Question 13 Marks

X Ltd. has a current ratio of 3 : 1 and quick ratio of 2 : 1. If the excess of current assets over quick assets as represented by stock is ₹ 40,000, calculate current assets and current liabilities.

Answer

View full question & answer→Let the Current Liabilities = x

Current Ratio 3:1,so current Assets =3x

Quick Ratio 2:1, SoQuick Assets = 2x

Quick Assets = Current Assets – Stock

2x = 3x – 40,000

-1x = – 40,000

x = ₹ 40,000

Current Liabilities = ₹ 40,000

Current Assets = 3 x 40,000 = ₹ 1,20,000

Current Ratio 3:1,so current Assets =3x

Quick Ratio 2:1, SoQuick Assets = 2x

Quick Assets = Current Assets – Stock

2x = 3x – 40,000

-1x = – 40,000

x = ₹ 40,000

Current Liabilities = ₹ 40,000

Current Assets = 3 x 40,000 = ₹ 1,20,000

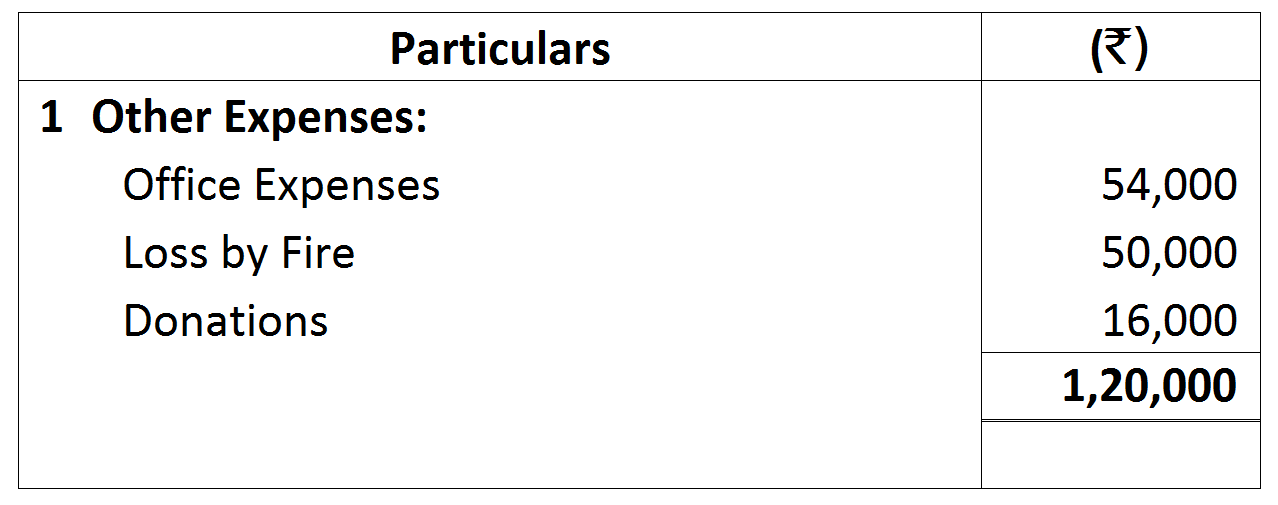

Notes to Accounts:

Notes to Accounts: