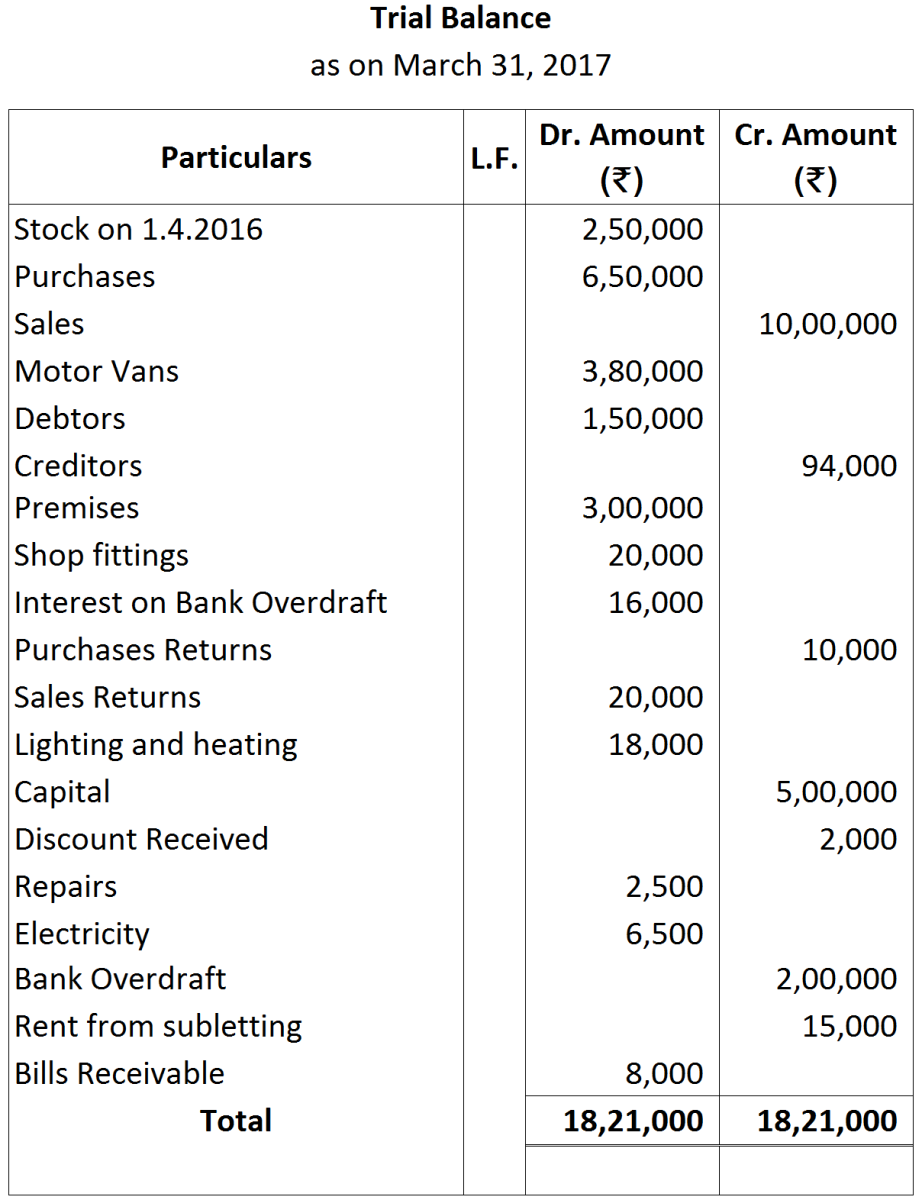

Question 16 Marks

What kinds of errors would cause difference in the trial balance. Also list examples that would not be revealed by a trial balance?

Answer

View full question & answer→The errors that lead to the differences in the Trial Balance are termed as one-sided errors. These are those errors that affect only one account. Below are given the errors that cause differences in the Trial Balance.

- Wrong casting of any account, this is termed as the error of casting.

- Wrong carrying forward of the balances from previous year’s books or from one end of page to another. These types of errors are termed as the errors in carrying forward.

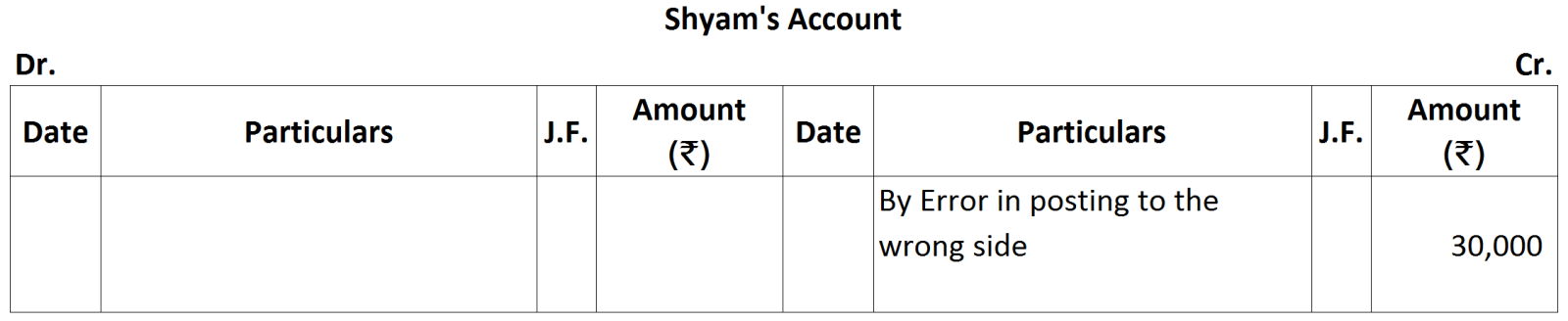

- If entries are posted in the wrong side of accounts.

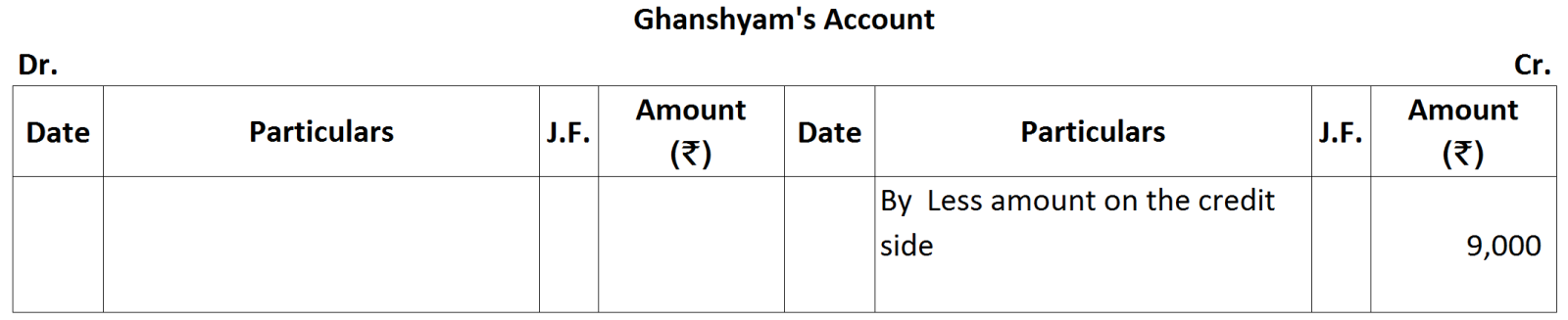

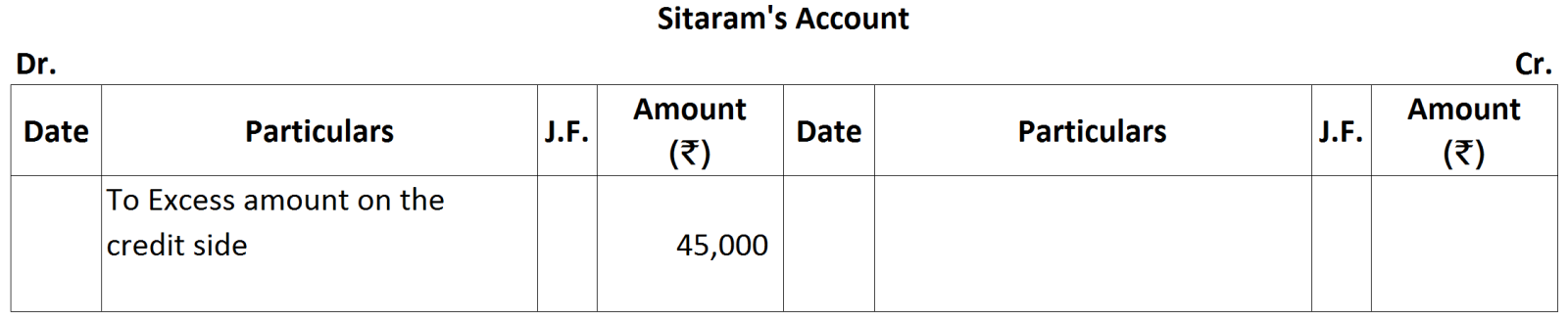

- Posting of a wrong amount in account, this is termed as the error of posting.

