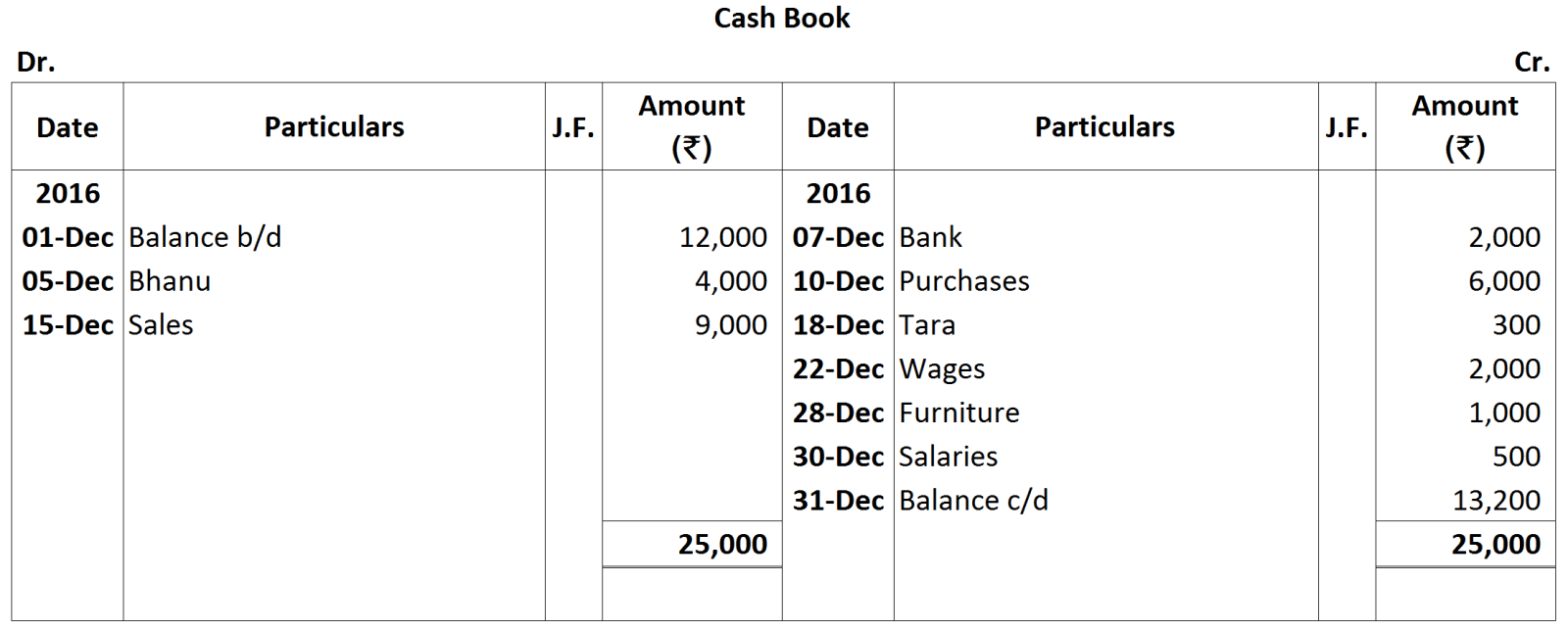

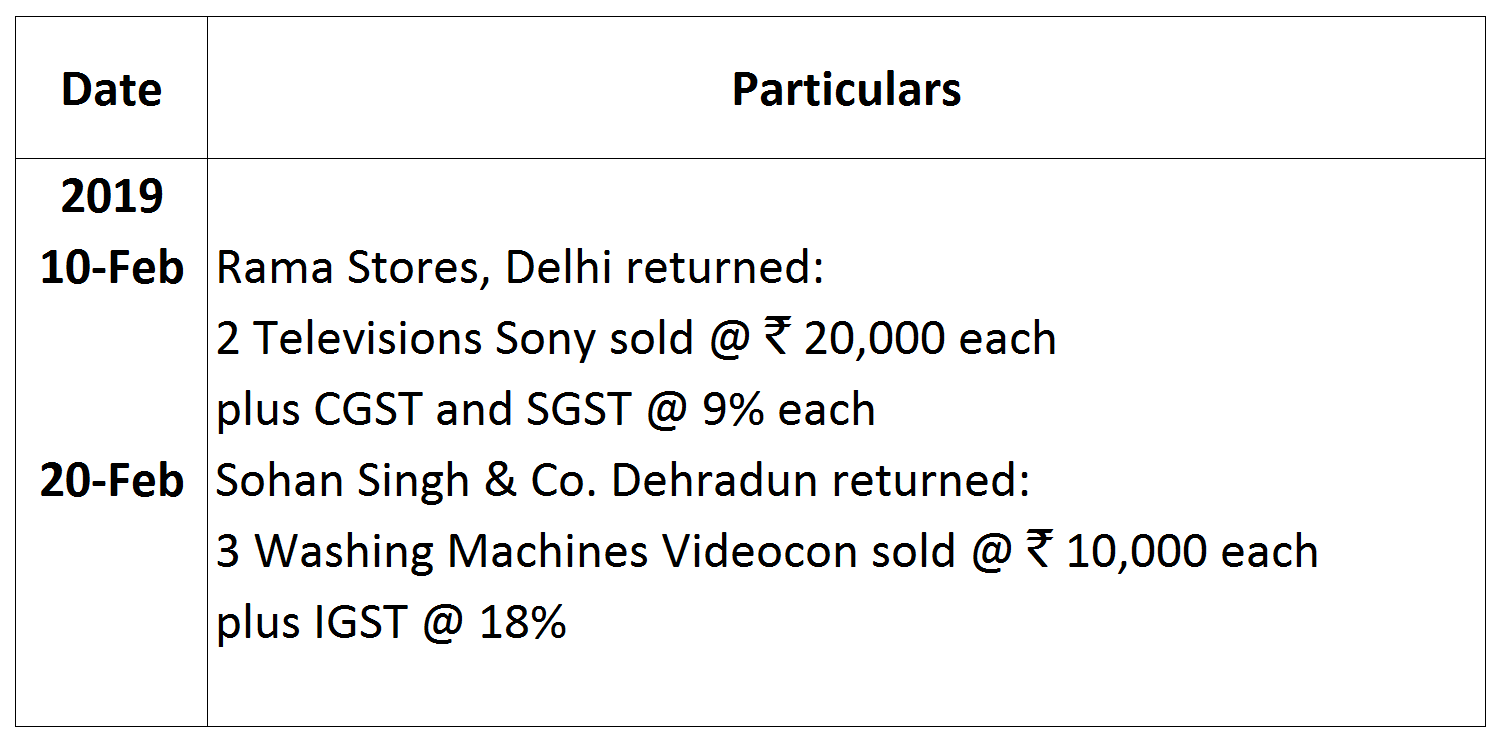

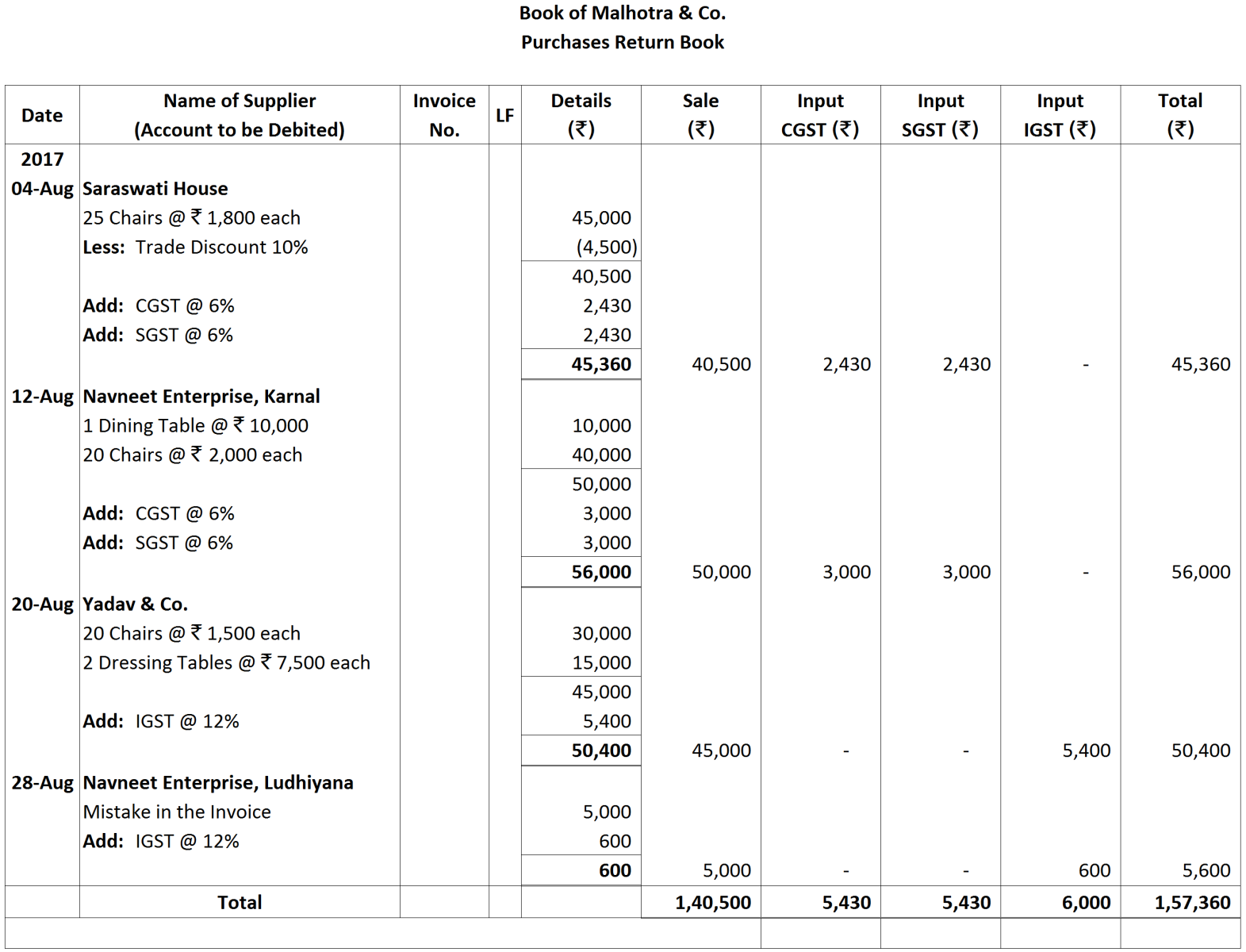

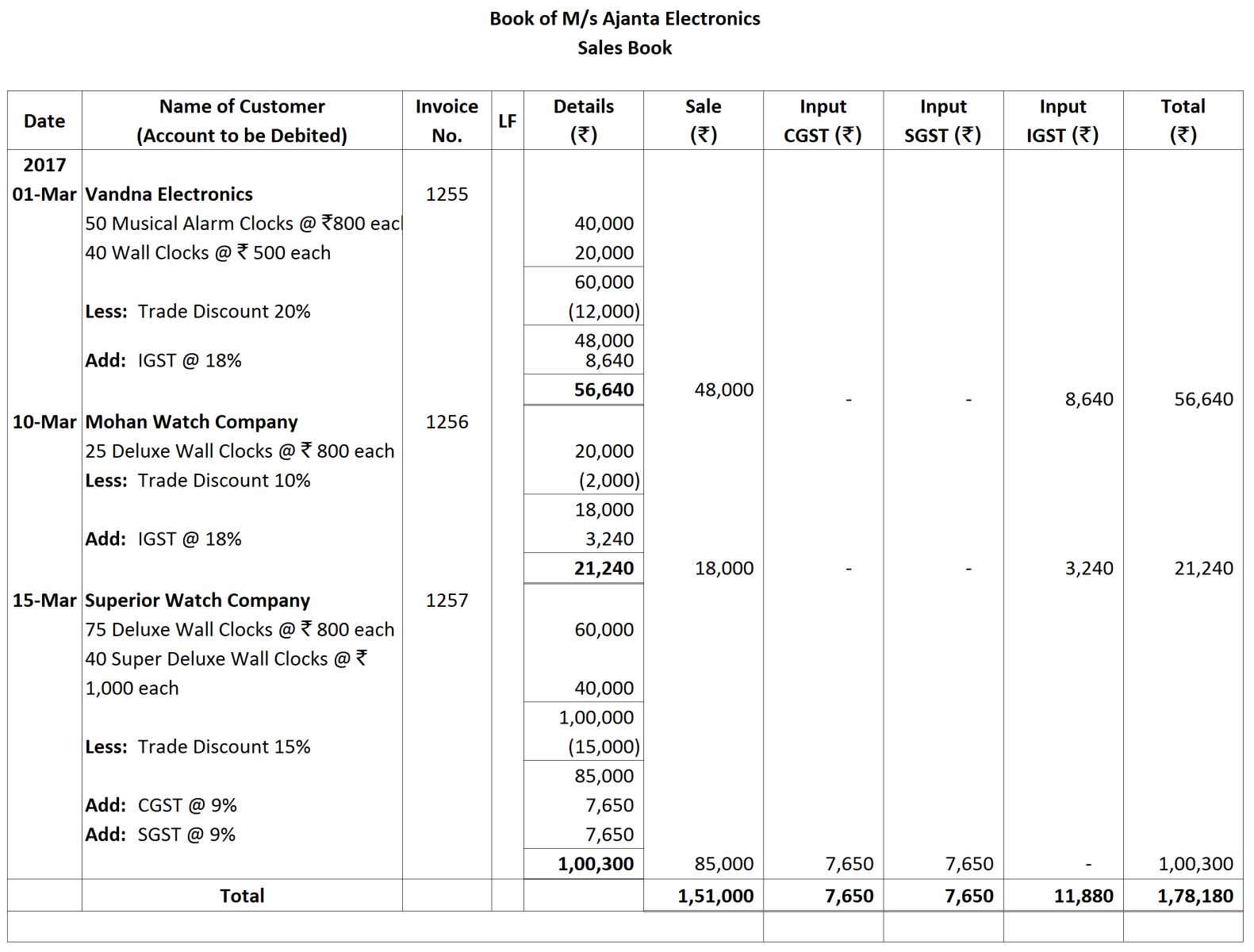

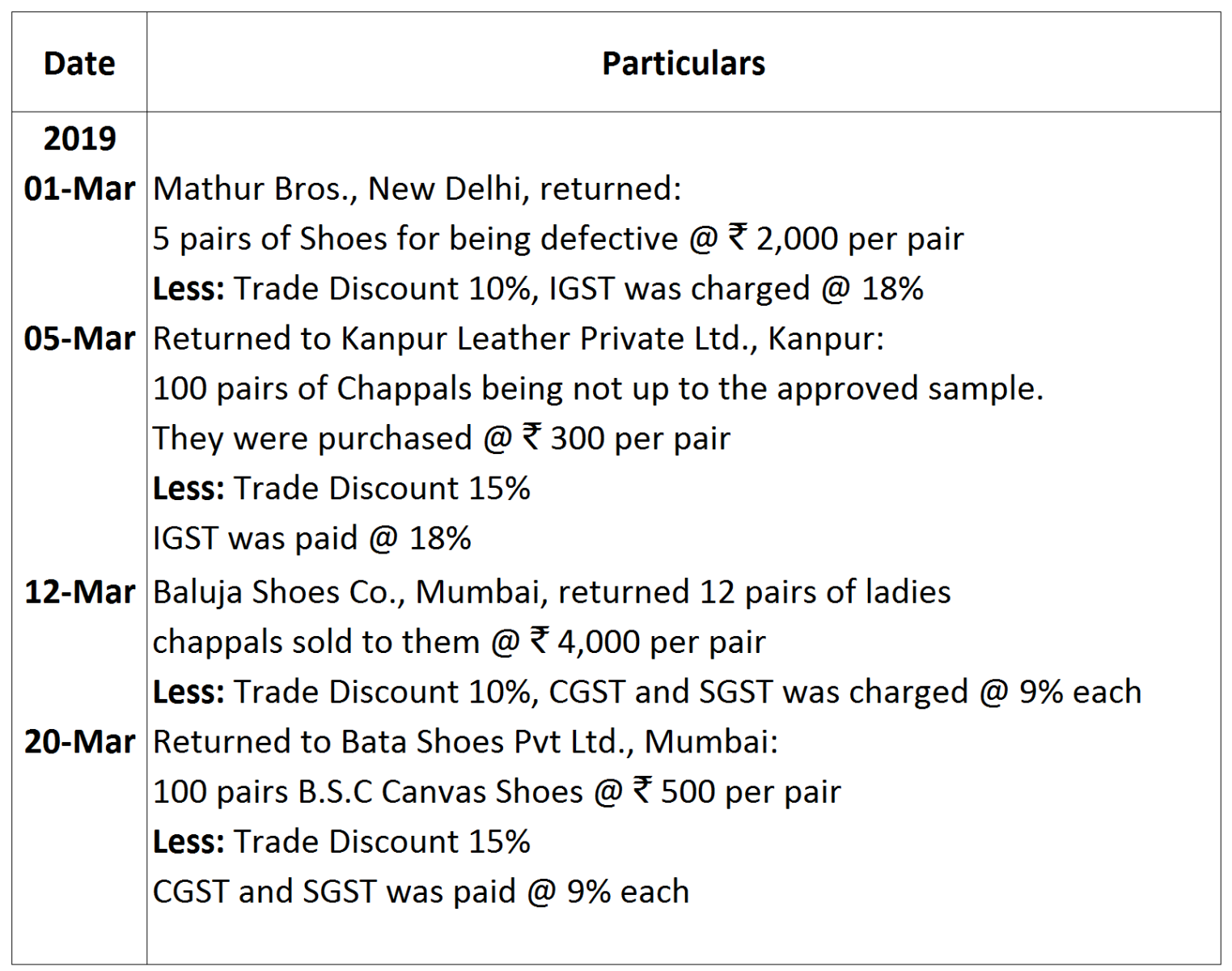

Question 14 Marks

Name the books of original entry where the following transactions will be recorded with reasons thereof:

| a | Goods Purchased from Ram Lal ₹ 5,000 on credit. |

| b | Provision for doubtful debts created @ 5% on debtors with book value of ₹ 10,000. |

| c | Defective goods sold to Babita on credit worth ₹ 4,000 were returned by her. |

| d | Purchased furniture on credit from Mr. Ratan Singh for ₹ 15,000 for use in the business. |

Answer

View full question & answer→|

Transactions

|

Books of Original Entry

|

Reason

|

|

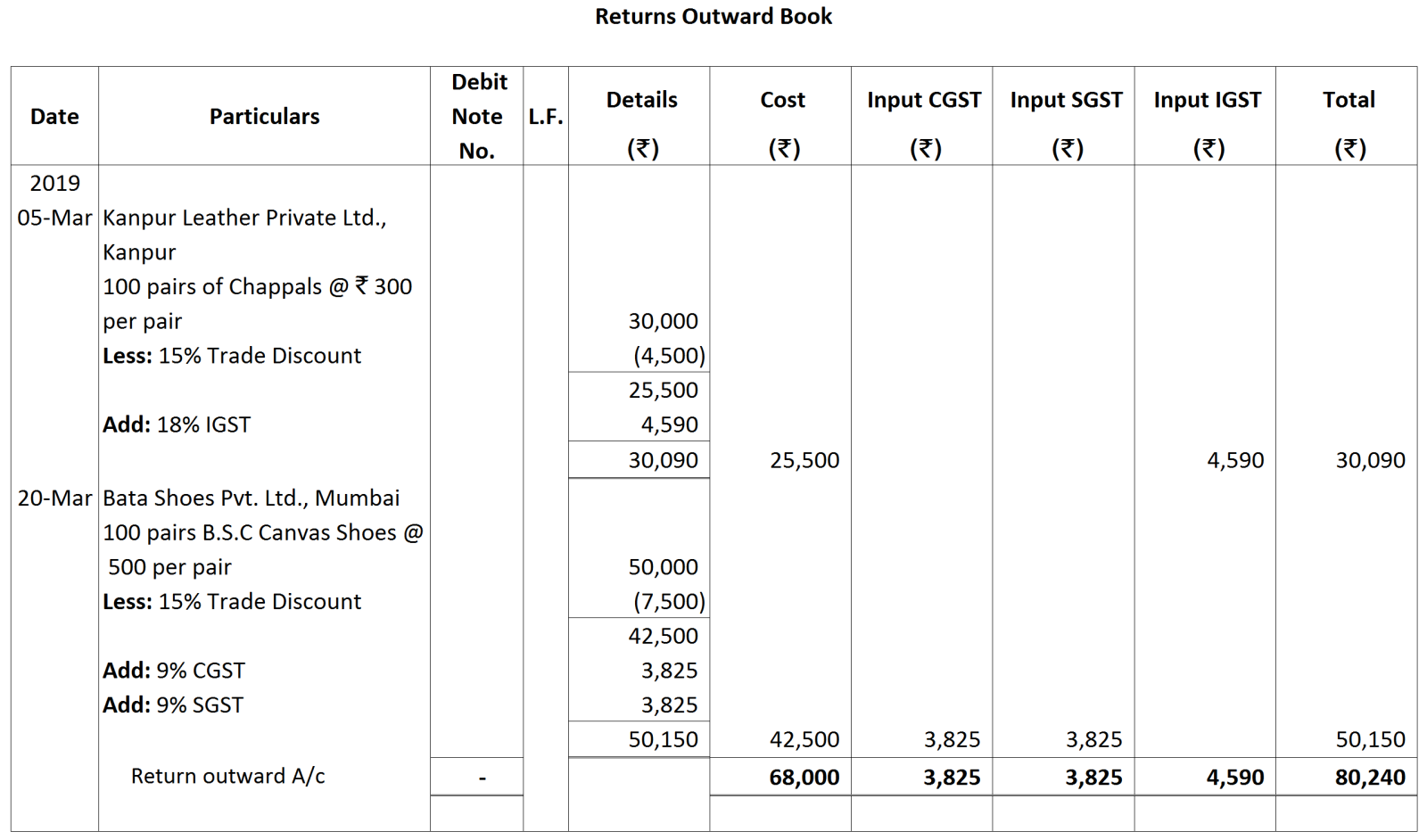

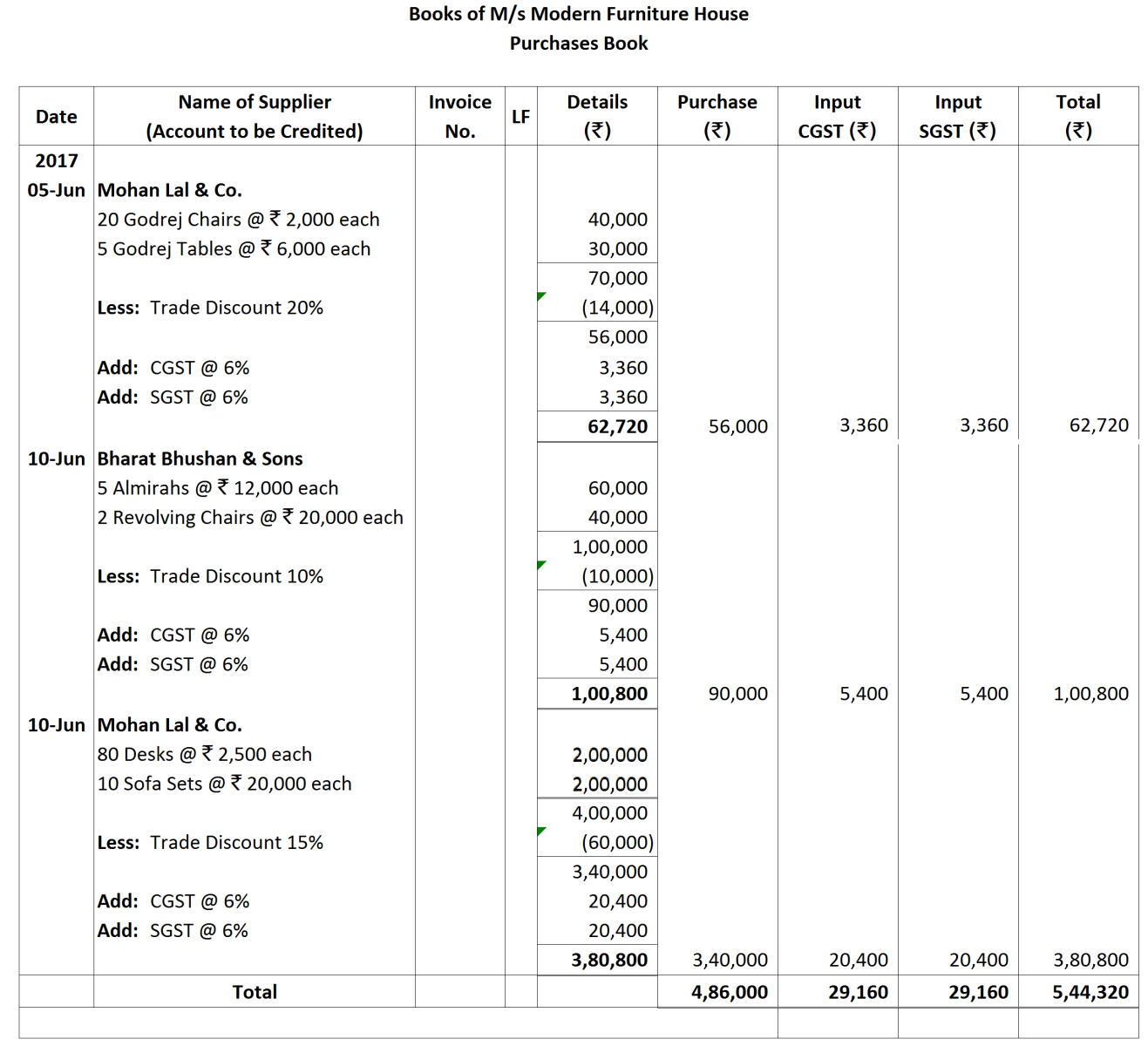

Goods purchased from Ram Lal @ ₹ 5,000 on credit.

|

Purchases Book

|

Purchases book records only credit purchase of goods.

|

|

Provision for doubtful debts created @ 5% on debtors with book value of ₹ 10,000

|

Journal Proper

|

Provision for doubtful debts is recorded in journal proper.

|

|

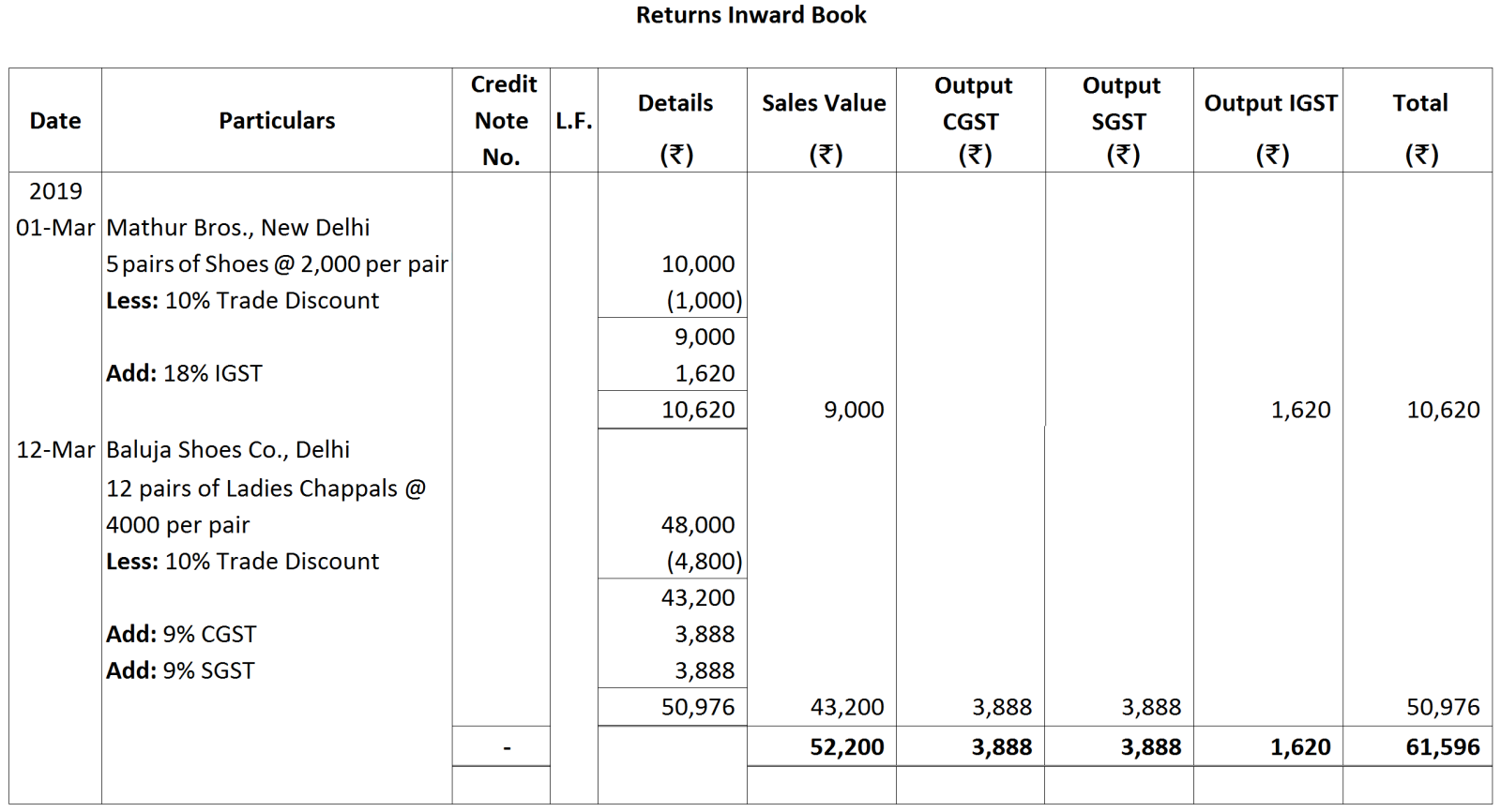

Defective goods sold to Babita on credit worth ₹ 4,000 were returned by her.

|

Sales Return Book

|

Goods returned by customer which were earlier sold on credit are recorded in Sales Return Book.

|

|

Purchased furniture on credit from Mr. Ratan Singh for ₹ 15,000 for use in the business.

|

Journal Proper

|

Purchases book records only credit purchase of goods, so Furniture purchased on credit will be recorded in Journal Proper.

|