Question 16 Marks

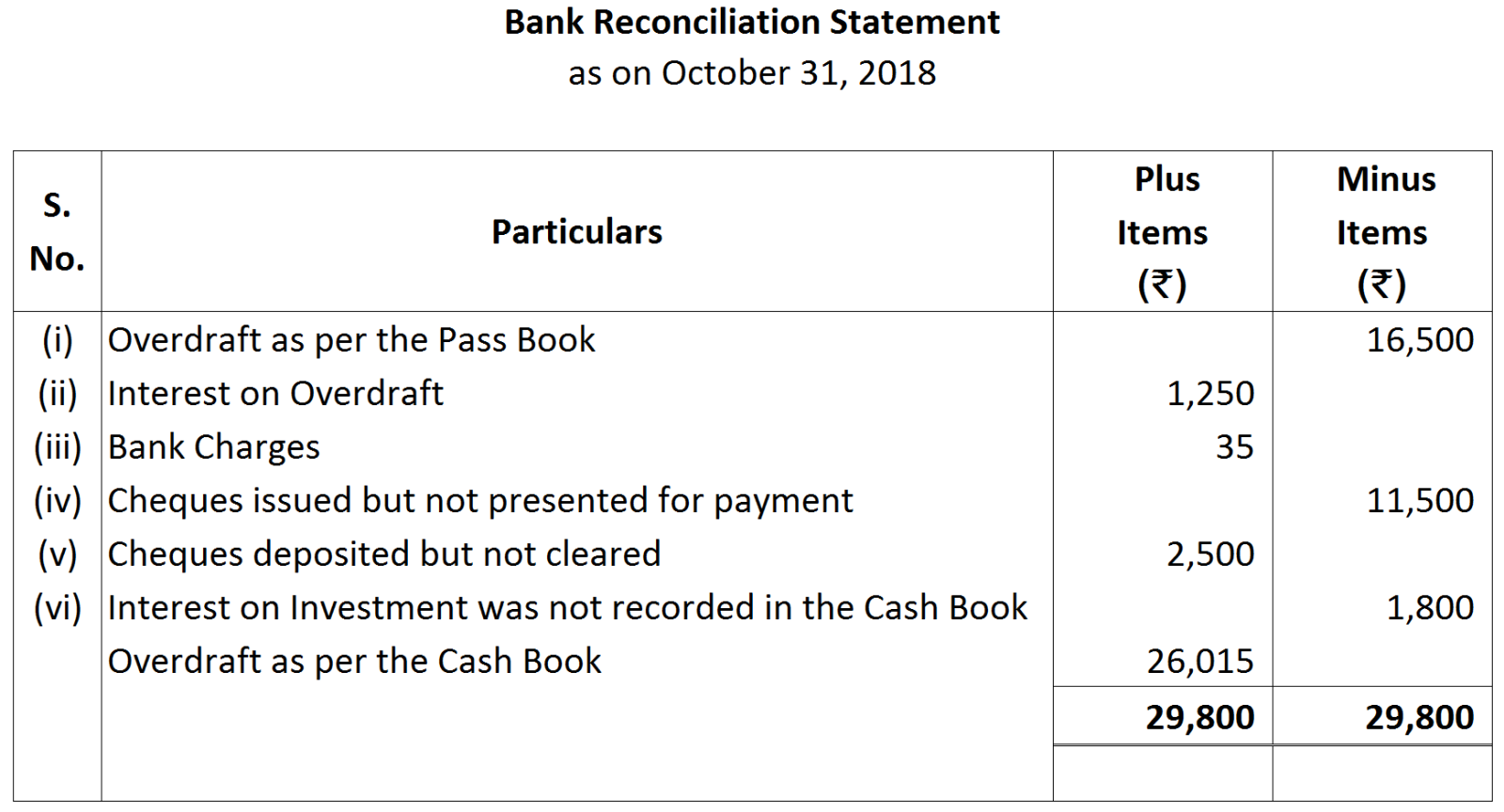

Raghav & Co. have two bank accounts. Account No. I and Account No. II. From the following particulars relating to Account No. I, find out the balance on that account of March 31, 2017 according to the cash book of the firm.

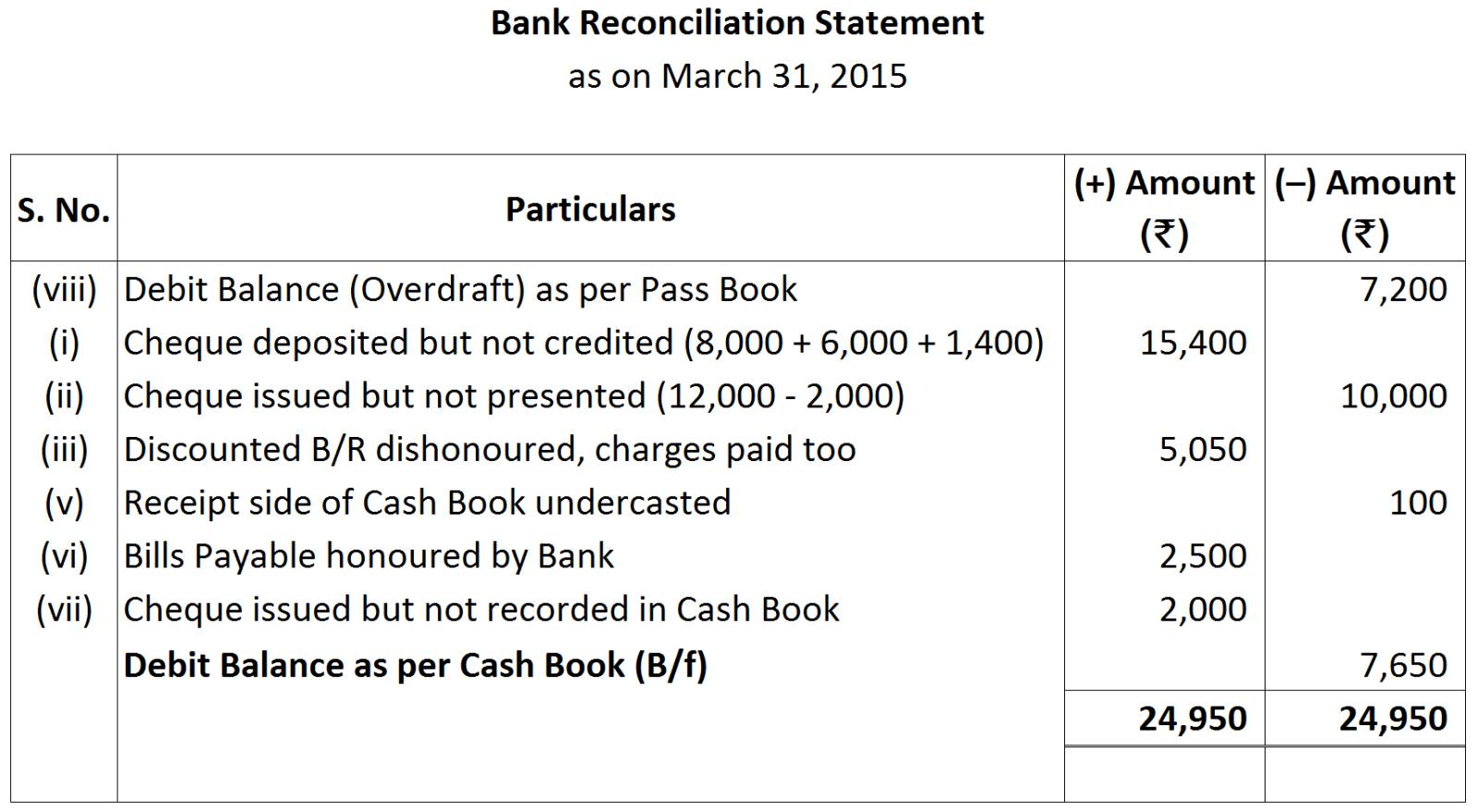

- Cheques paid into bank prior to March 31, 2017, but not credited for ₹ 10,000.

- Transfer of funds from account No. II to account no. I recorded by the bank on March 31, 2017 but entered in the cash book after that date for ₹ 8,000.

- Cheques issued prior to March 31, 2017 but not presented until after that date for ₹ 7,429.