- If entries are recorded partially, i.e., the entries are not recorded completely, then due to the error of partial omission, Trial Balance does not agree.

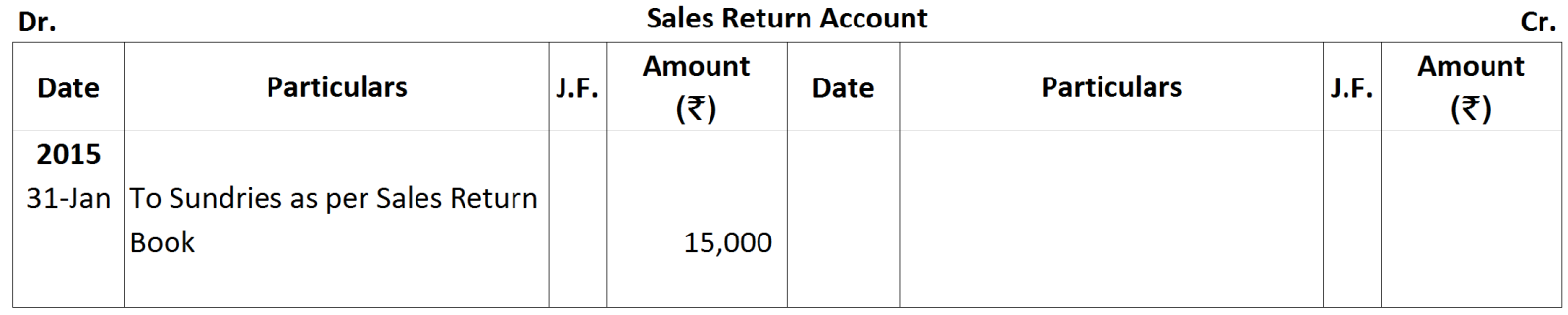

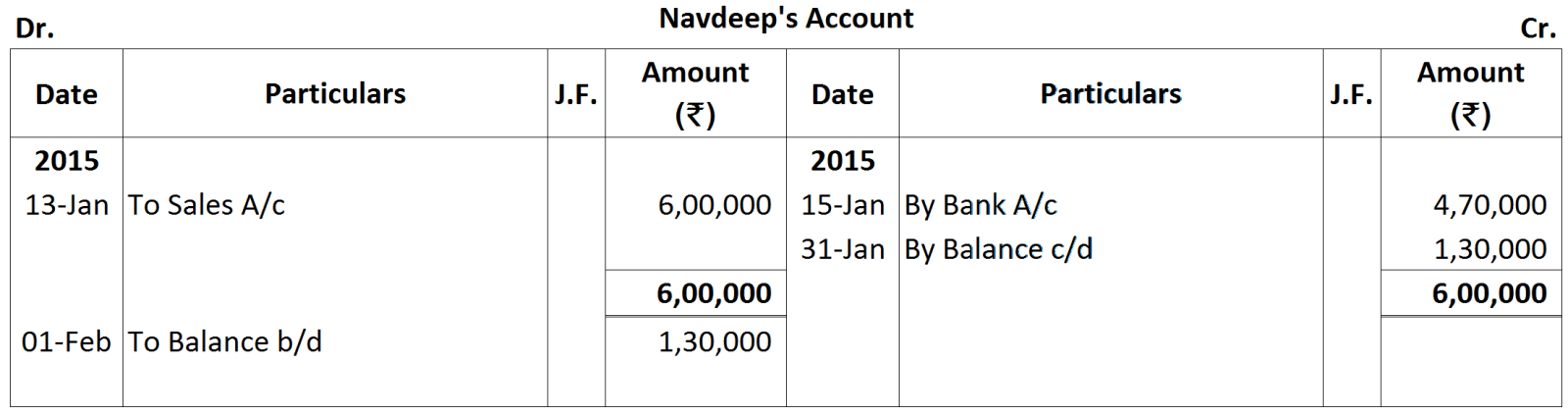

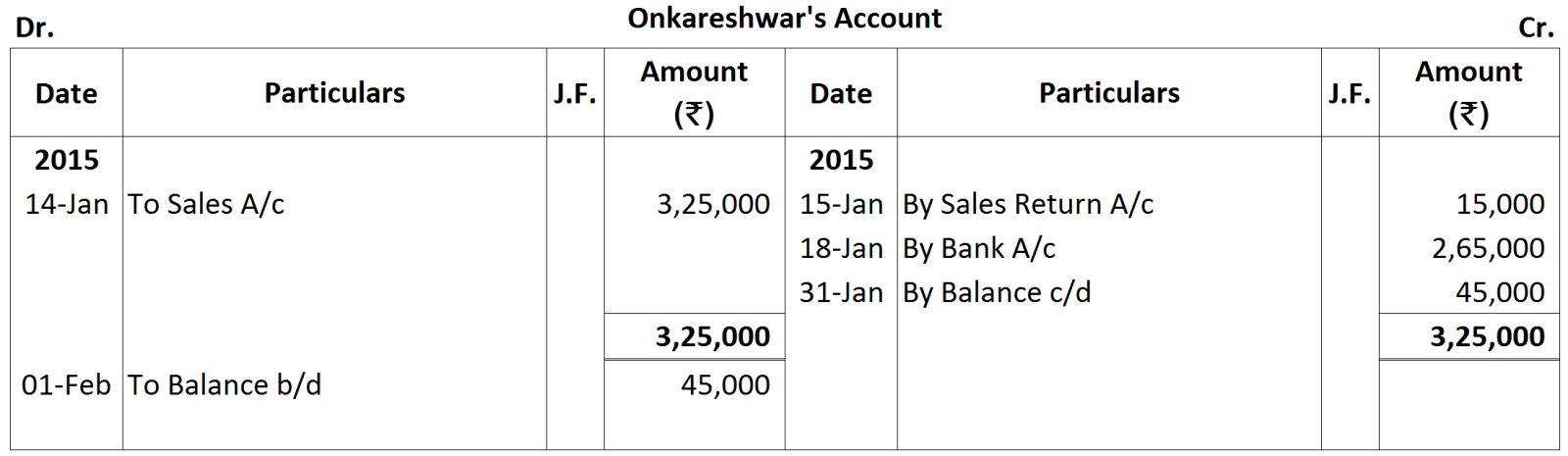

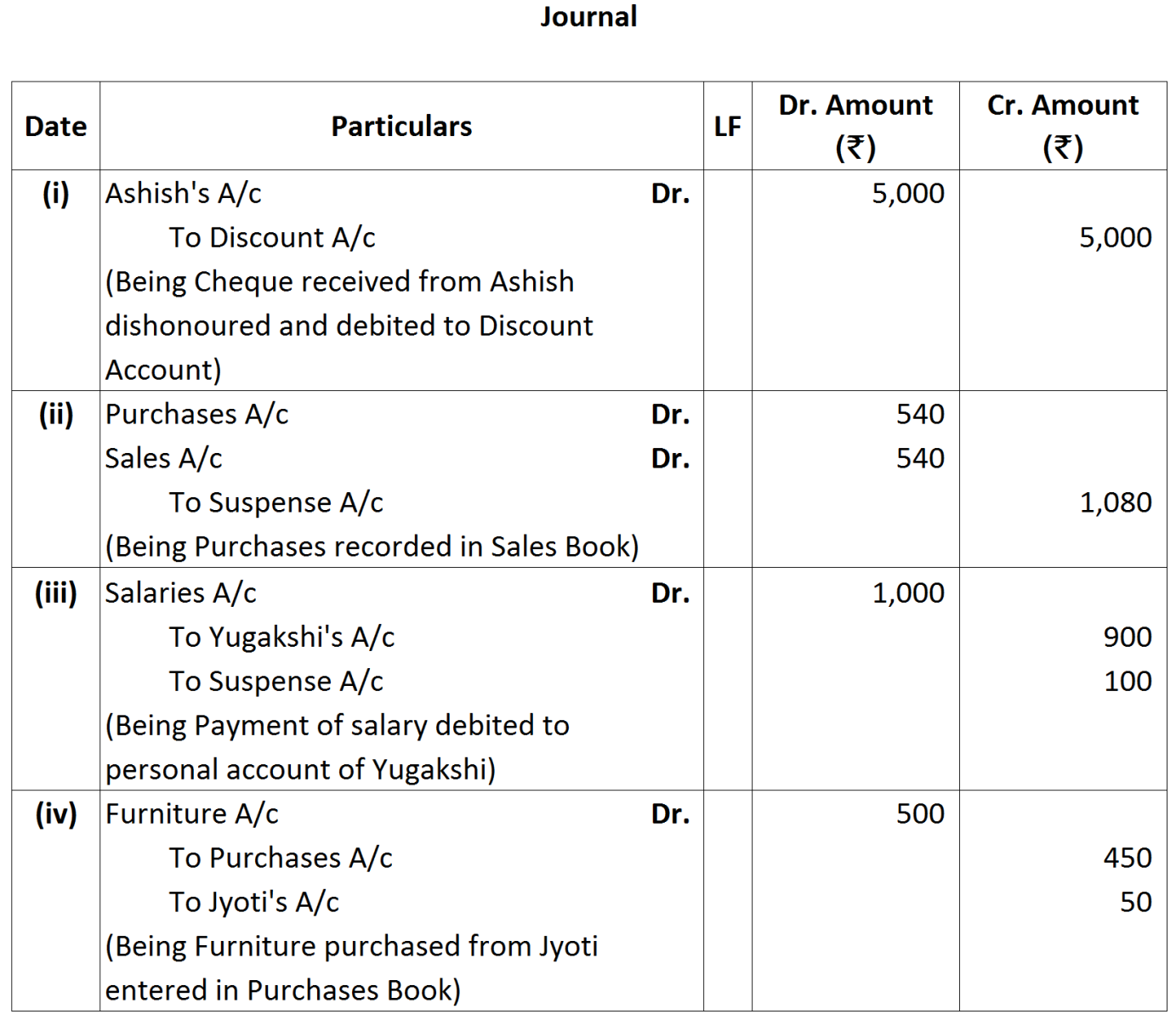

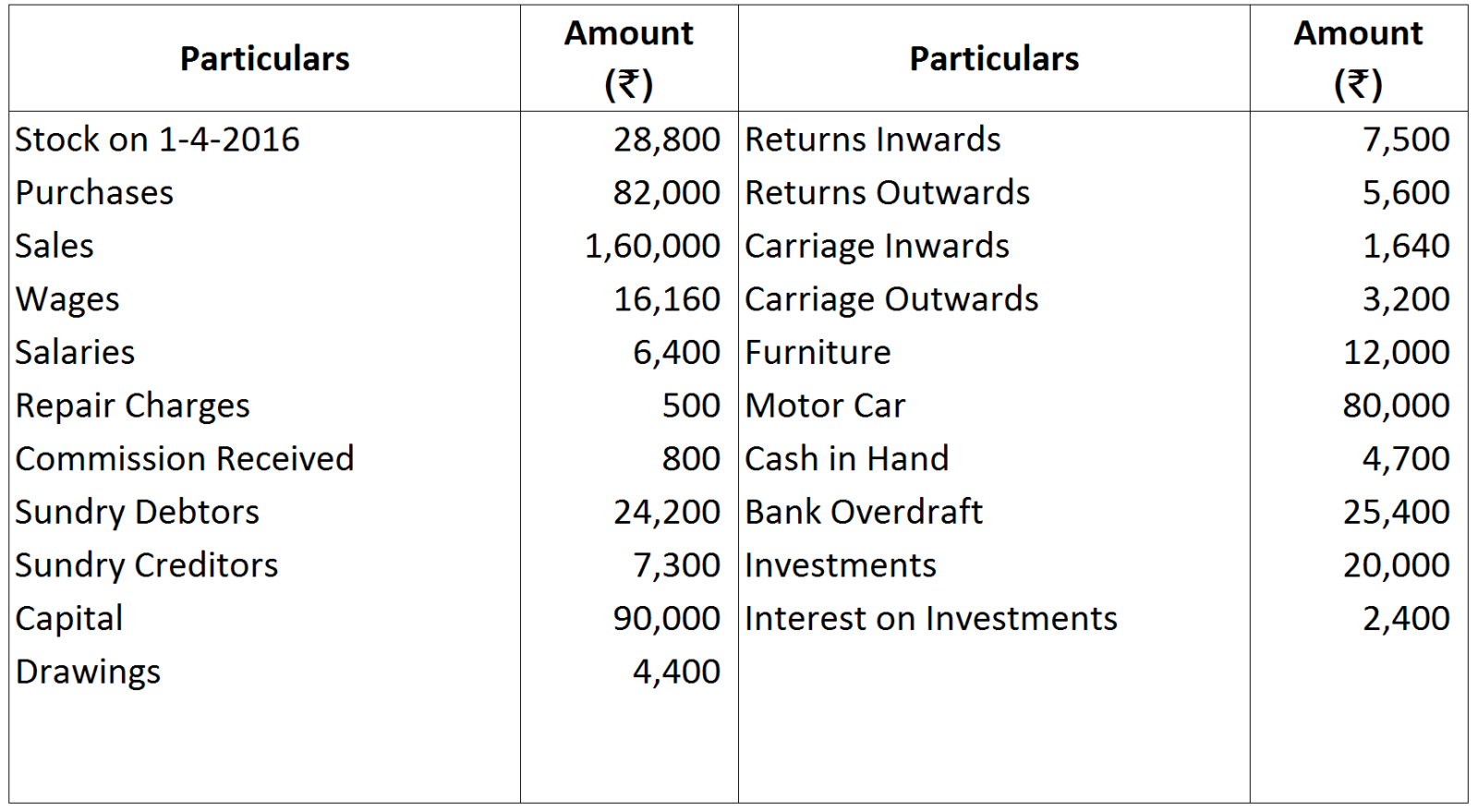

- Sales to Mr. X, omitted to be recorded in the Sales Day Book.

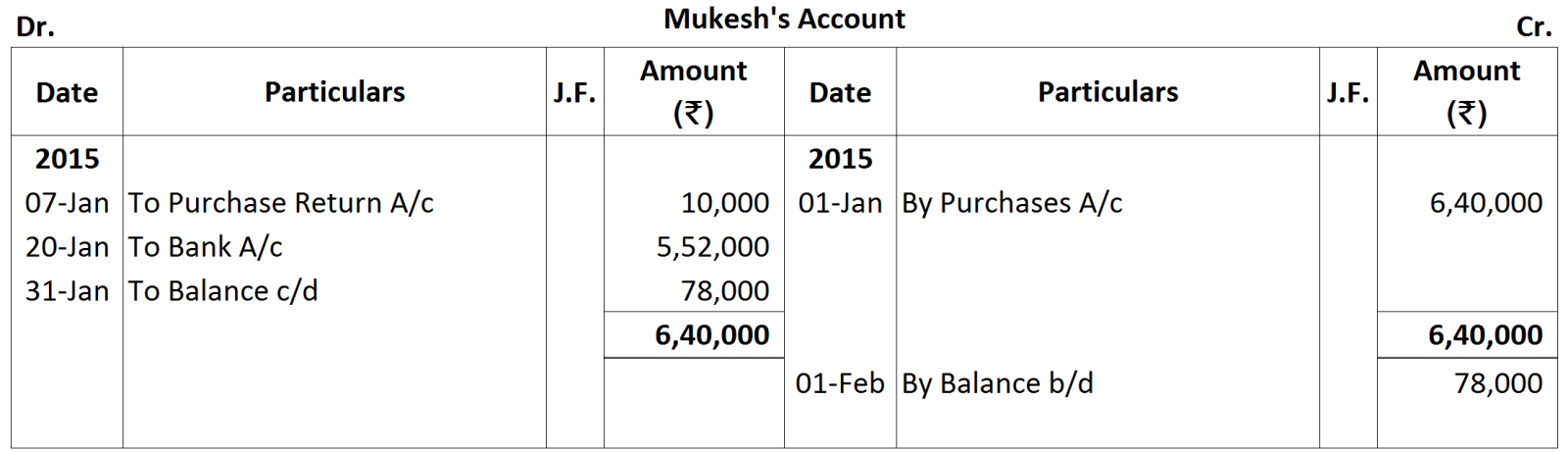

- Purchases made from Mukesh, recorded in Mahesh’s Account, who is an other creditor.

- Wages paid for construction of building, recorded in the Wages Account.

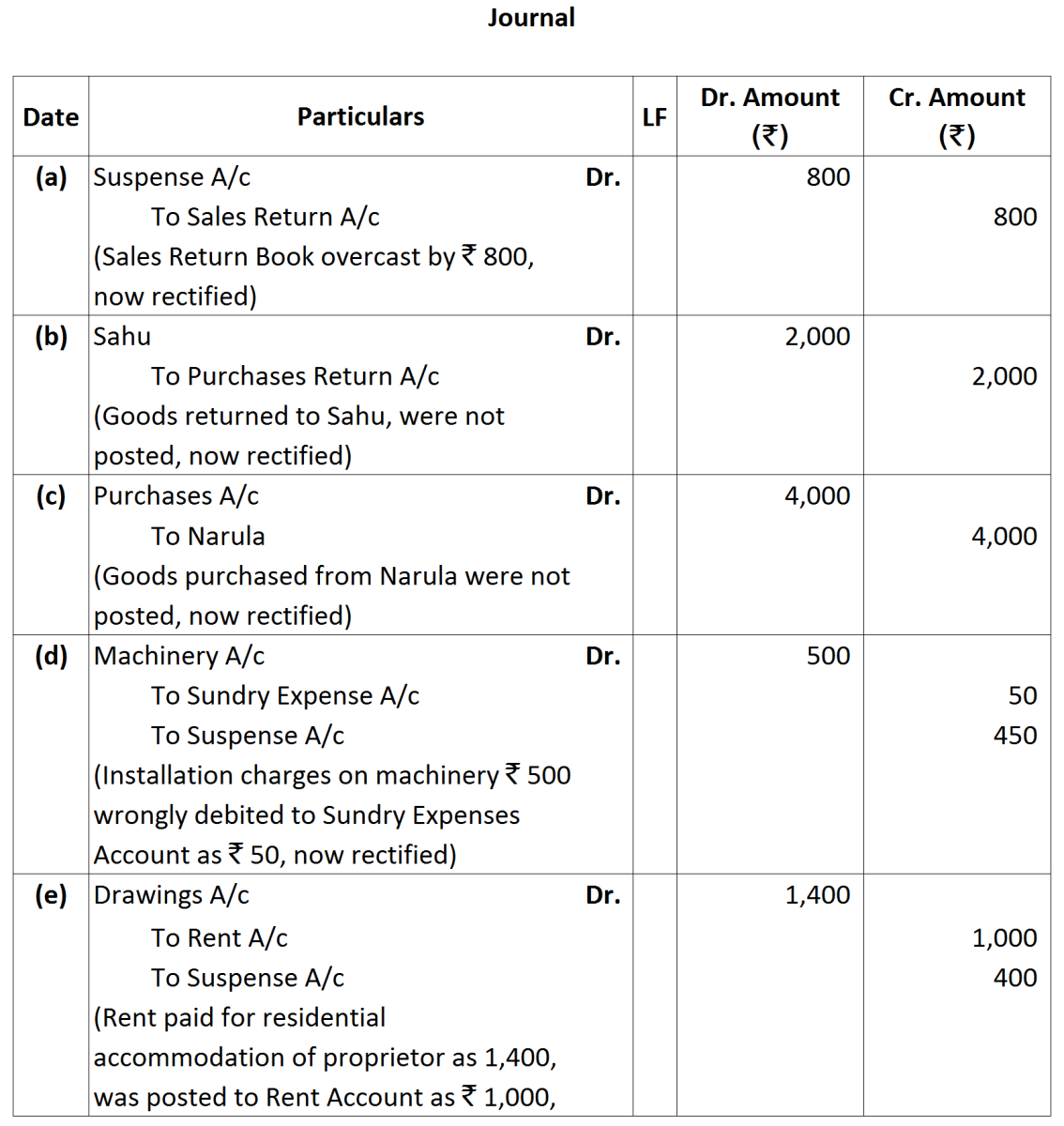

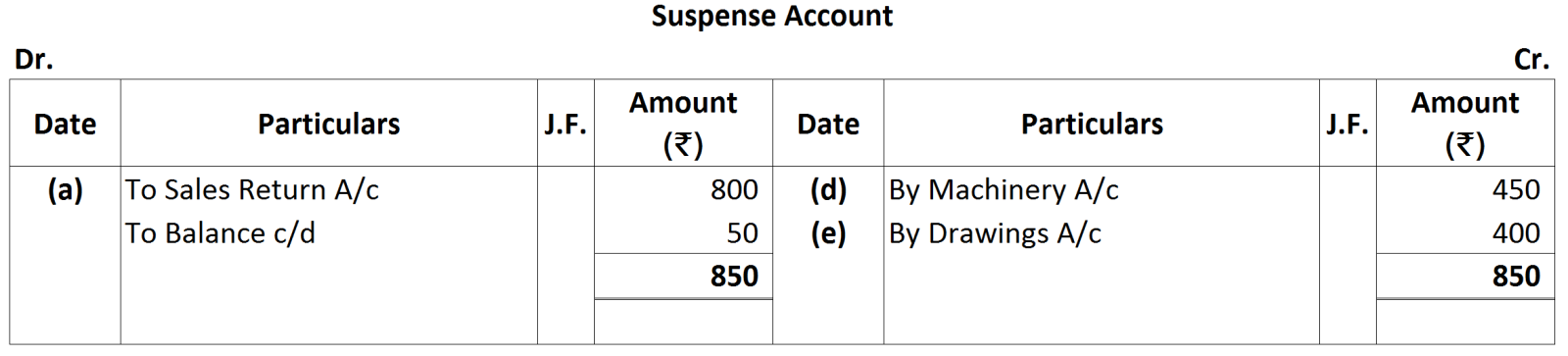

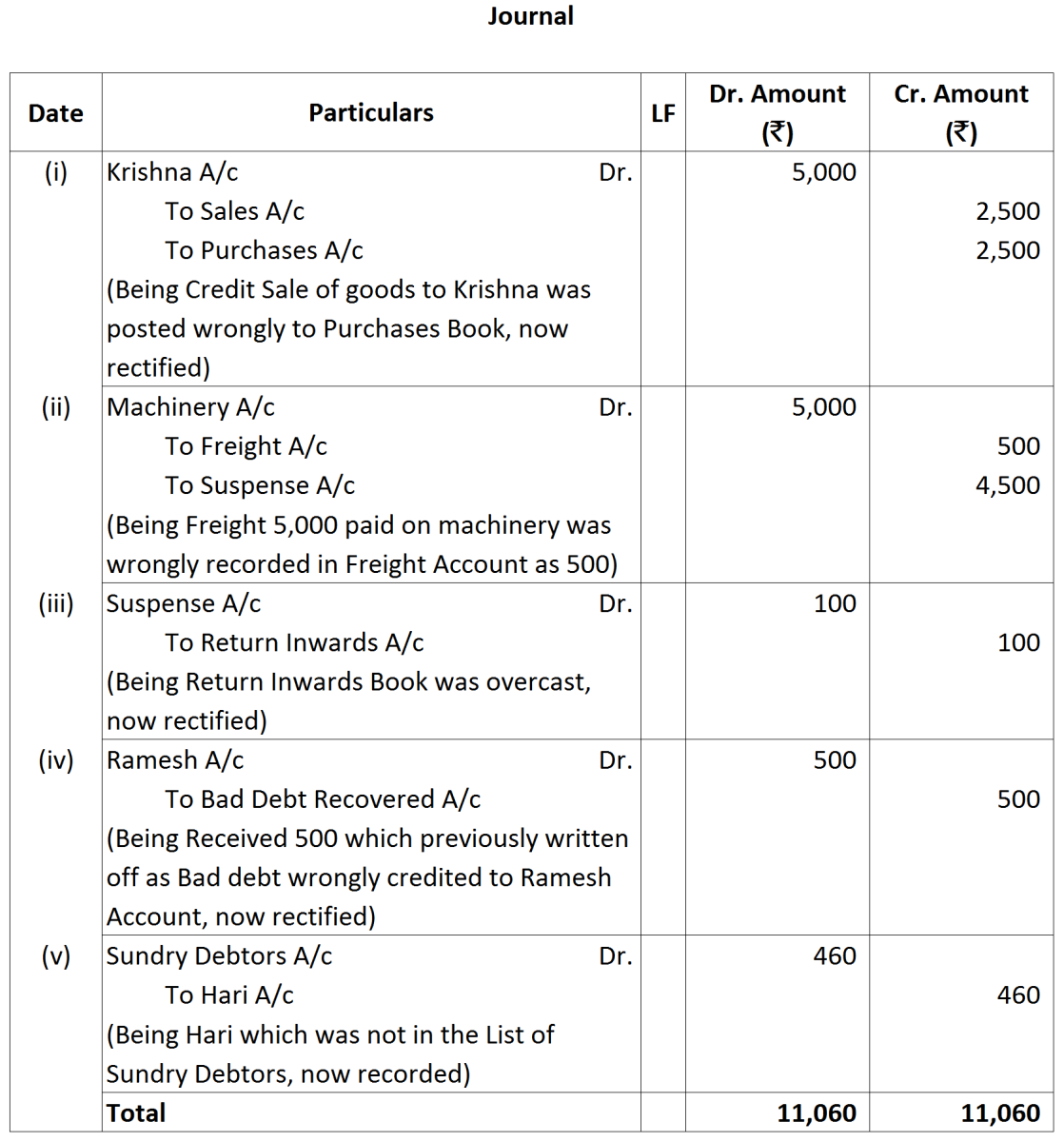

Note: As per the solution Suspense Account shows a credit balance of ₹ 50. However, as per the answer given in the book, it is a credit balance of ₹ 2050. In order to match answer with the book item (b) is taken as, ‘Purchases return to Sahu ₹ 2,000 were not posted to Sahu’s Account.’ Thus, the rectifying entry for this error will be as:

Note: As per the solution Suspense Account shows a credit balance of ₹ 50. However, as per the answer given in the book, it is a credit balance of ₹ 2050. In order to match answer with the book item (b) is taken as, ‘Purchases return to Sahu ₹ 2,000 were not posted to Sahu’s Account.’ Thus, the rectifying entry for this error will be as:

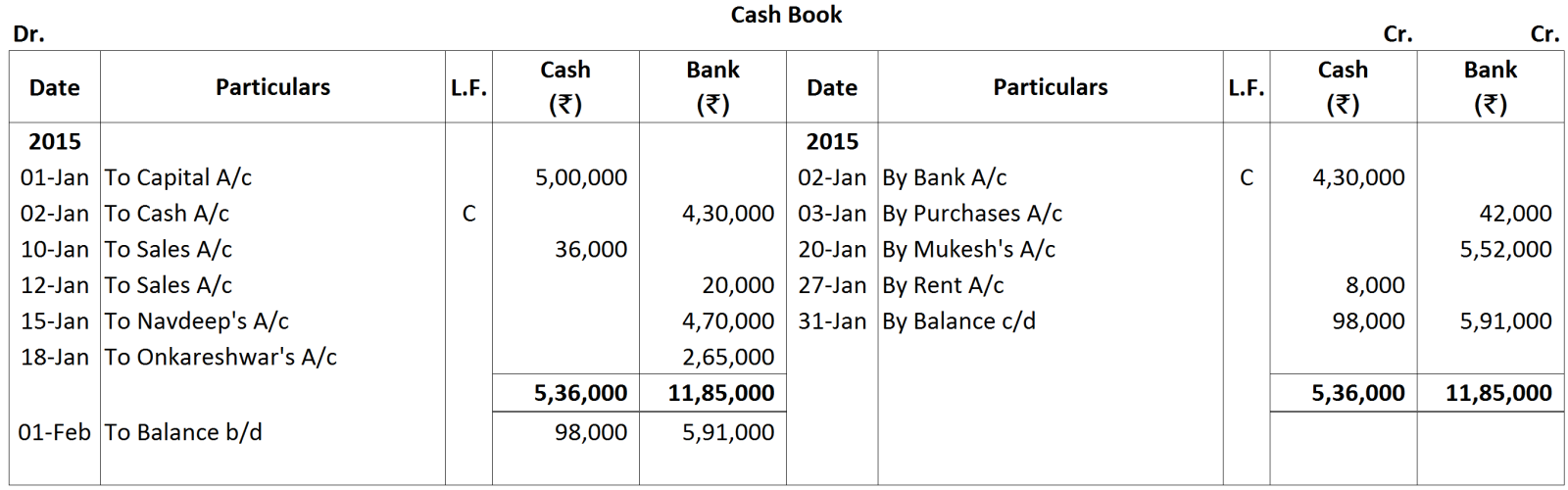

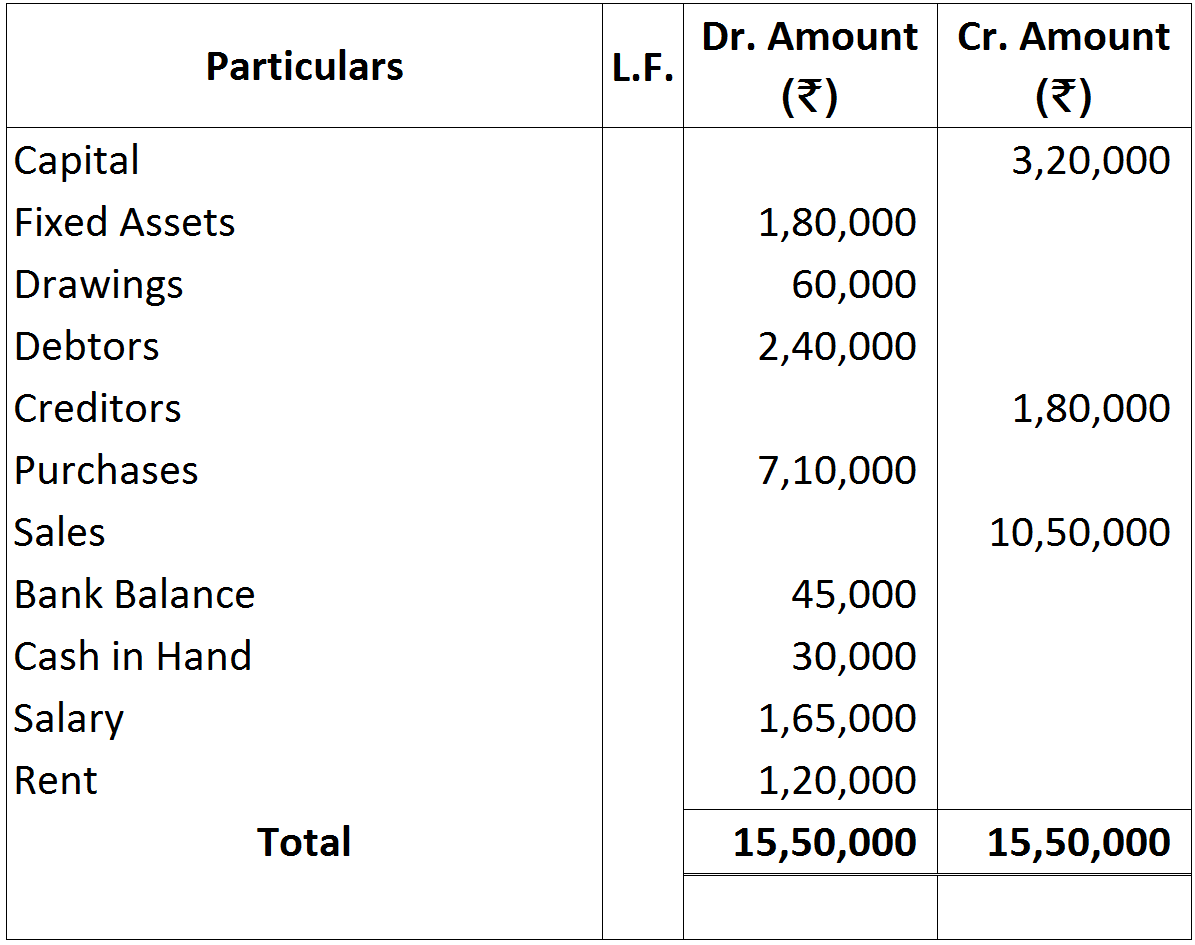

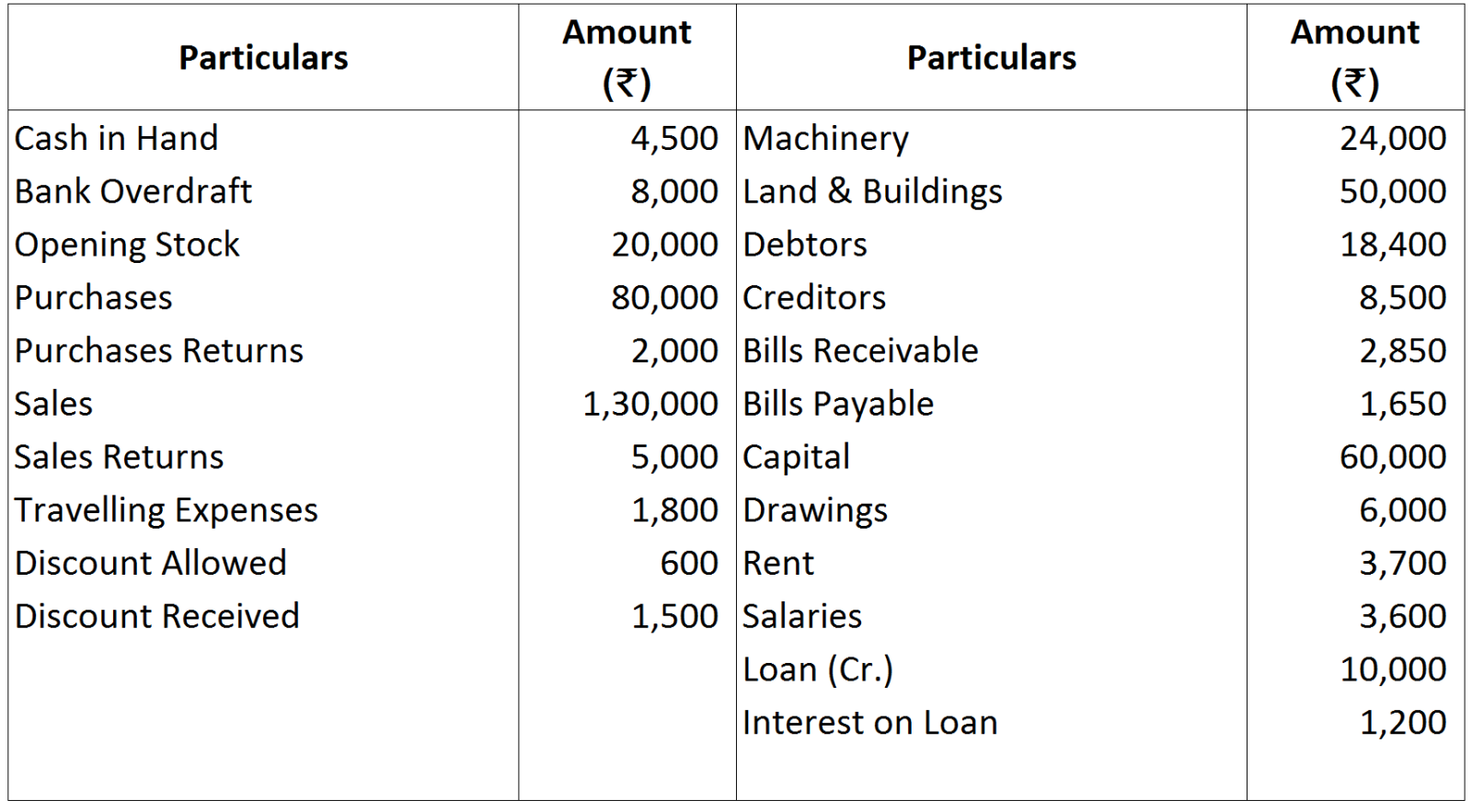

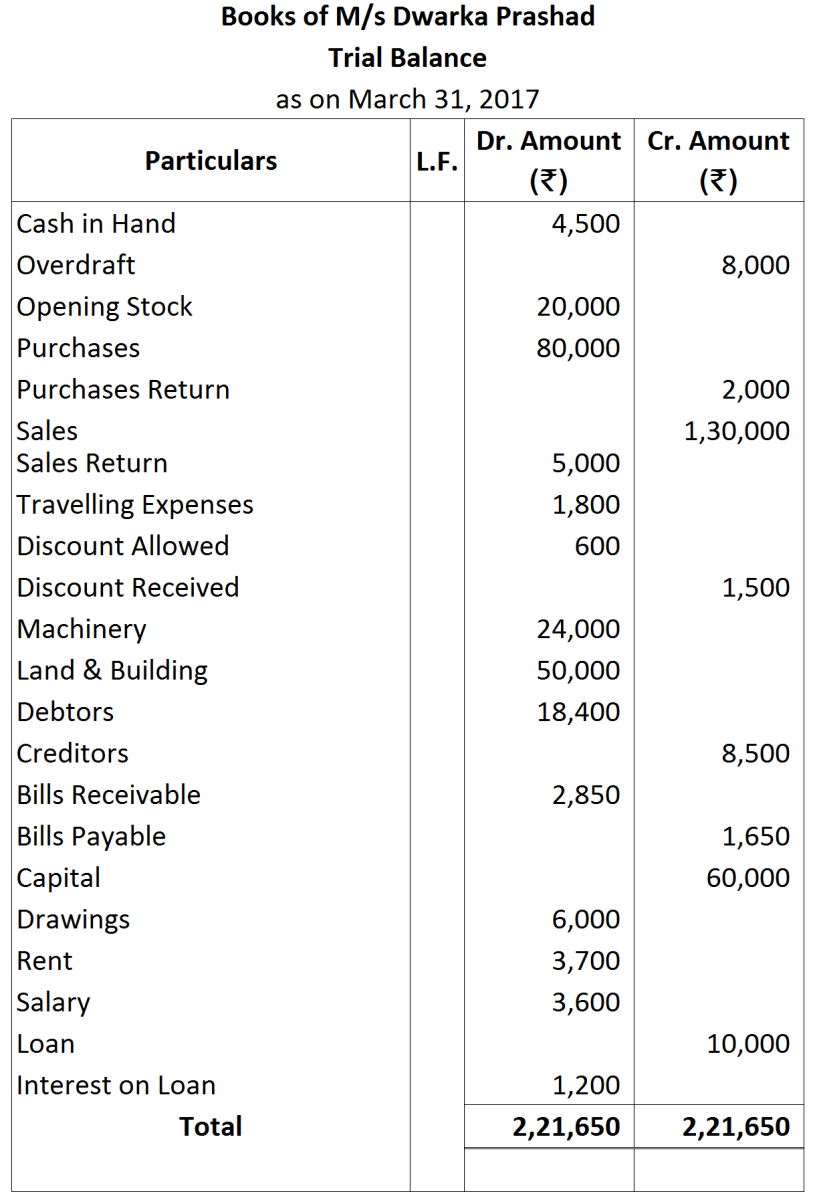

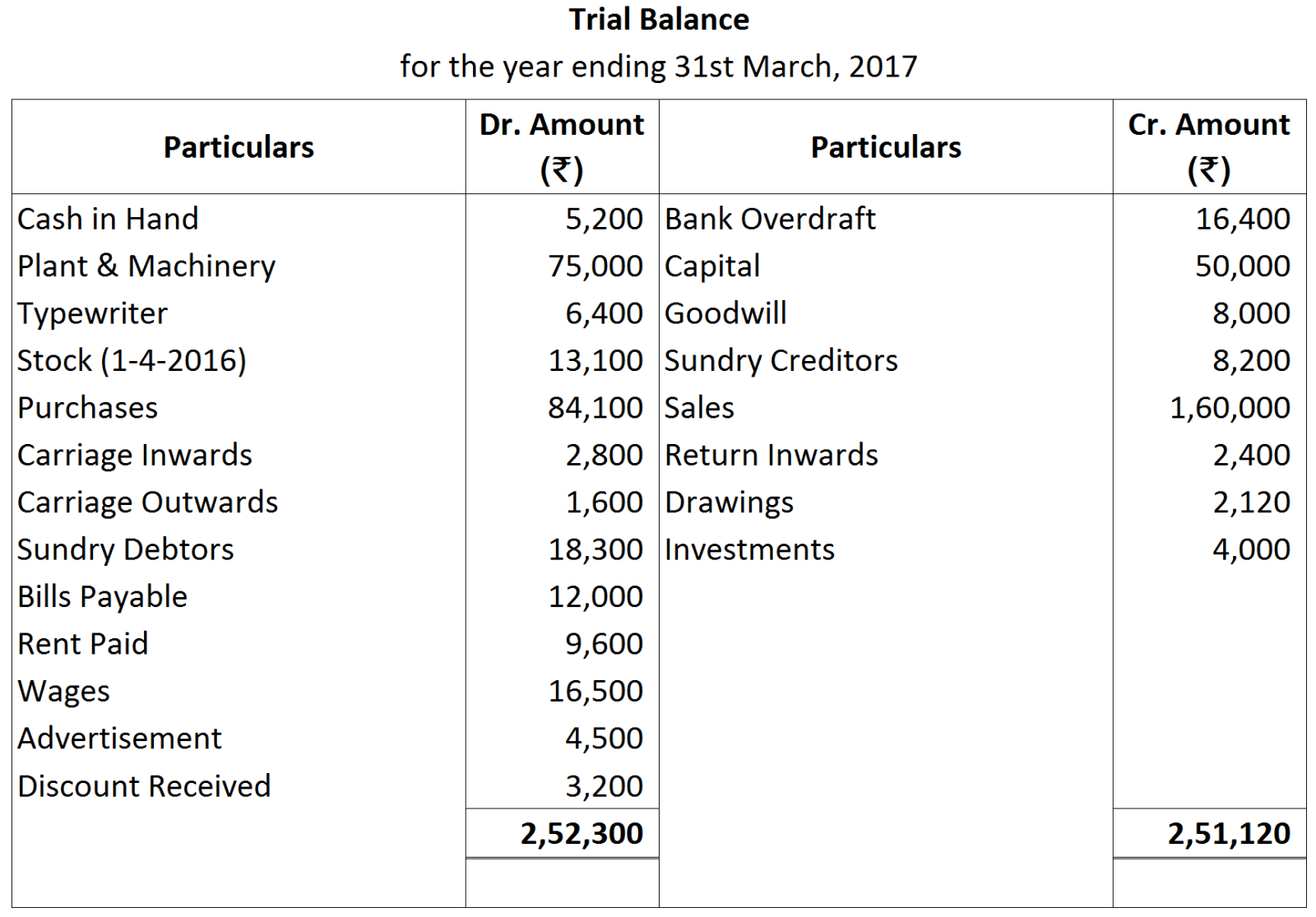

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded:

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded:

