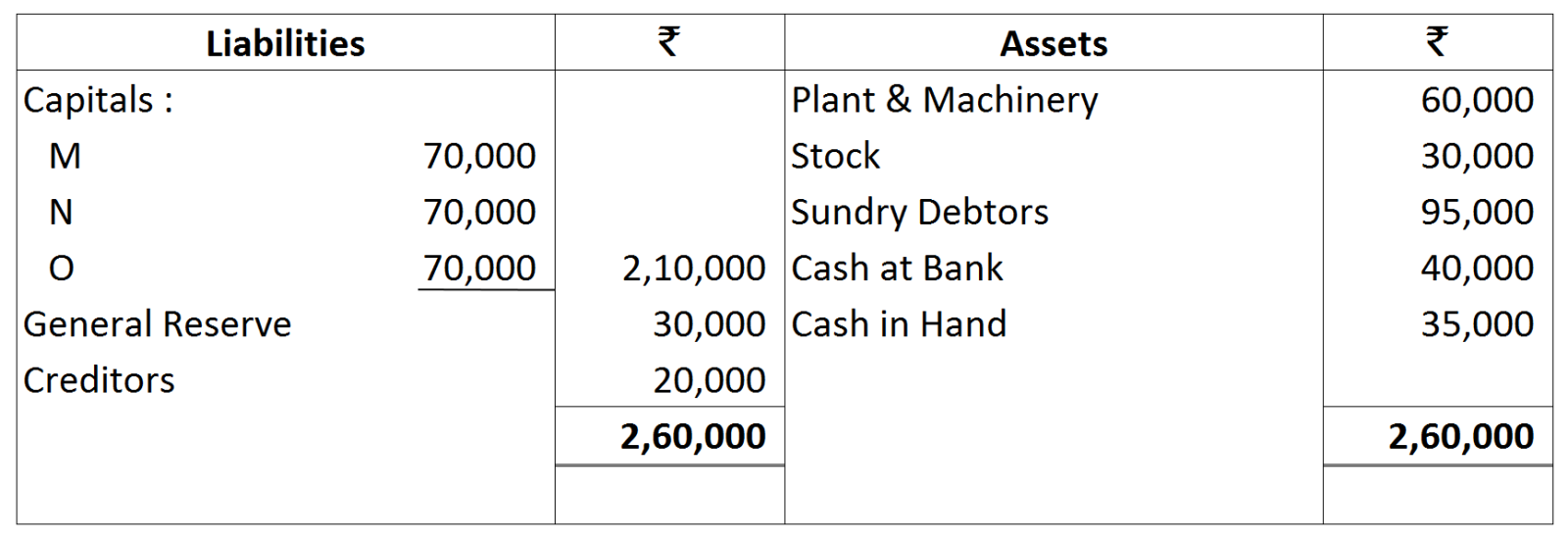

M, N and O were partners in a firm sharing profits and losses equally. Their Balance Sheet as at 31st March, 2015 was as follows:

N died on 12th June, 2015 According to the Partnership Deed, executors of the deceased partner are entitled to:

- Balance of partner's capital account.

- Interest on Capital @5% p.a.

- Share of goodwill calculated on the basis of twice the average of past three year's profits.

- Share of profits from the closure of the last accounting year till the date of death on the basis of twice the average of three completed year's profits before death.

- As per N's Will, ₹ 50,000 is to be donated to 'Prime Ministers' Clean Ganga Project.

Profits for the years ended 31st March 2013, 2014 and 2015 were ₹ 80,000, ₹ 90,000 and ₹ 1,00,000 respectively. Show the working for deceased partner's share of goodwill and profits till the date of his death. Pass the necessary journal entries and prepare N's Capital Account to be rendered to his executors. Also mention the values in the question.