Question

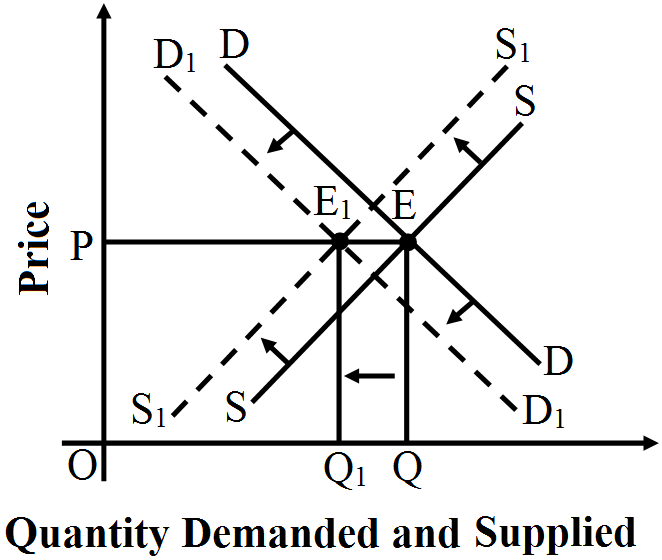

What would be an effect on equilibrium price and equilibrium quantity if demand and supply both fall at the same rate?

OR

Market for a good is in equilibrium. There is simultaneous "decrease" both in demand and supply but there is no change in market price. Explain with the help of a schedule how is it possible.

OR

Market for a good is in equilibrium. There is simultaneous "decrease" both in demand and supply but there is no change in market price. Explain with the help of a schedule how is it possible.