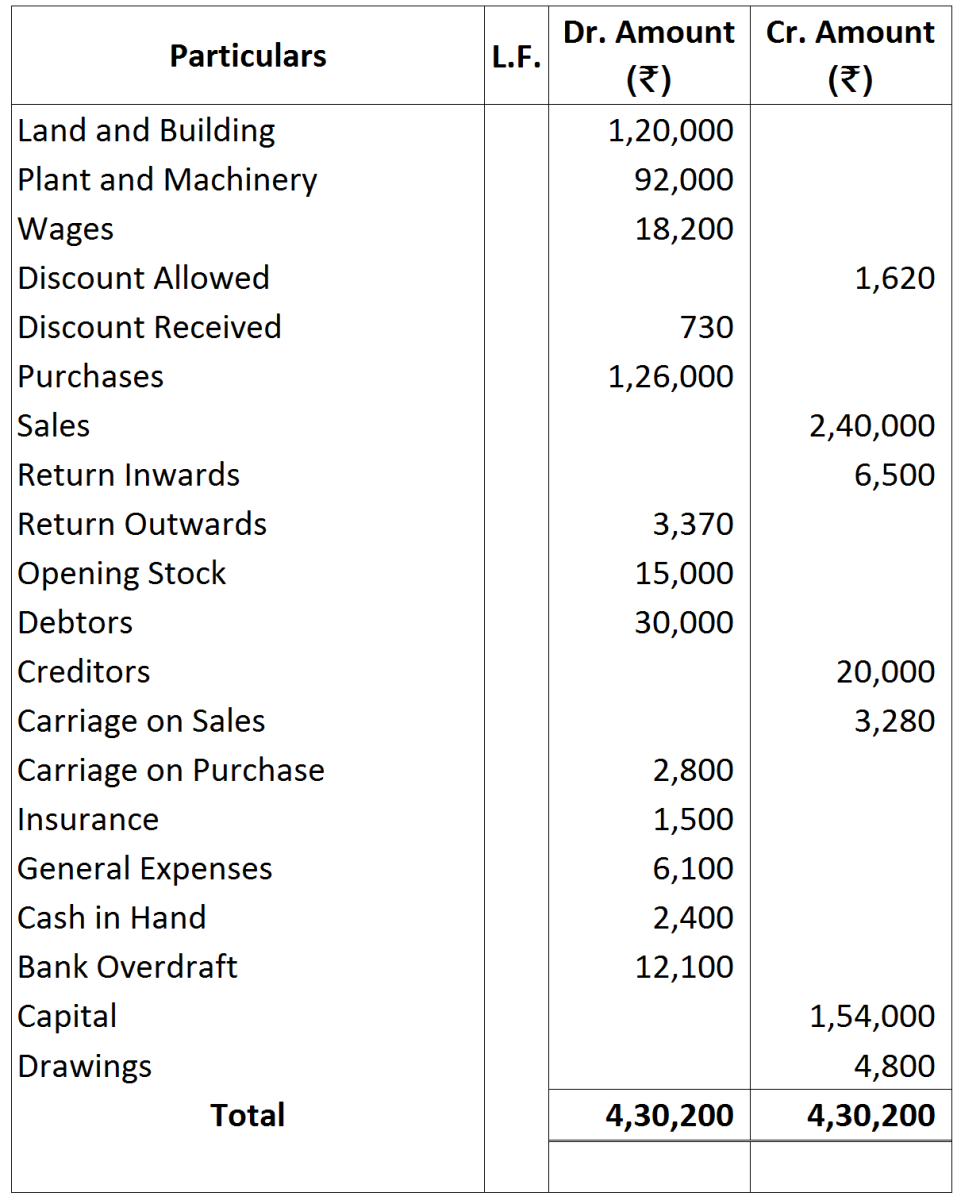

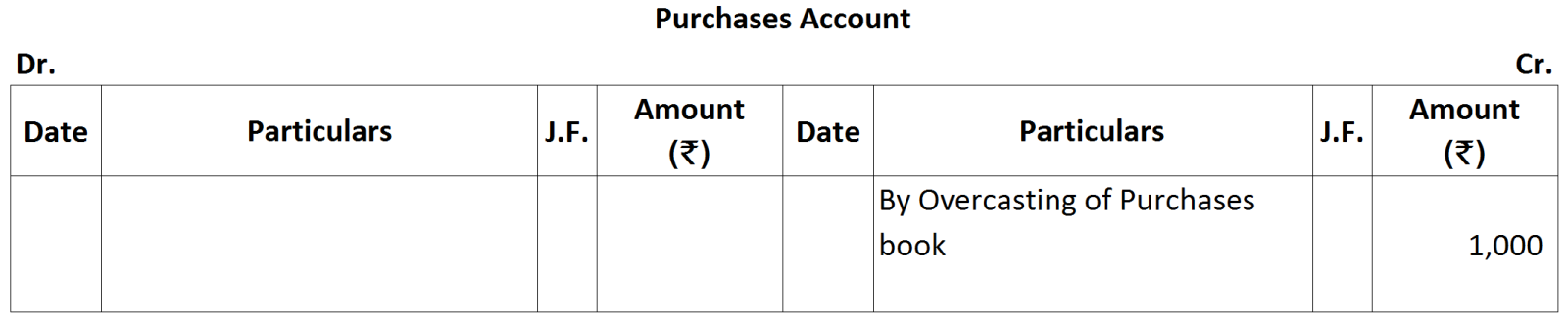

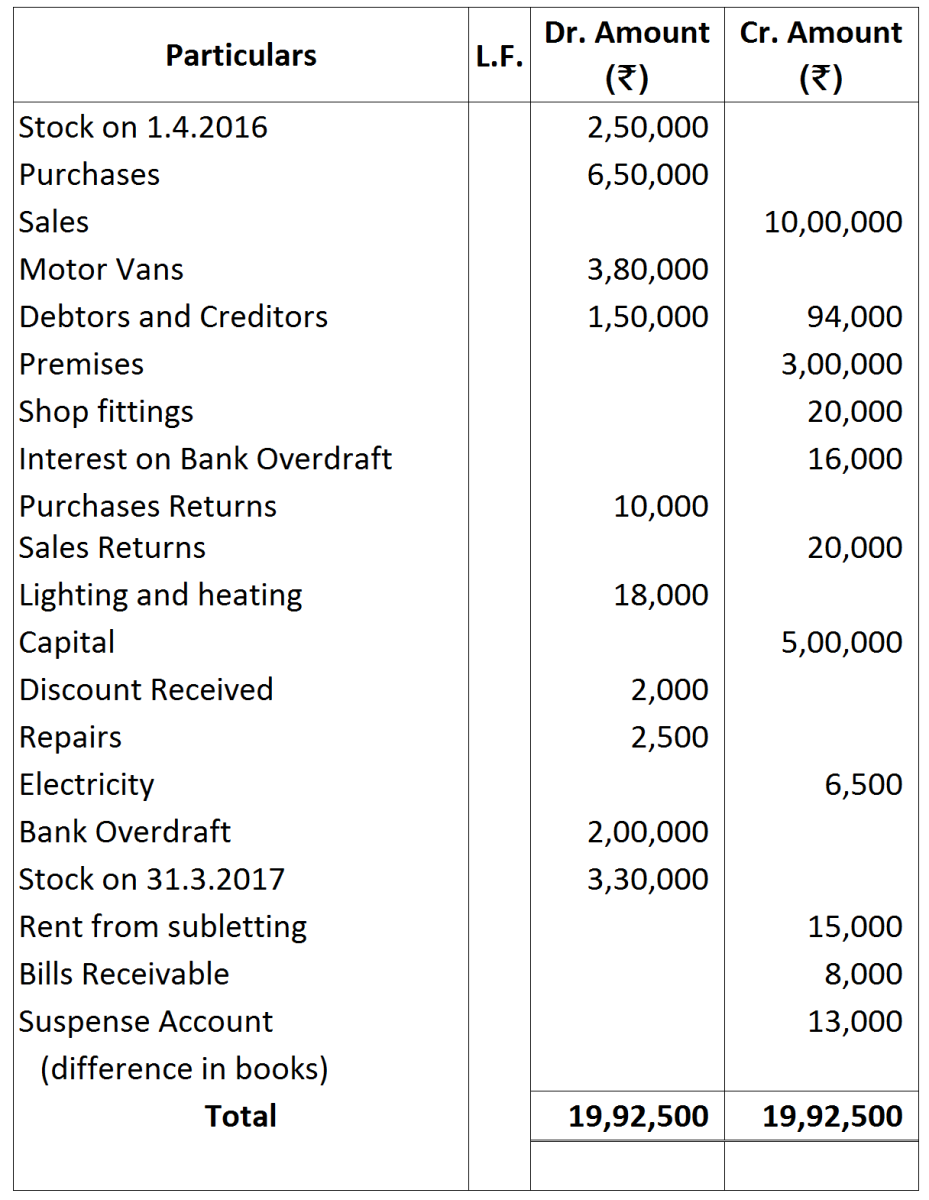

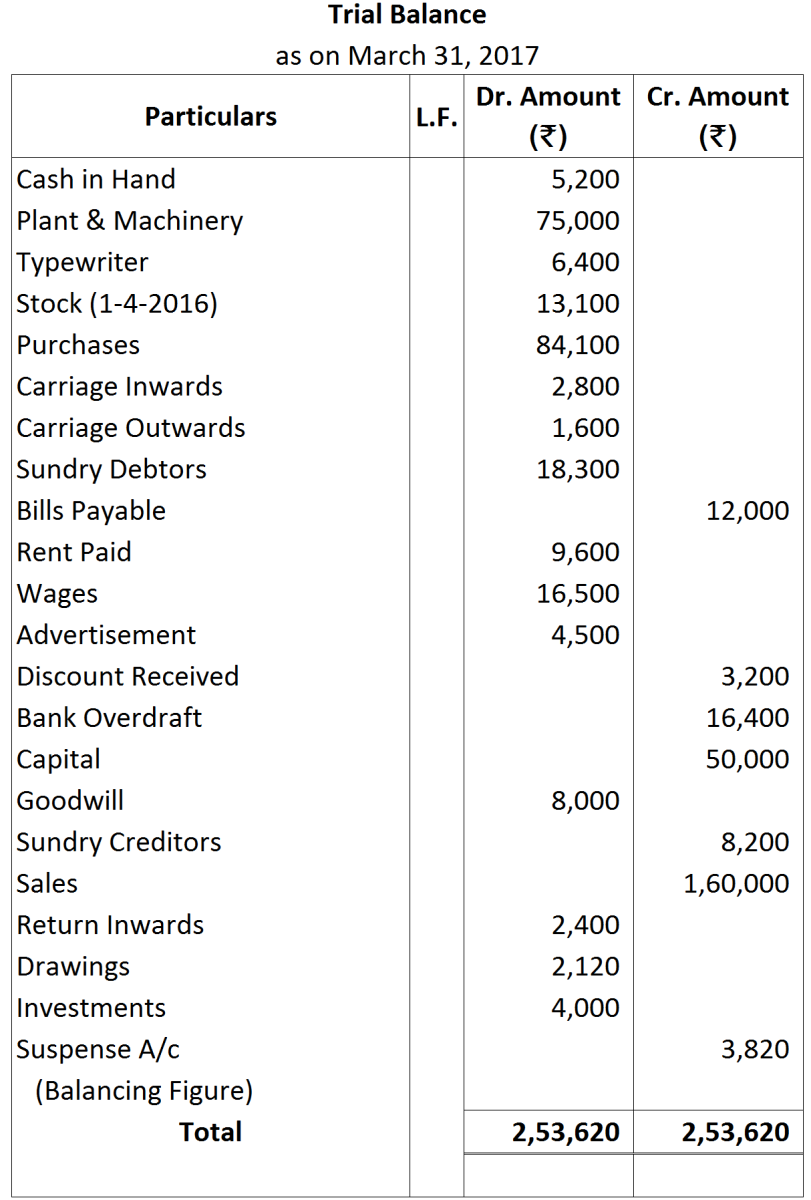

Note: Since, the Trial Balance does not tally, thus, the difference of ₹ 3,820 is transferred to the Credit Balance Column of Trial Balance.

Note: Since, the Trial Balance does not tally, thus, the difference of ₹ 3,820 is transferred to the Credit Balance Column of Trial Balance.