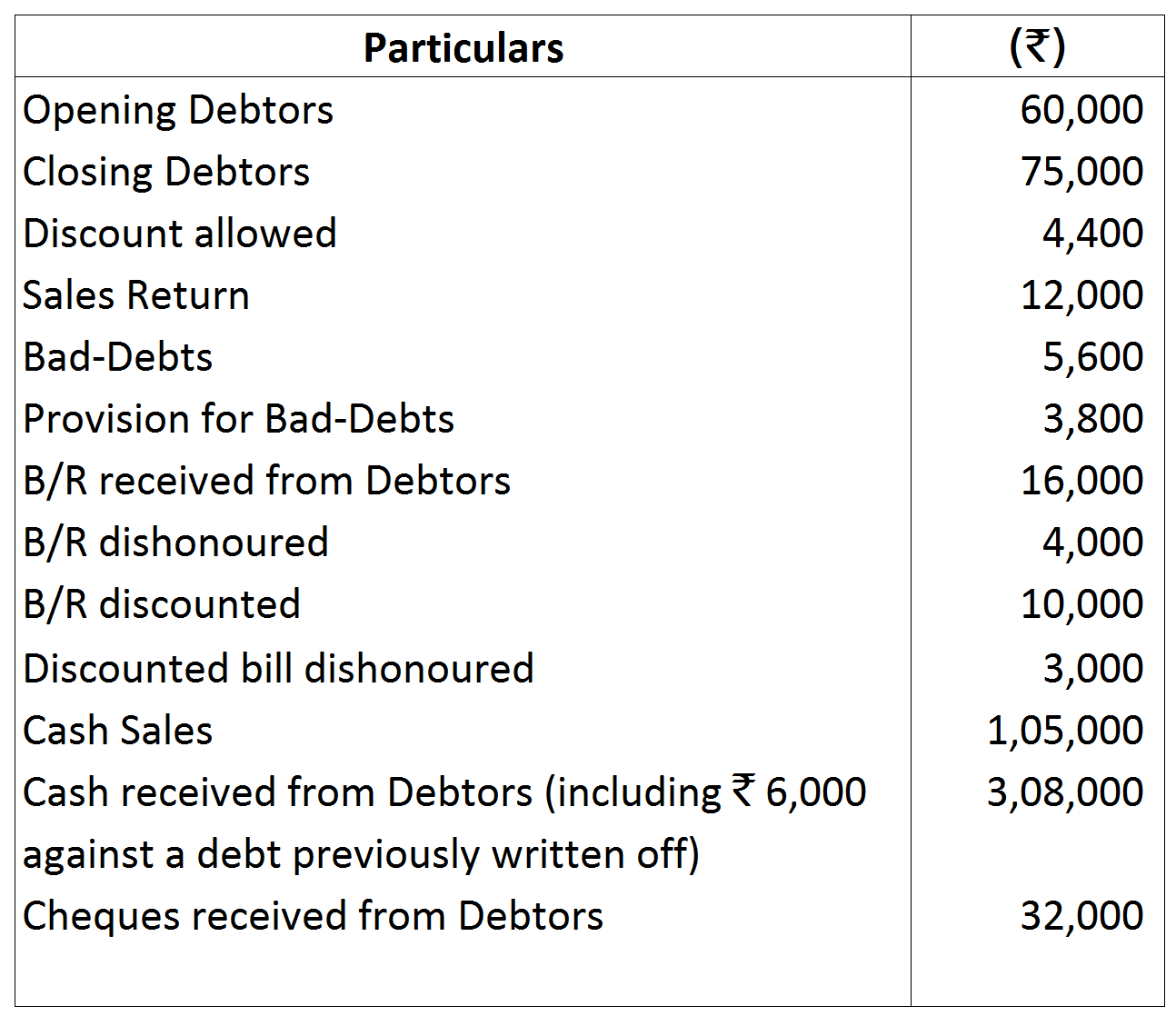

Question 13 Marks

From the details given below find out the Credit Sales and Total Sales:

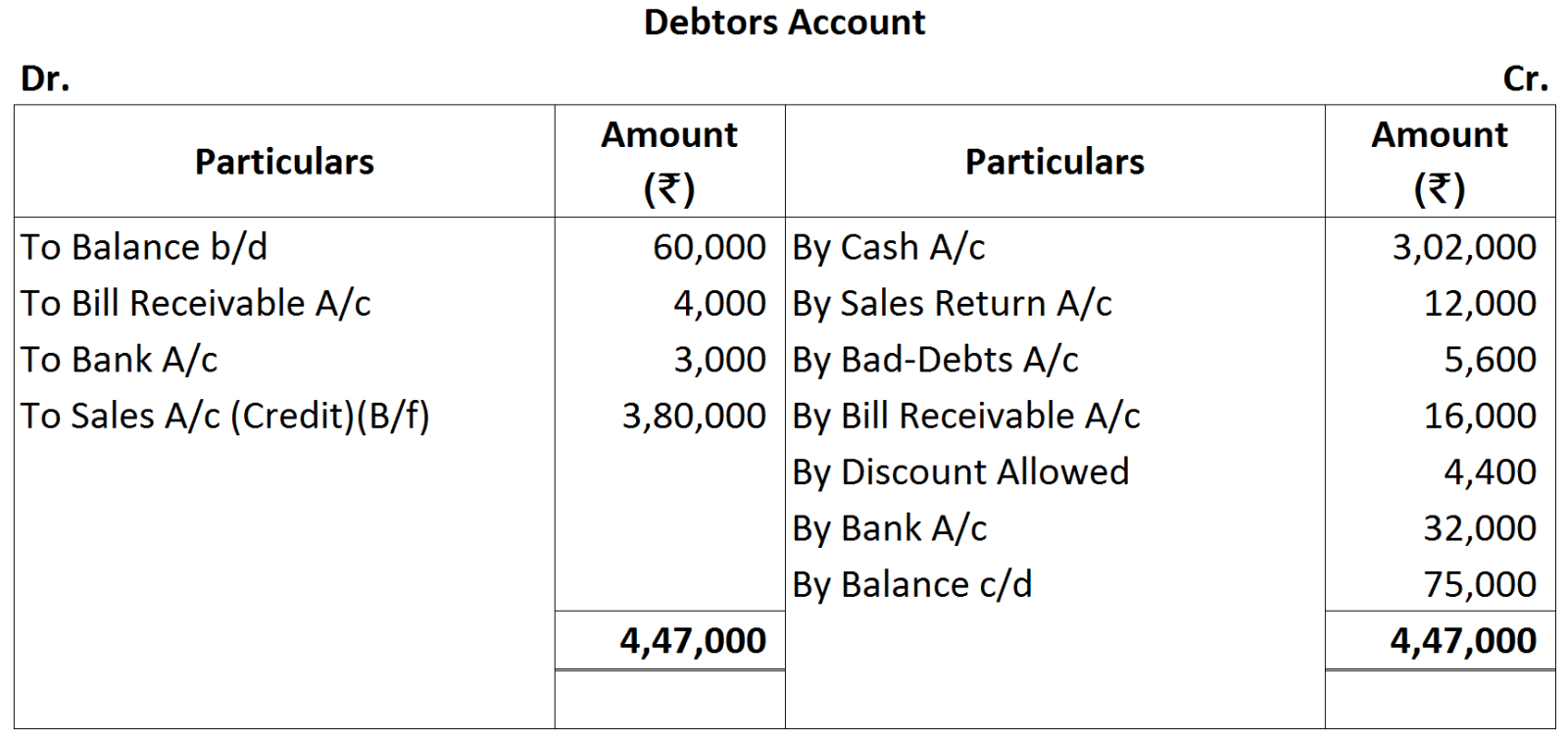

Answer

Total Sales = Cash Sales + Credit Sales

Total Sales = Cash Sales + Credit Sales

Total Sales = 1,05,000 + 3,80,000 = 4,85,000

View full question & answer→Total Sales = Cash Sales + Credit SalesTotal Sales = 1,05,000 + 3,80,000 = 4,85,000