Question 13 Marks

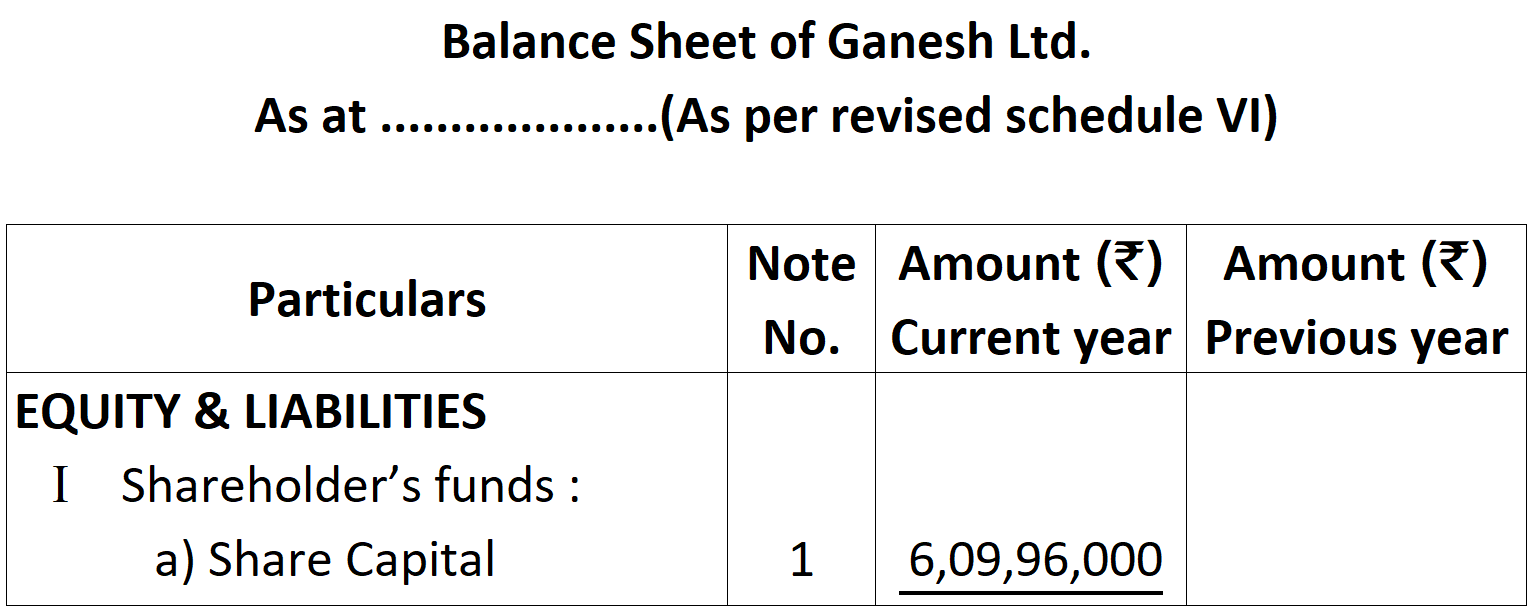

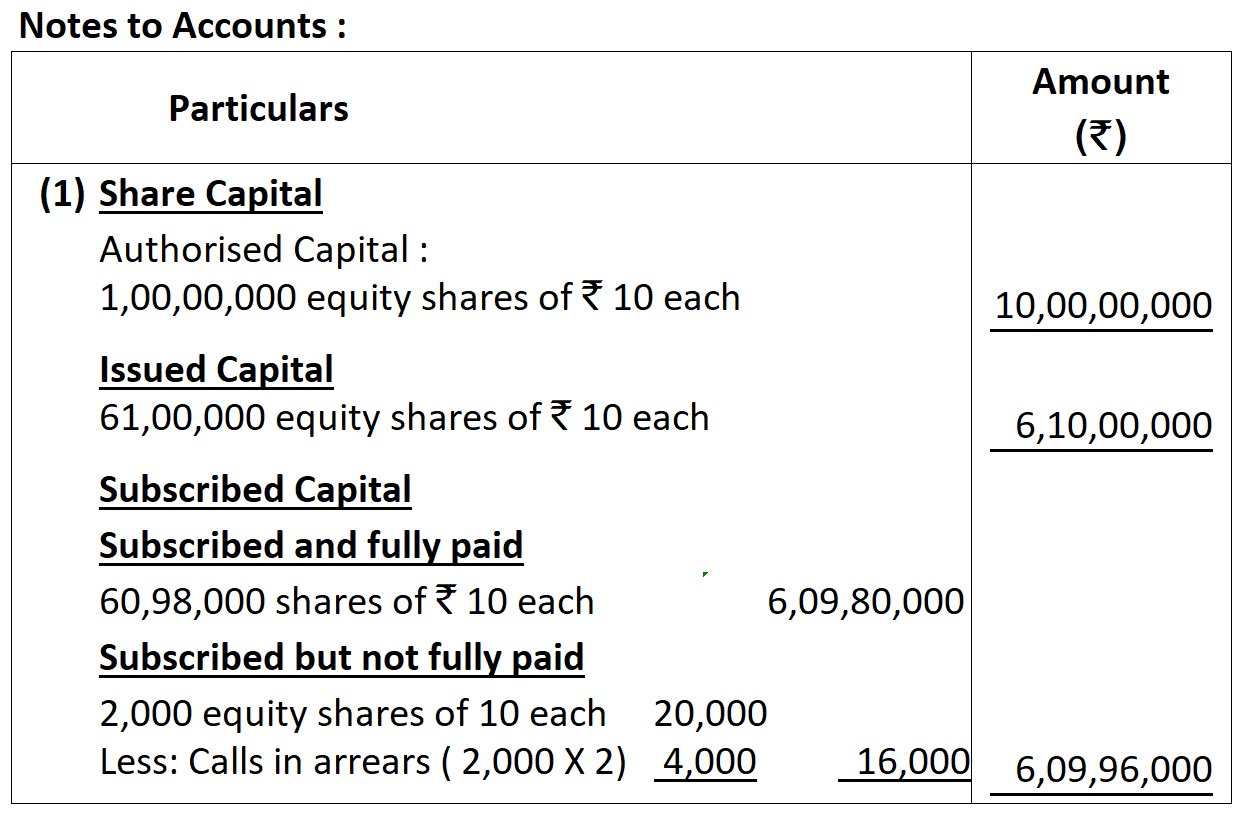

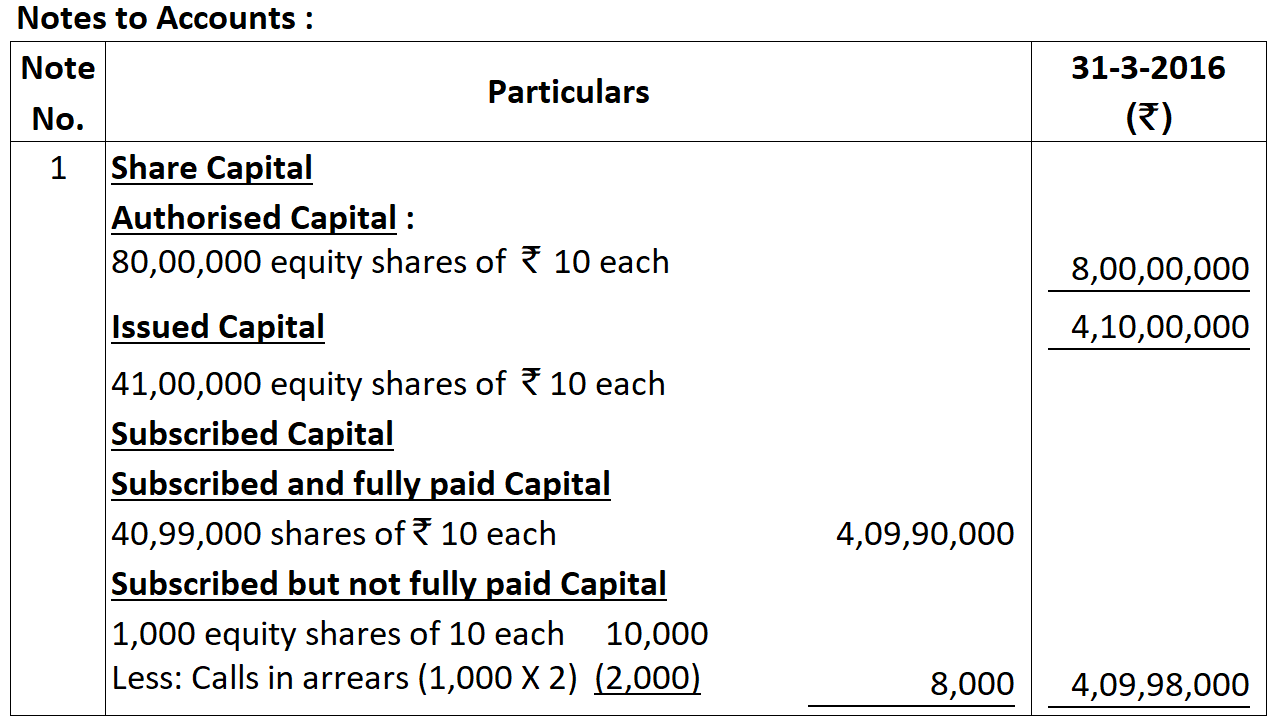

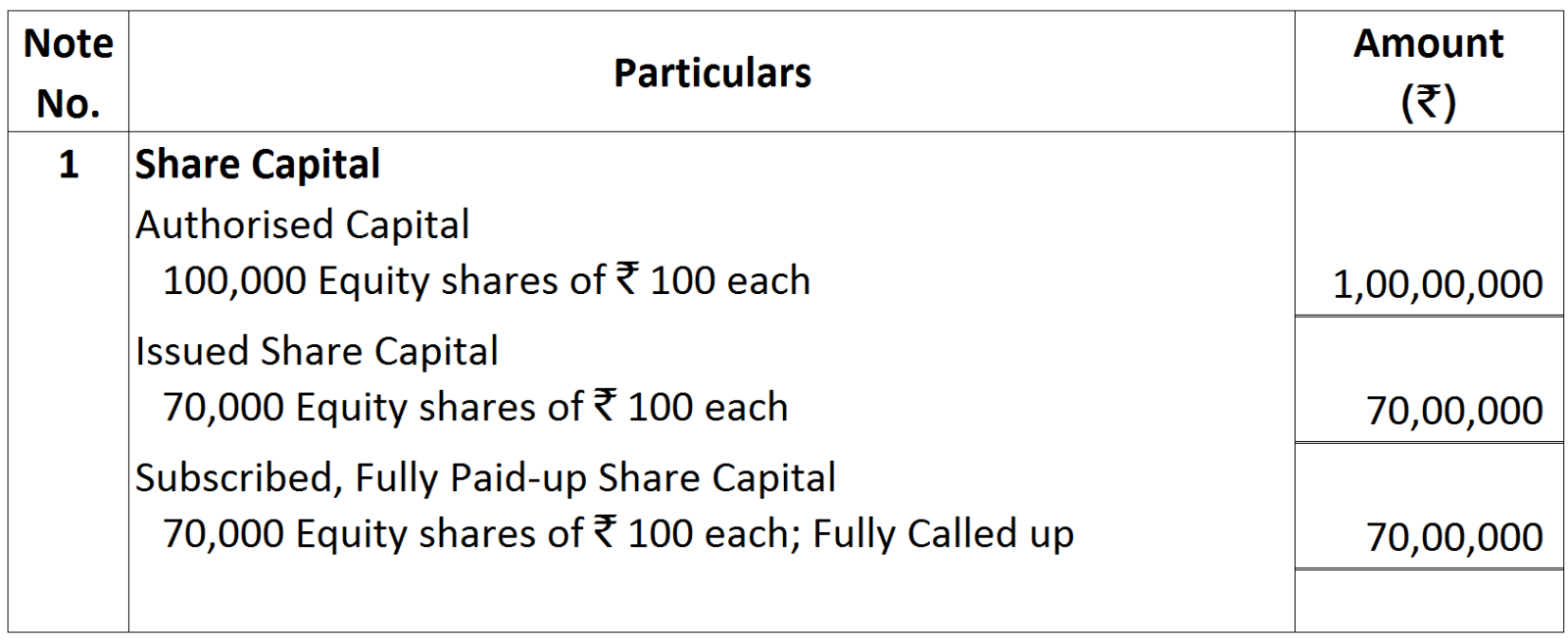

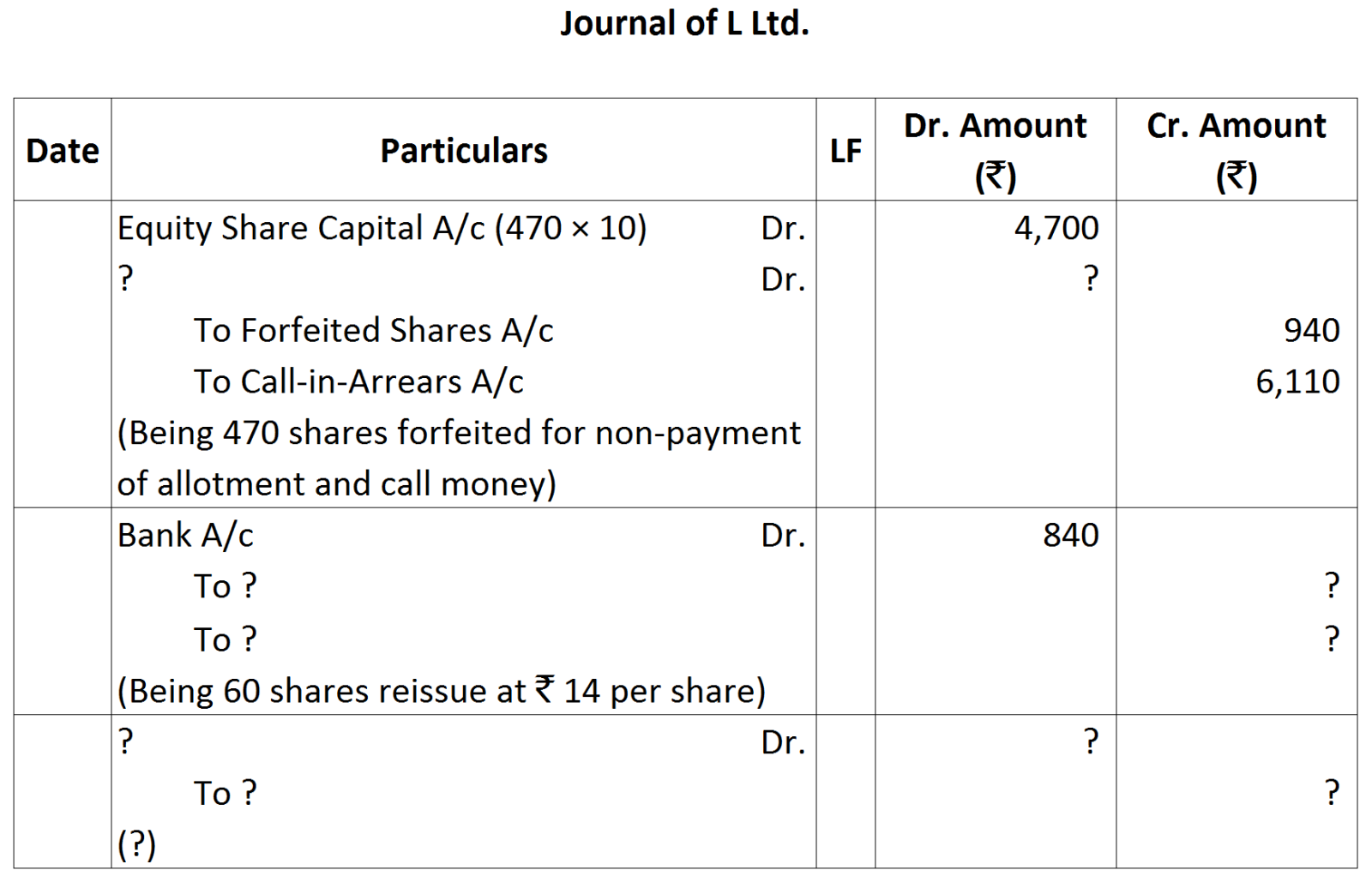

Ganesh Ltd. is registered with an authorised capital of ₹ 10,00,00,000 divided into equity shares of ₹ 10 each. Subscribed and fully paid up capital of the company was ₹ 6,00,00,000. For providing employment to the local youth and for the development of the tribal areas of Arunachal Pradesh the company decided to set up a hydro power plant there. The company also decided to open skill development centres in Itanagar, Pasighat and Tawang. To meet its new financial requirements, the company decided to issue 1,00,000 equity shares of ₹ 10 each and 1,00,000, 9% debentures of ₹ 100 each. The debentures were redeemable after five years at par. The issue of shares and debentures was fully subscribed. A shareholder holding 2,000 shares failed to pay the final call of ₹ 2 per share.

Show the share capital in the Balance Sheet of the company as per the provisions of Schedule III of the Companies Act, 2013. Also identify any two values that the company wishes to propagate.

Show the share capital in the Balance Sheet of the company as per the provisions of Schedule III of the Companies Act, 2013. Also identify any two values that the company wishes to propagate.

Answer

Values:

View full question & answer→Values:

- Providing employment opportunities to the local youth.

- Promotion of development in tribal areas.

- Promotion of skill development in Arunachal Pradesh.

- Paying attention towards regions of social unrest.

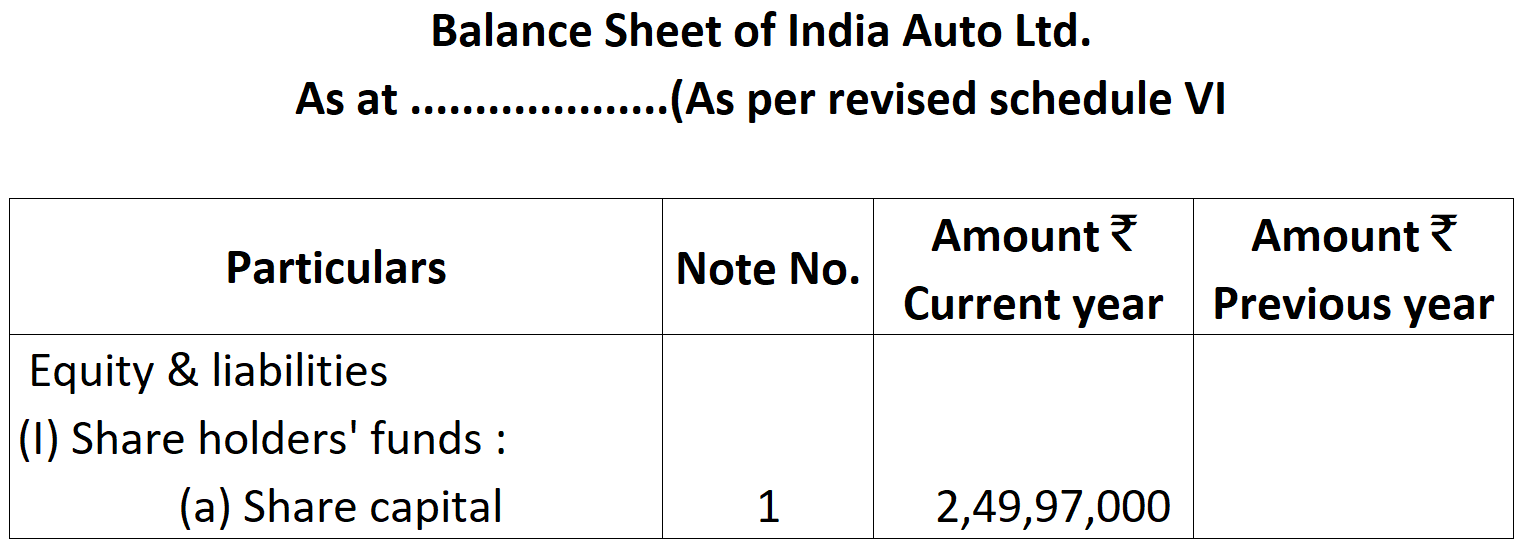

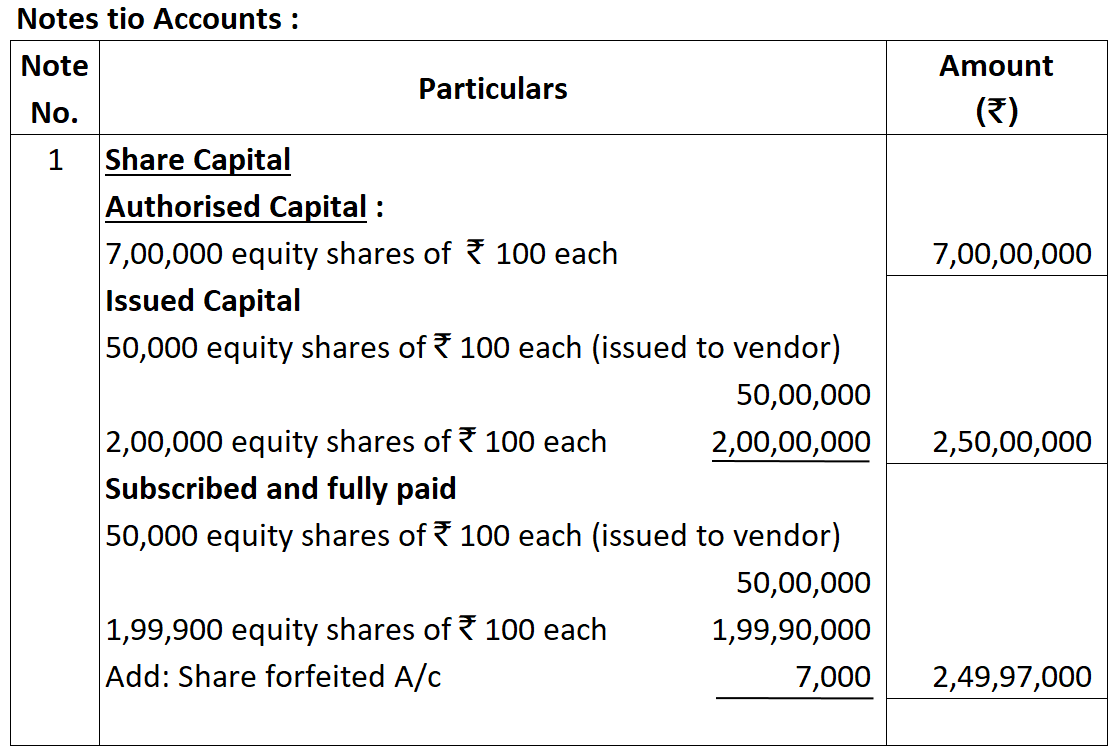

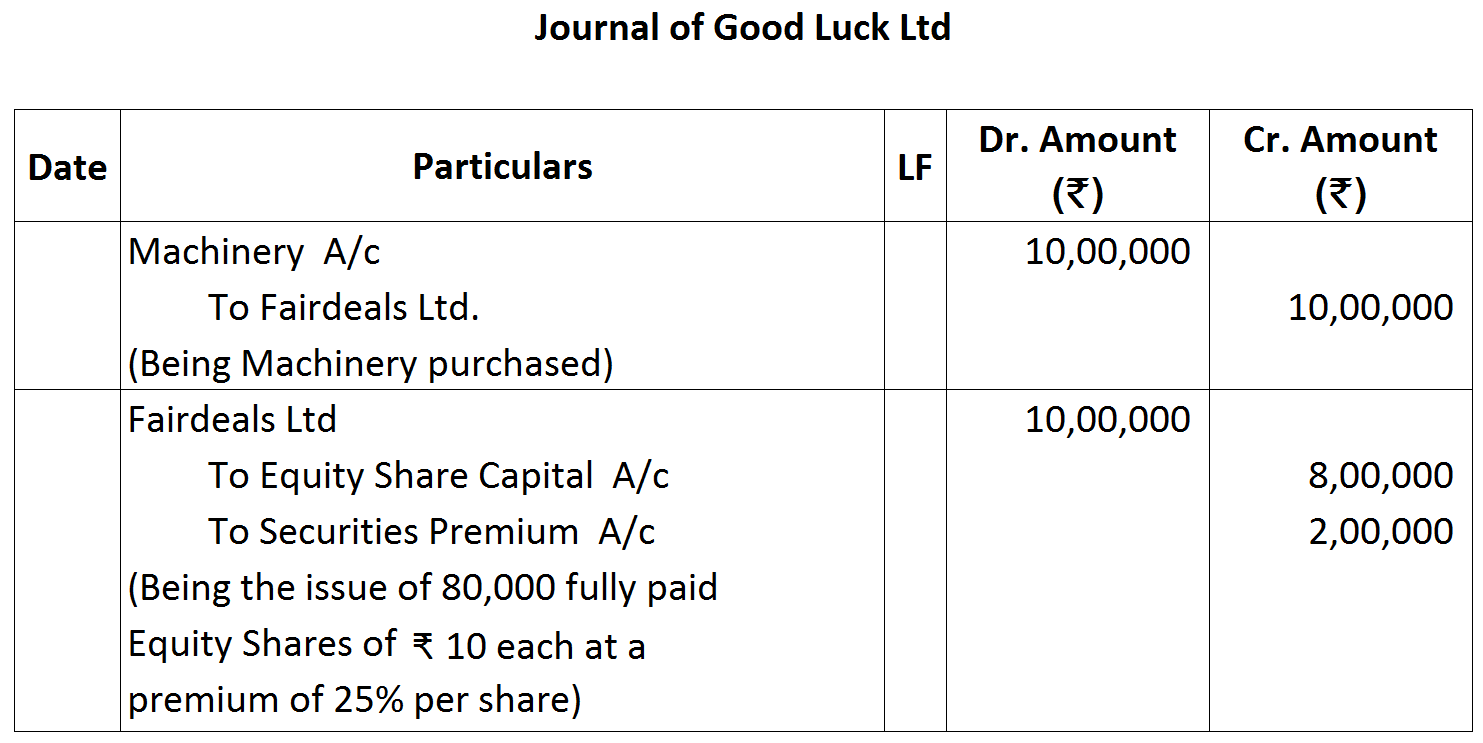