- Bank charges debited by bank not entered in the cash book for ₹ 200.

- Interest Debited by the bank not entered in the cash book ₹ 580.

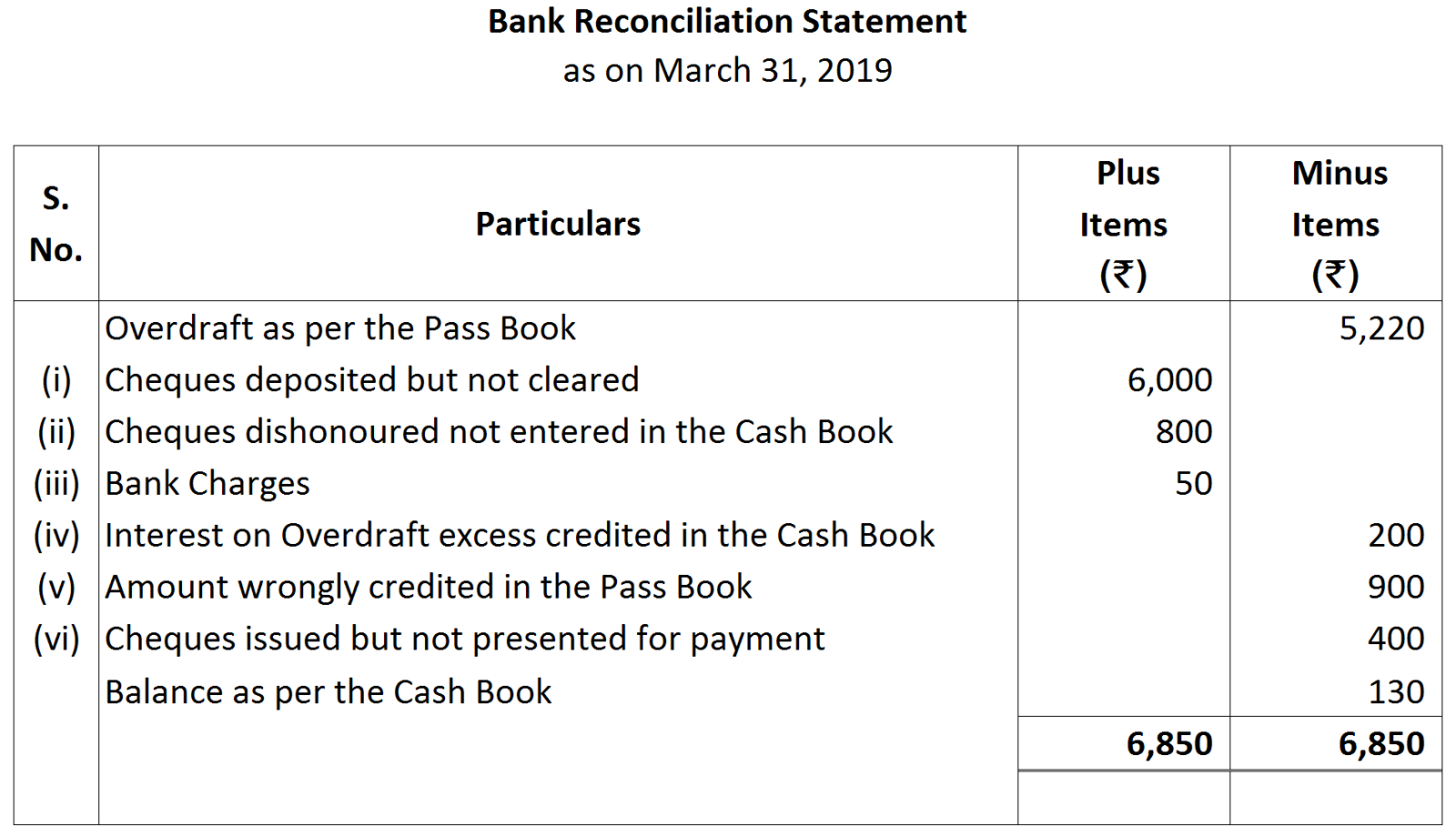

- Overdraft as per Passbook ₹ 18,990.

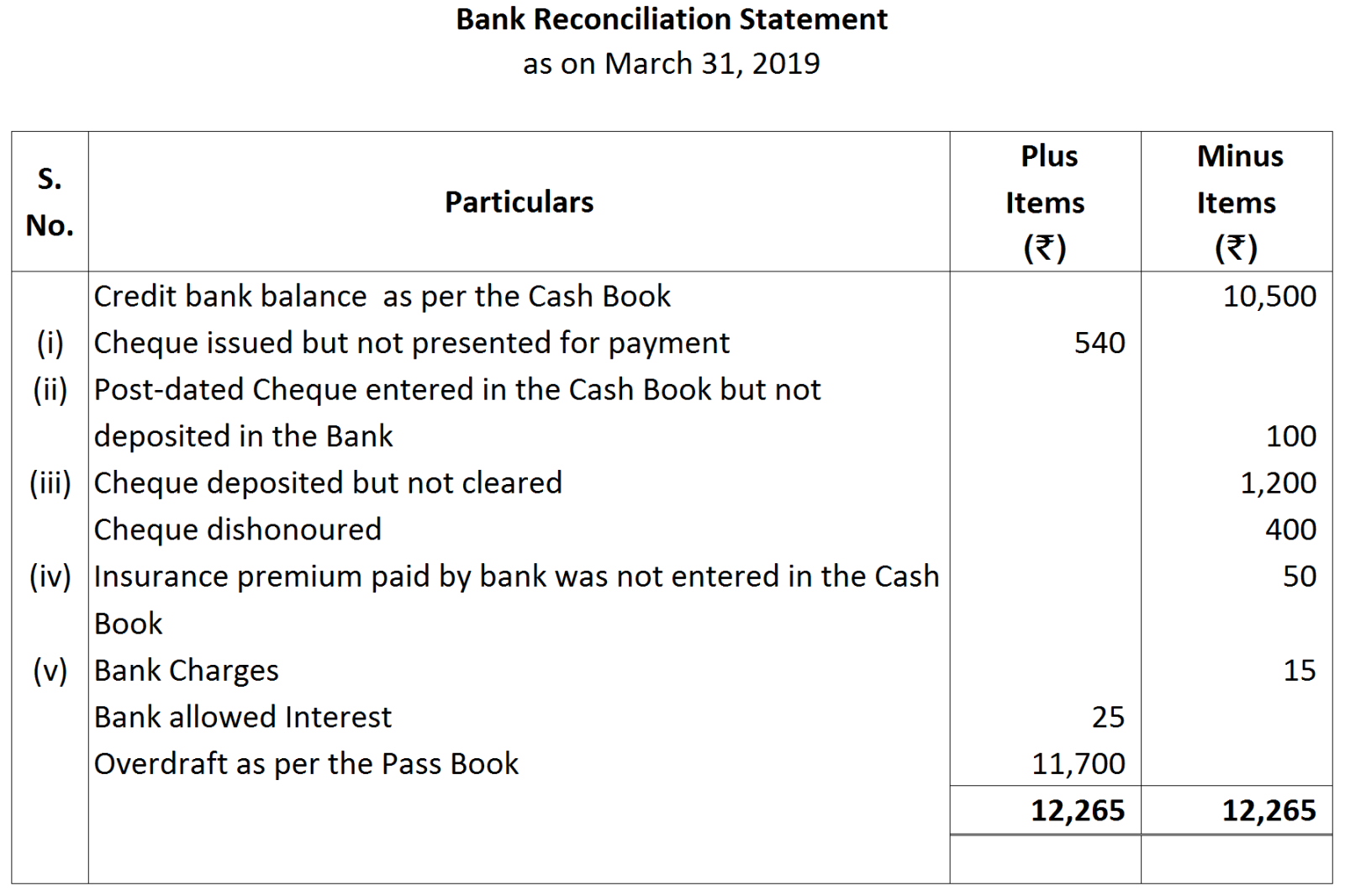

Note: Cheque dated 15th April, 2019 issued to M & Co. dishonoured will have no impact as this statement is as on 31st March 2019.

Note: Cheque dated 15th April, 2019 issued to M & Co. dishonoured will have no impact as this statement is as on 31st March 2019.

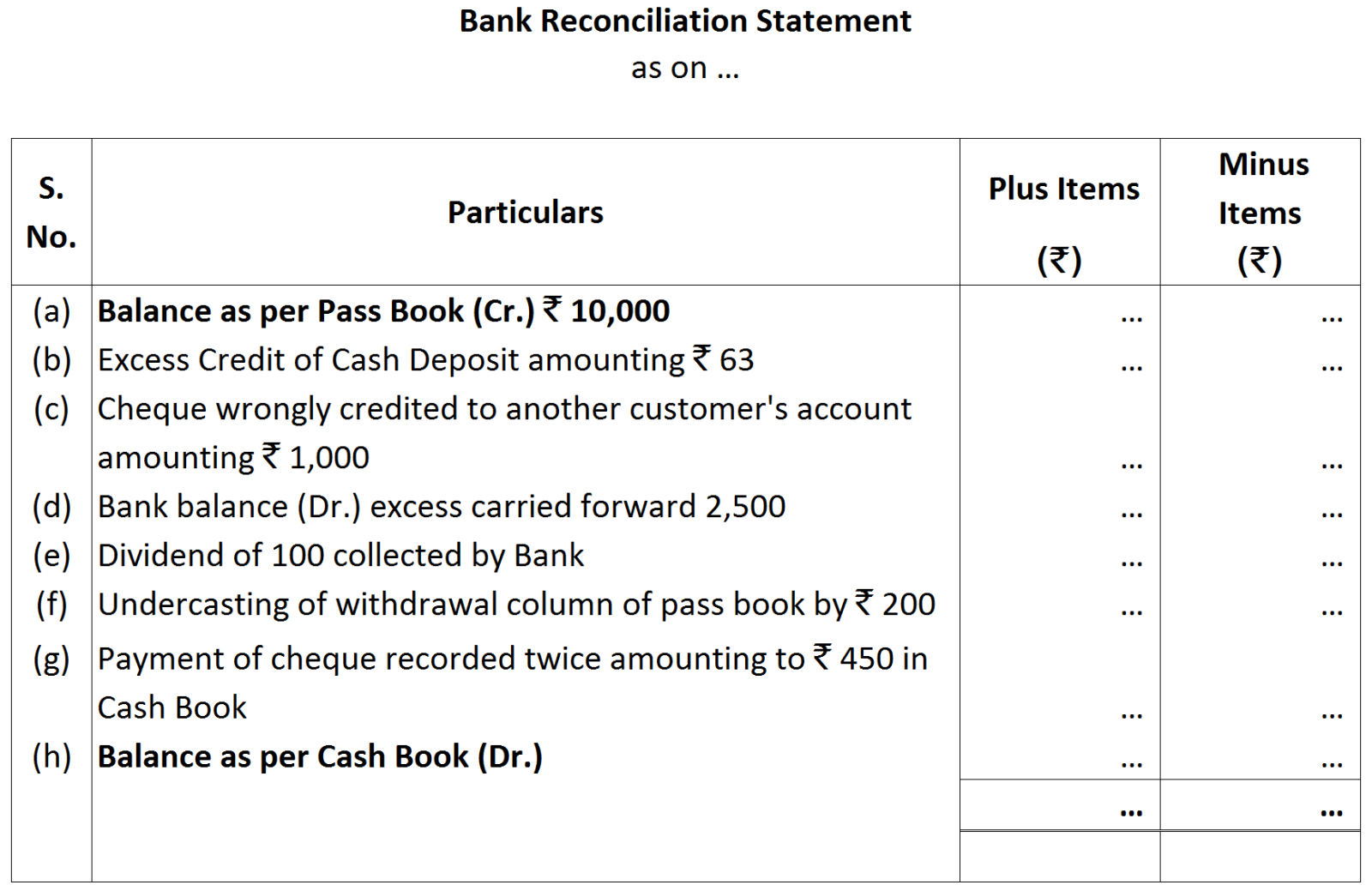

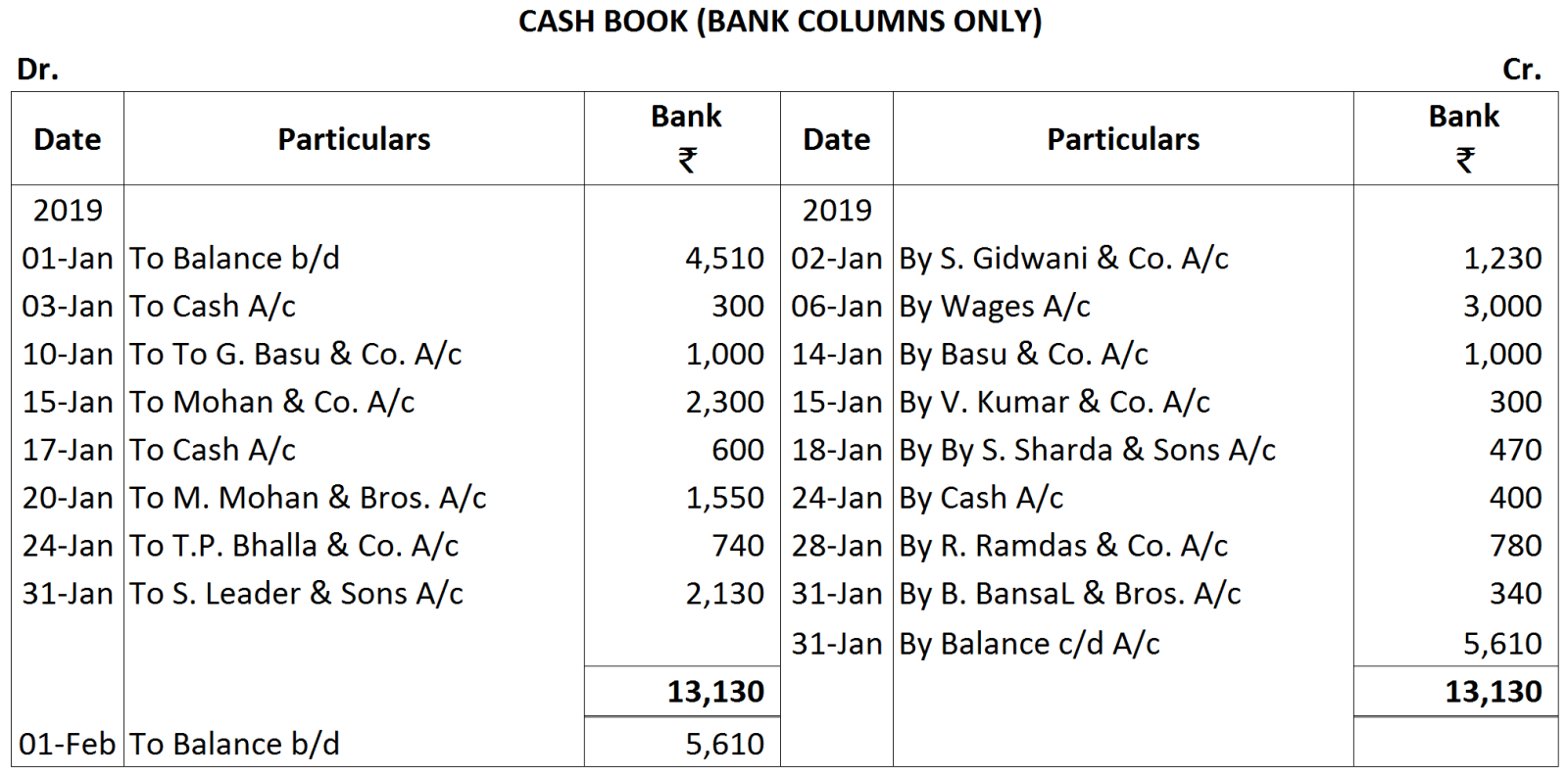

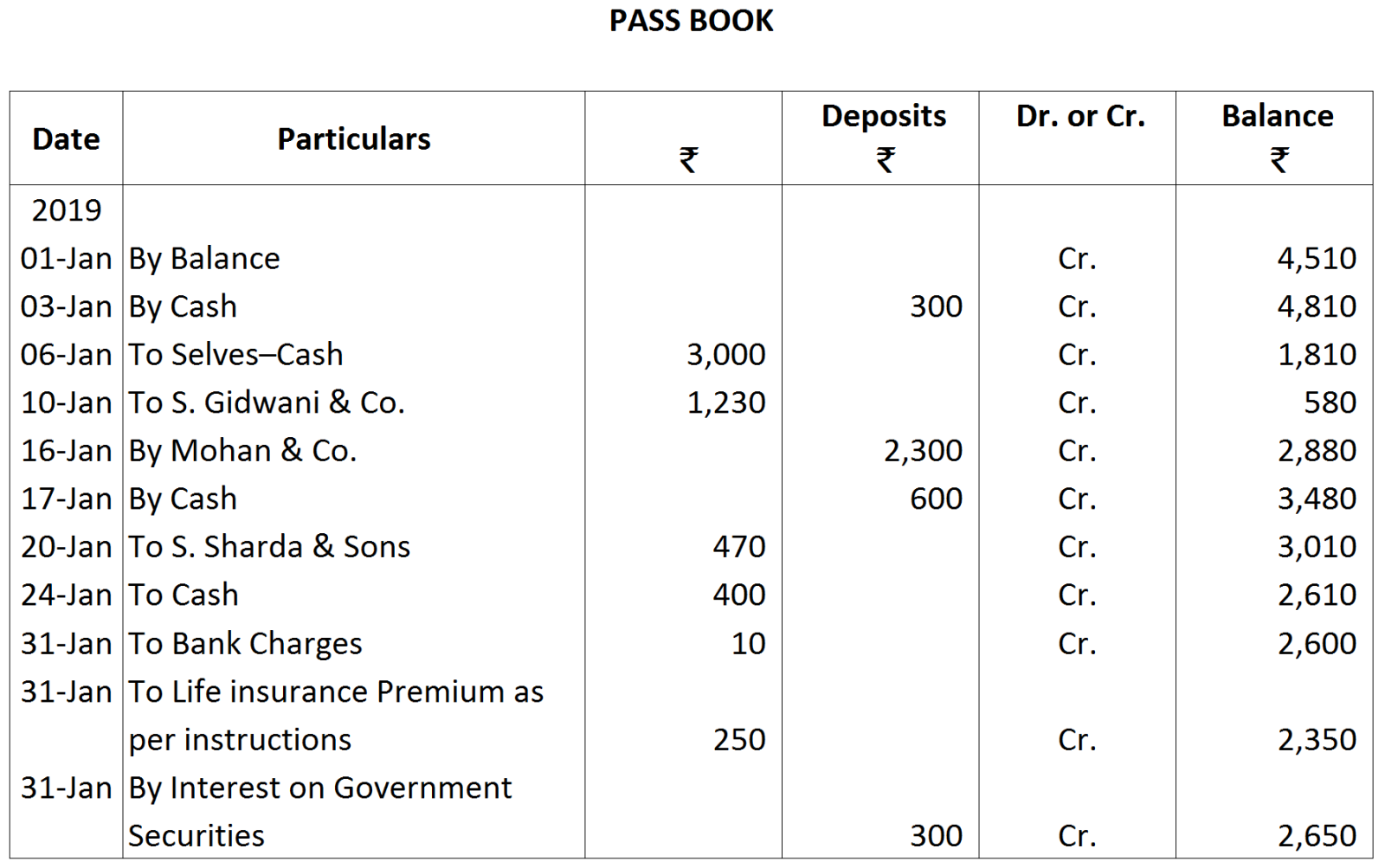

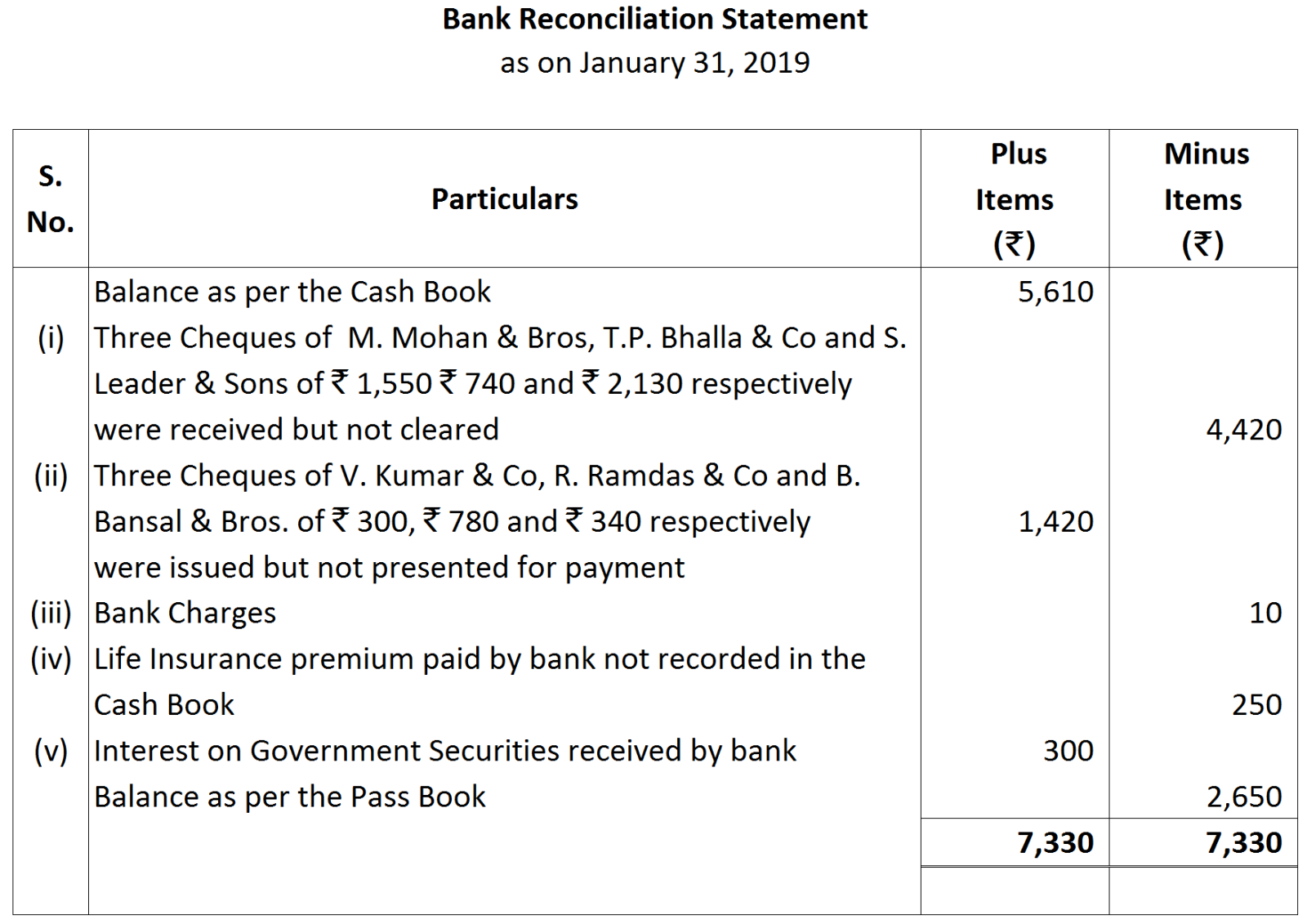

Note: In Cash Book cheque received from G. Basu & Co is debited with ₹ 1,000 and at the time of dishonour entry is reversed by crediting G. Basu & Co with ₹ 1,000. Therefore its net effect is nil in Cash Book.

Note: In Cash Book cheque received from G. Basu & Co is debited with ₹ 1,000 and at the time of dishonour entry is reversed by crediting G. Basu & Co with ₹ 1,000. Therefore its net effect is nil in Cash Book. Note:

Note: \

\

Note: Overdraft balance has credit balance but taken as debit balance, so to correct the error credit cash book by double amount.

Note: Overdraft balance has credit balance but taken as debit balance, so to correct the error credit cash book by double amount. Note: Point (vii) will have no affect on the statement as error in recording cash deposit entry is already rectified.

Note: Point (vii) will have no affect on the statement as error in recording cash deposit entry is already rectified.