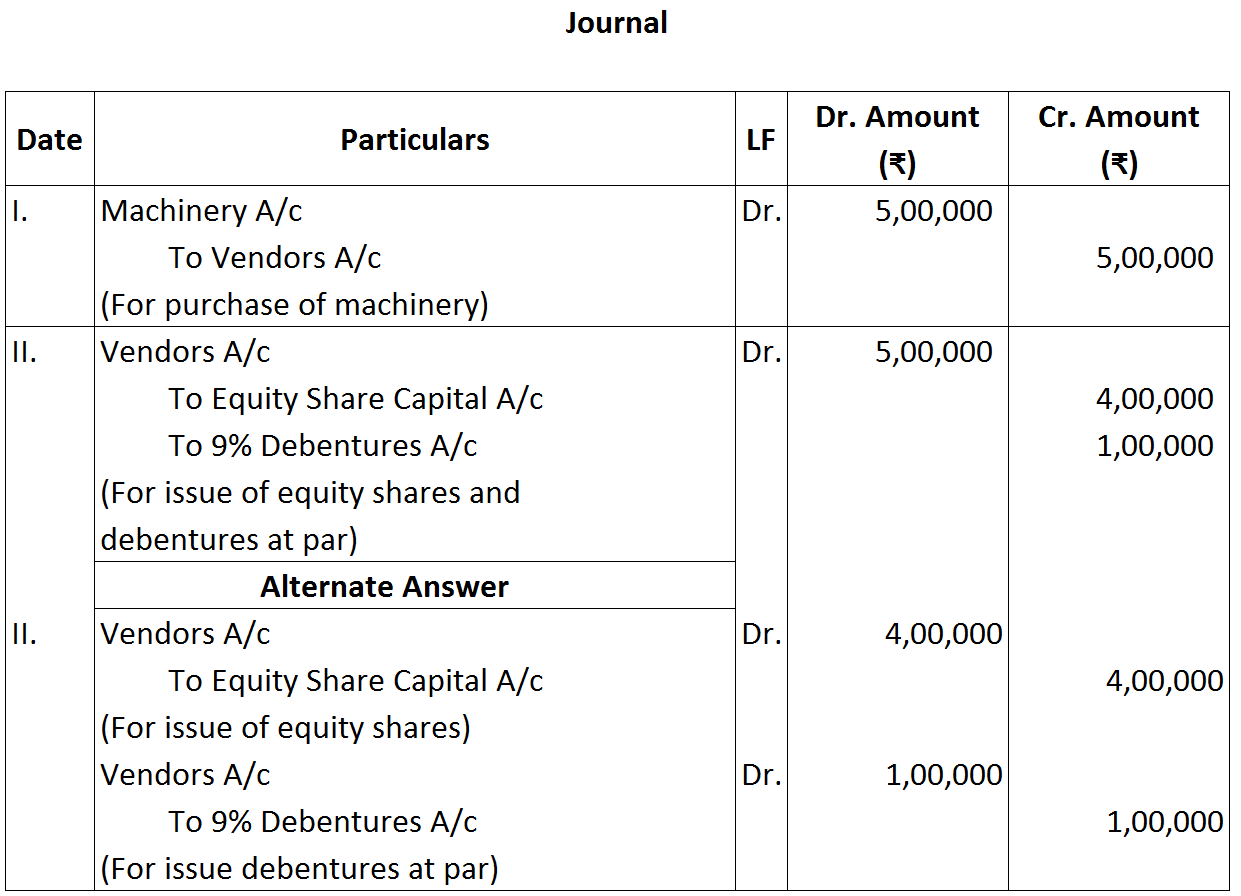

Note: 50,000 equity shares of ₹ 100 each issued to vendors.

Note: 50,000 equity shares of ₹ 100 each issued to vendors. Values:

Values:

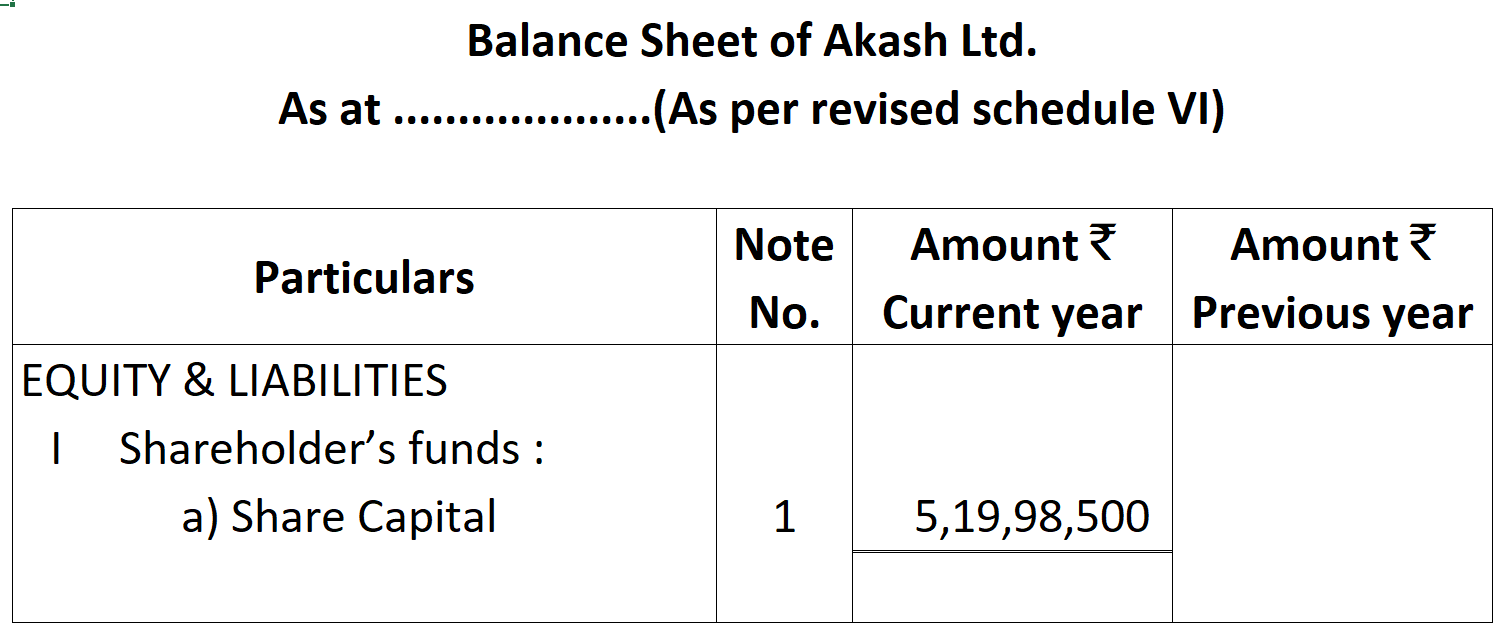

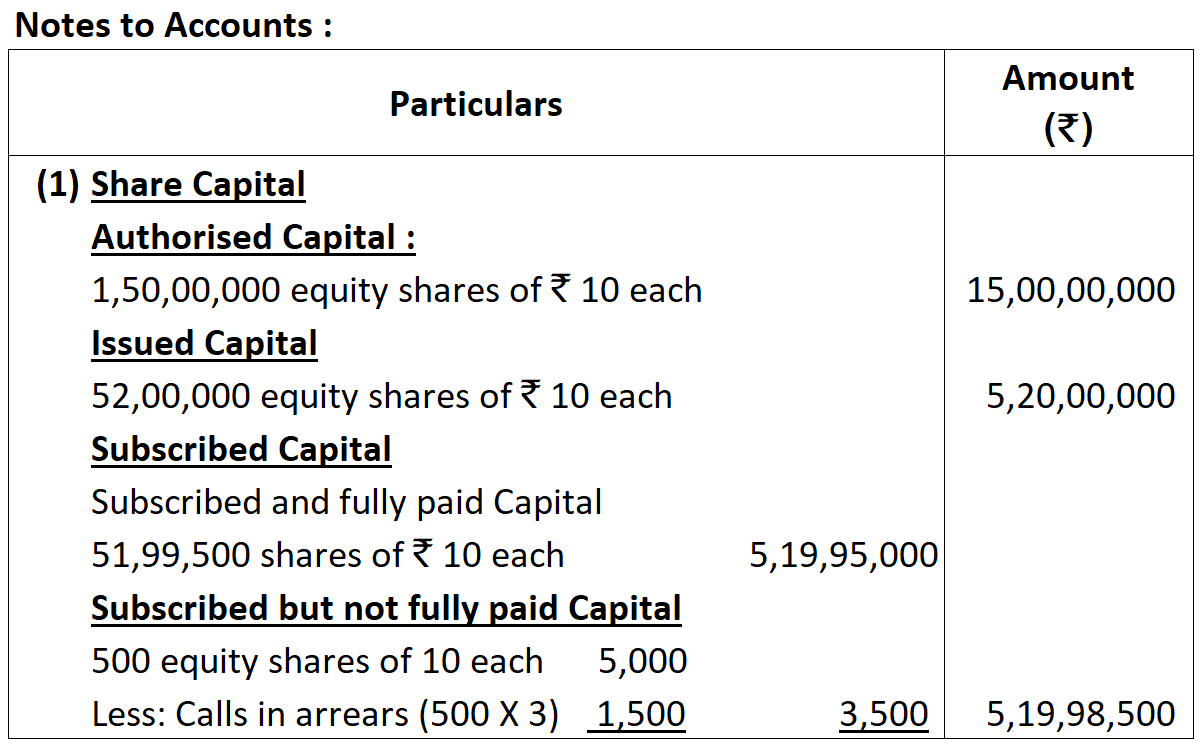

Notes to Accounts:

Notes to Accounts:

Working Note:

Working Note:

Values:

Values:

Values:

Values:

Working Note:

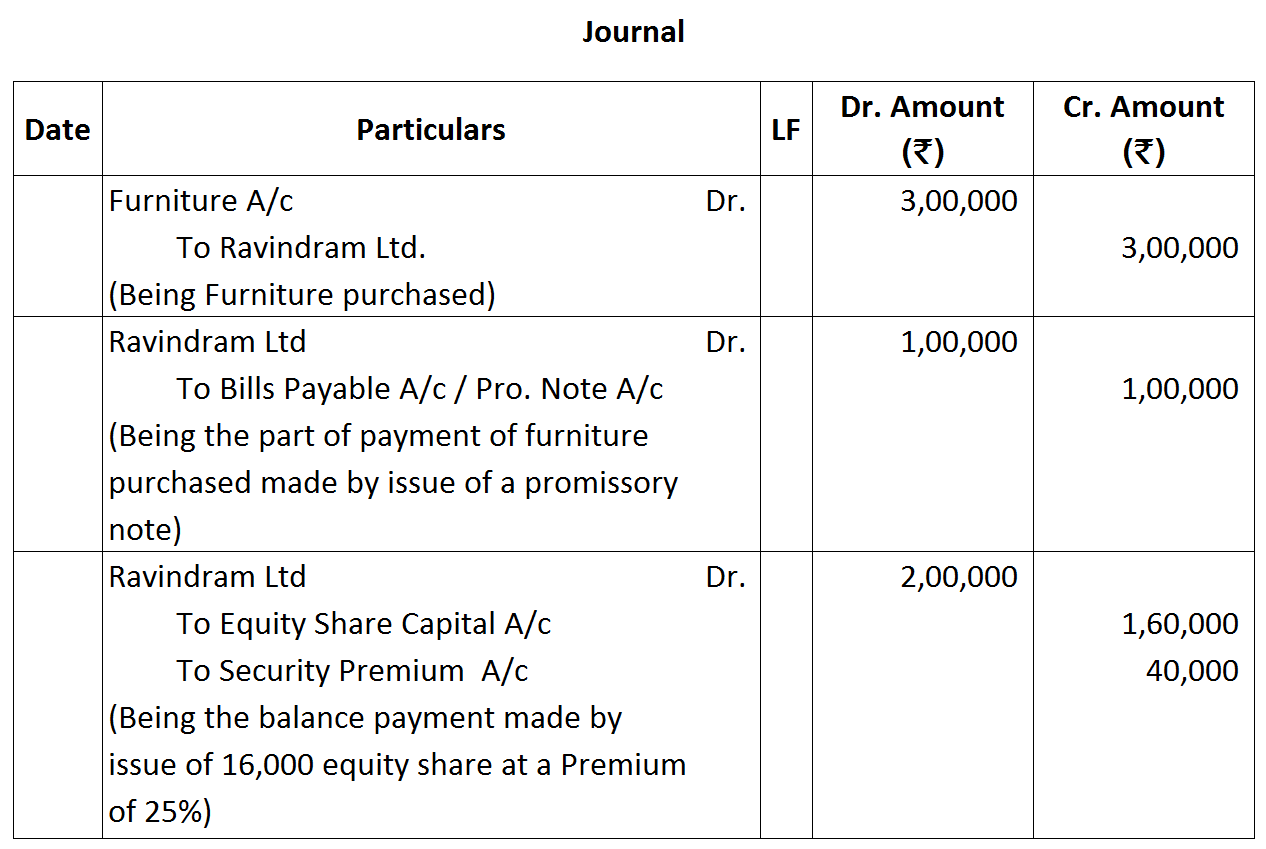

Working Note: Working Note:$\text{Number of Equity Shares to be issued}=\frac {\text{purchase price}} {\text{issue}}$

Working Note:$\text{Number of Equity Shares to be issued}=\frac {\text{purchase price}} {\text{issue}}$ NOTES TO ACCOUNT

NOTES TO ACCOUNT

Working Notes:

Working Notes: Note:

Note: