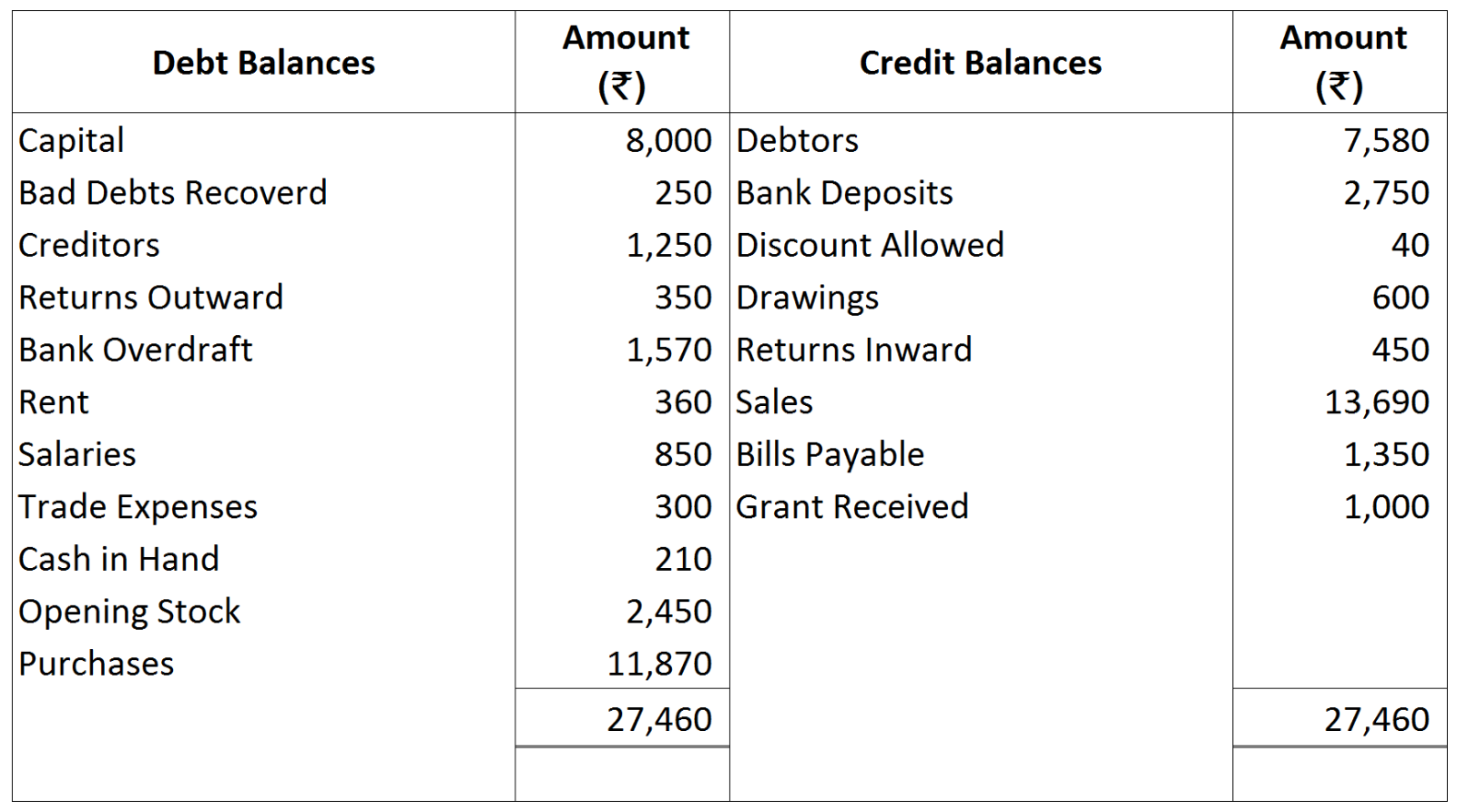

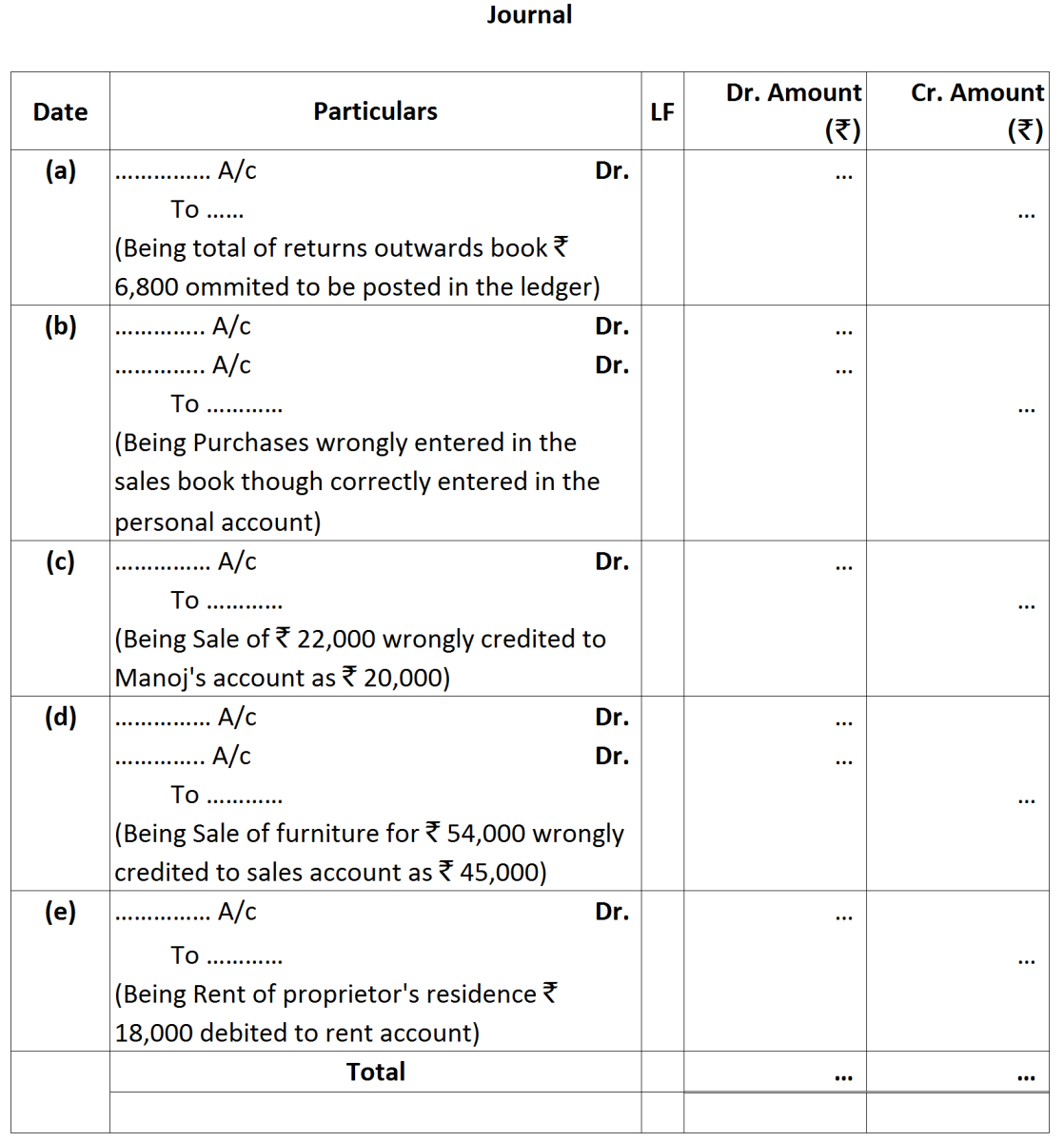

Question 516 Marks

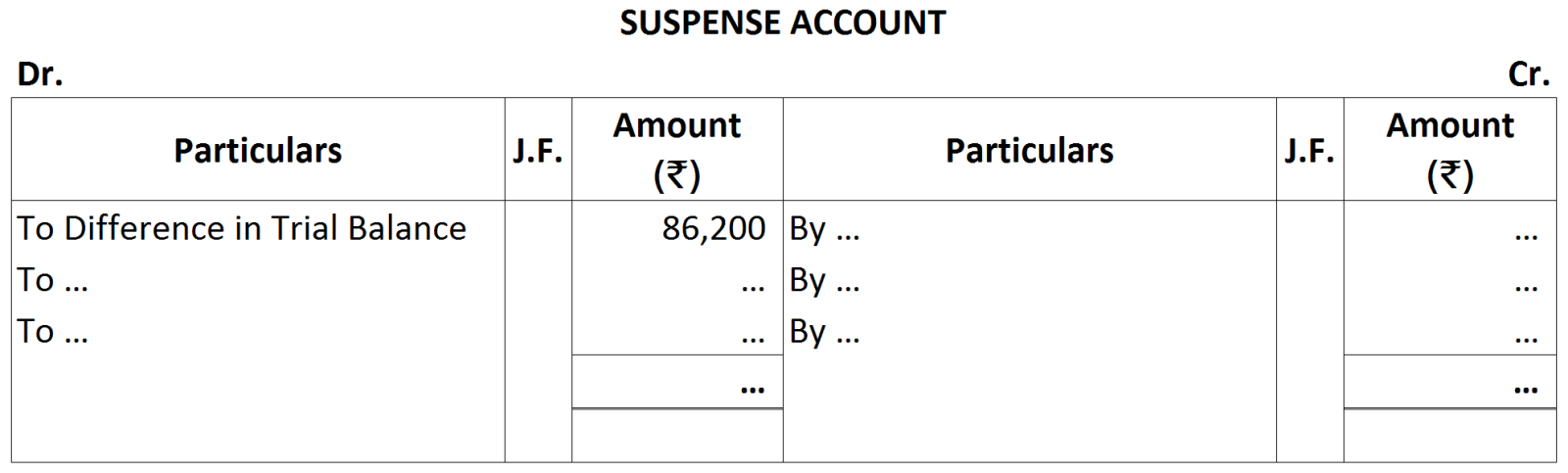

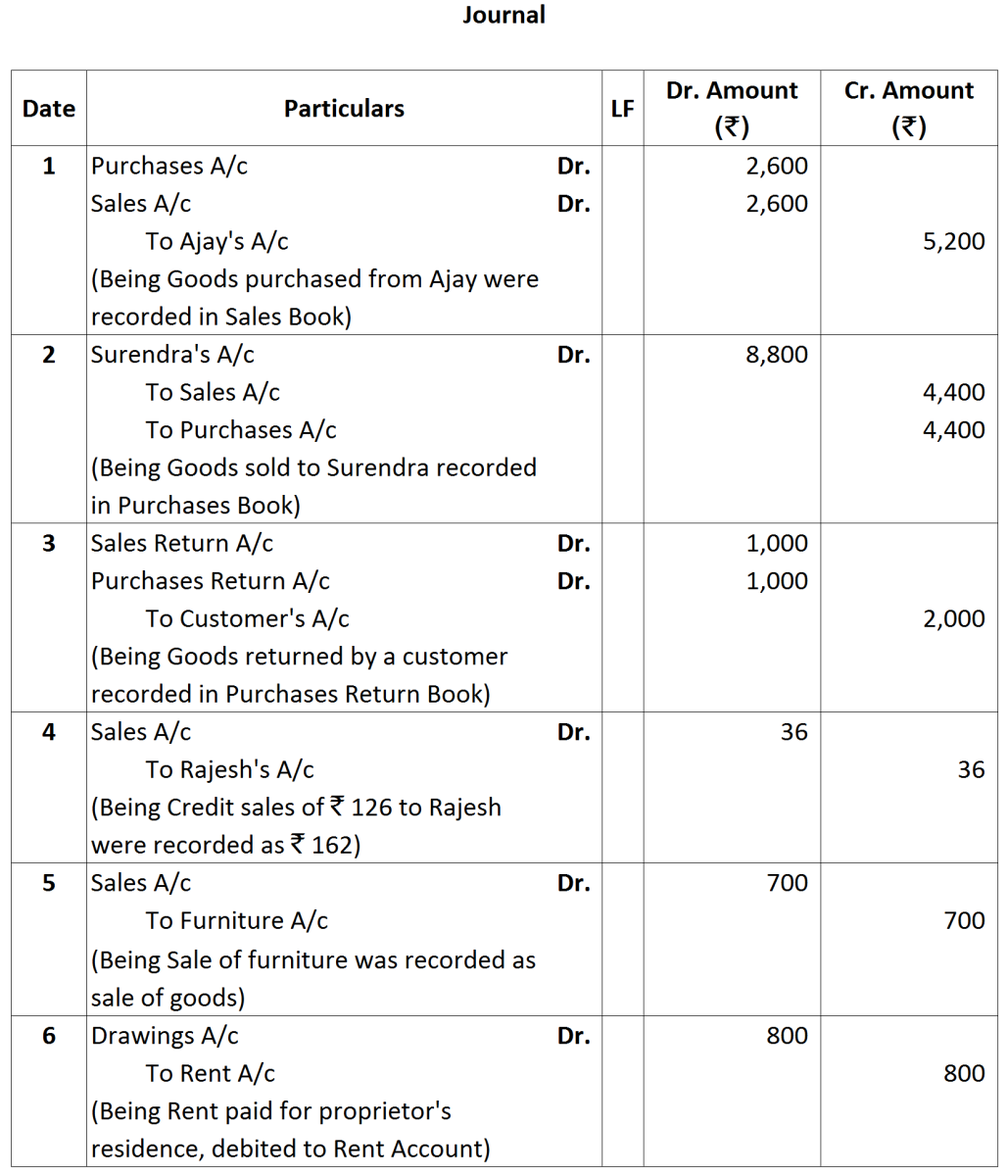

A Book-keeper finds that the totals of his trial balance disagree by ₹ 2,800. He temporarily debits a Suspense Account with this amount and closes the books. On an examination of the books, the following errors are discovered:-

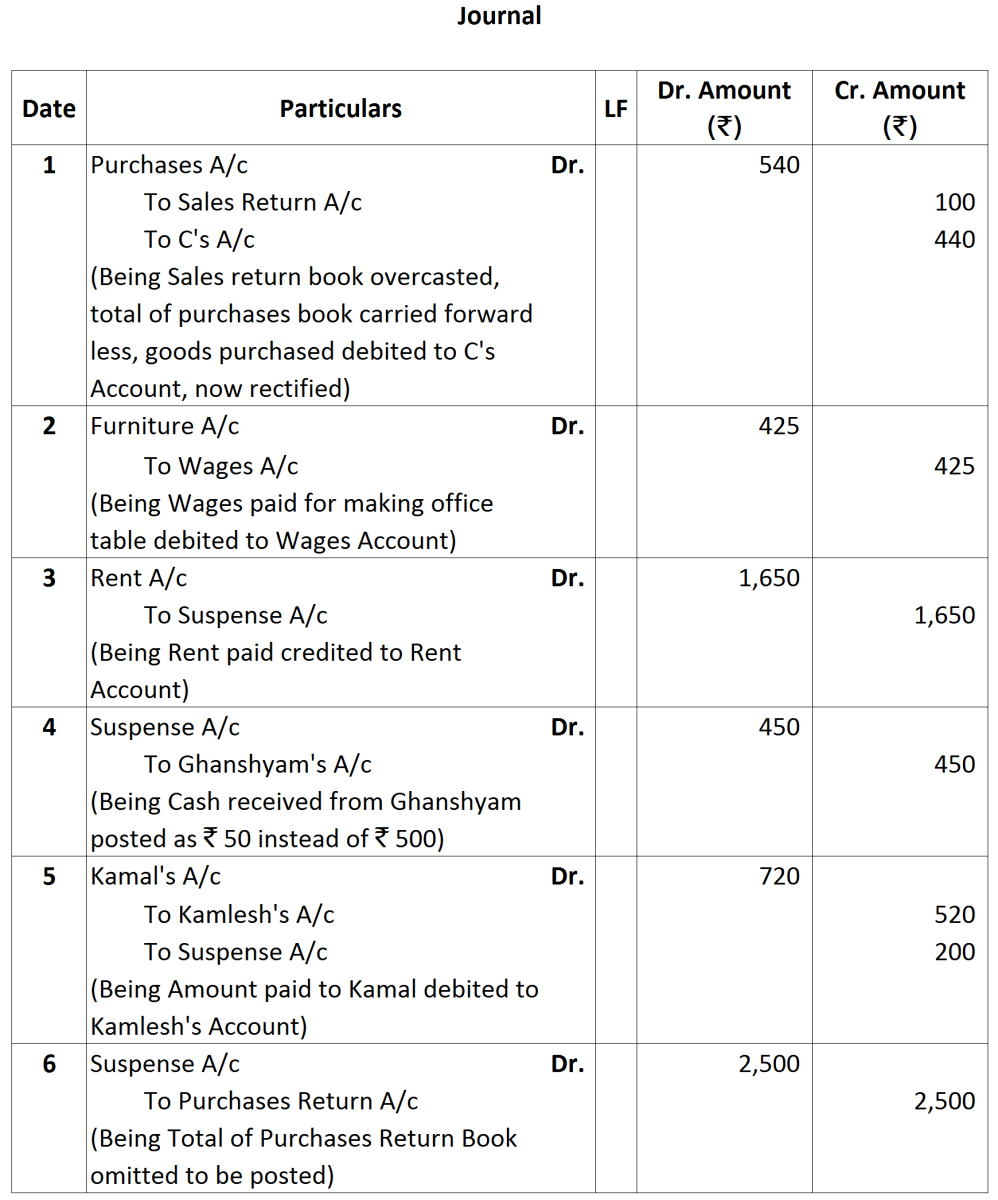

- The total of Purchase Return Book ₹ 710 was posted Twice.

- Goods costing ₹ 800 were distributed as free samples but no entry was passed in the books.

- Purchase of Machinery for ₹ 5,600 on credit was recorded in Purchase Book as ₹ 6,500.

- Cash Sales to Ram Lal for ₹ 1,200 were recorded in Cash Book as well as in Sales Book and were posted from both.

- Closing Stock has been overvalued by ₹ 1,500.

- Sales Return Book was untotalled, though personal accounts were posted ₹ 1,580.

- No entries have been made in the Cash Book for the Insurance Premium directly paid by bank ₹ 700 and interest charged on overdraft ₹ 320.

- A sum of ₹ 200 for Drawings on the Credit Side of Cash Book was not posted to the Drawings account.

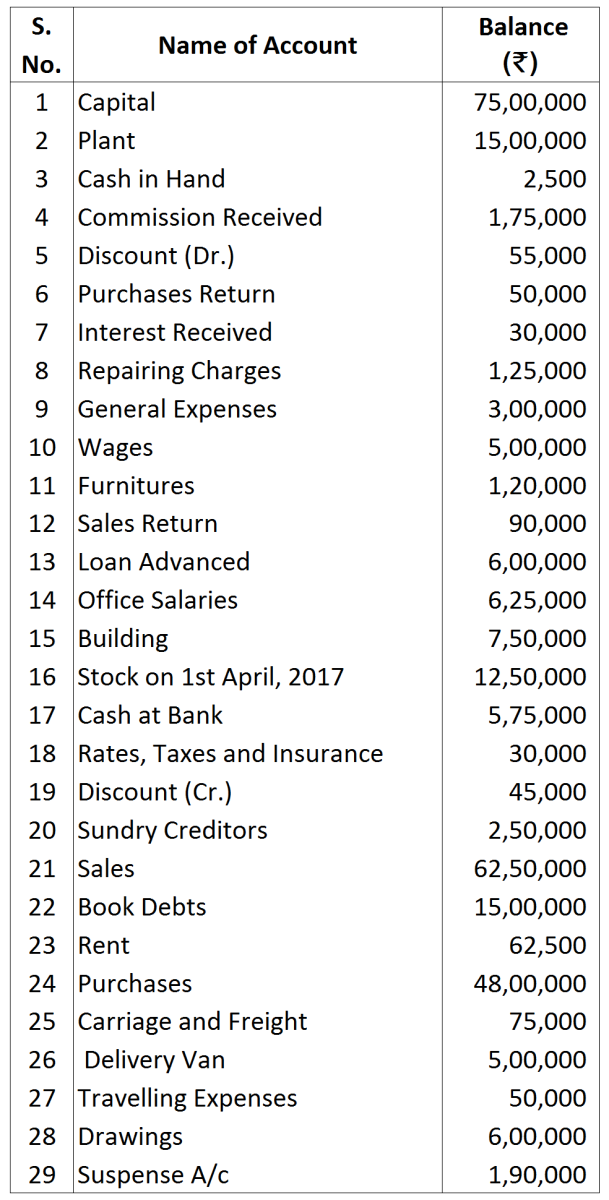

You are required to prepare the trial balance treating the difference as his capital.

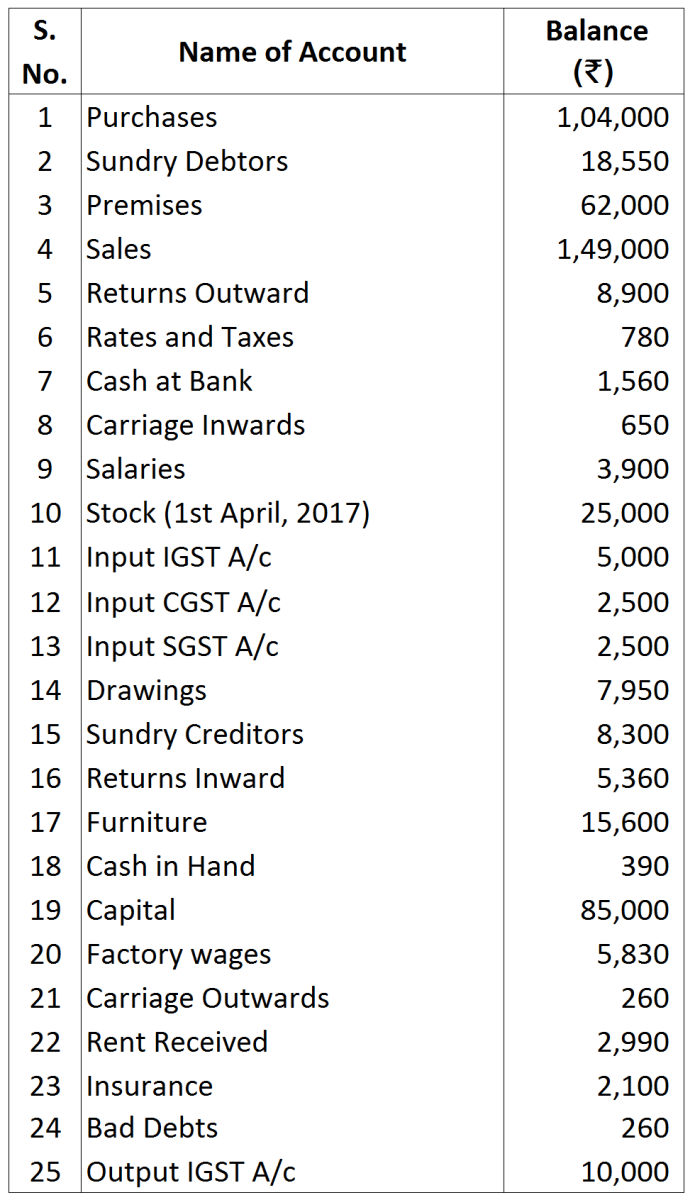

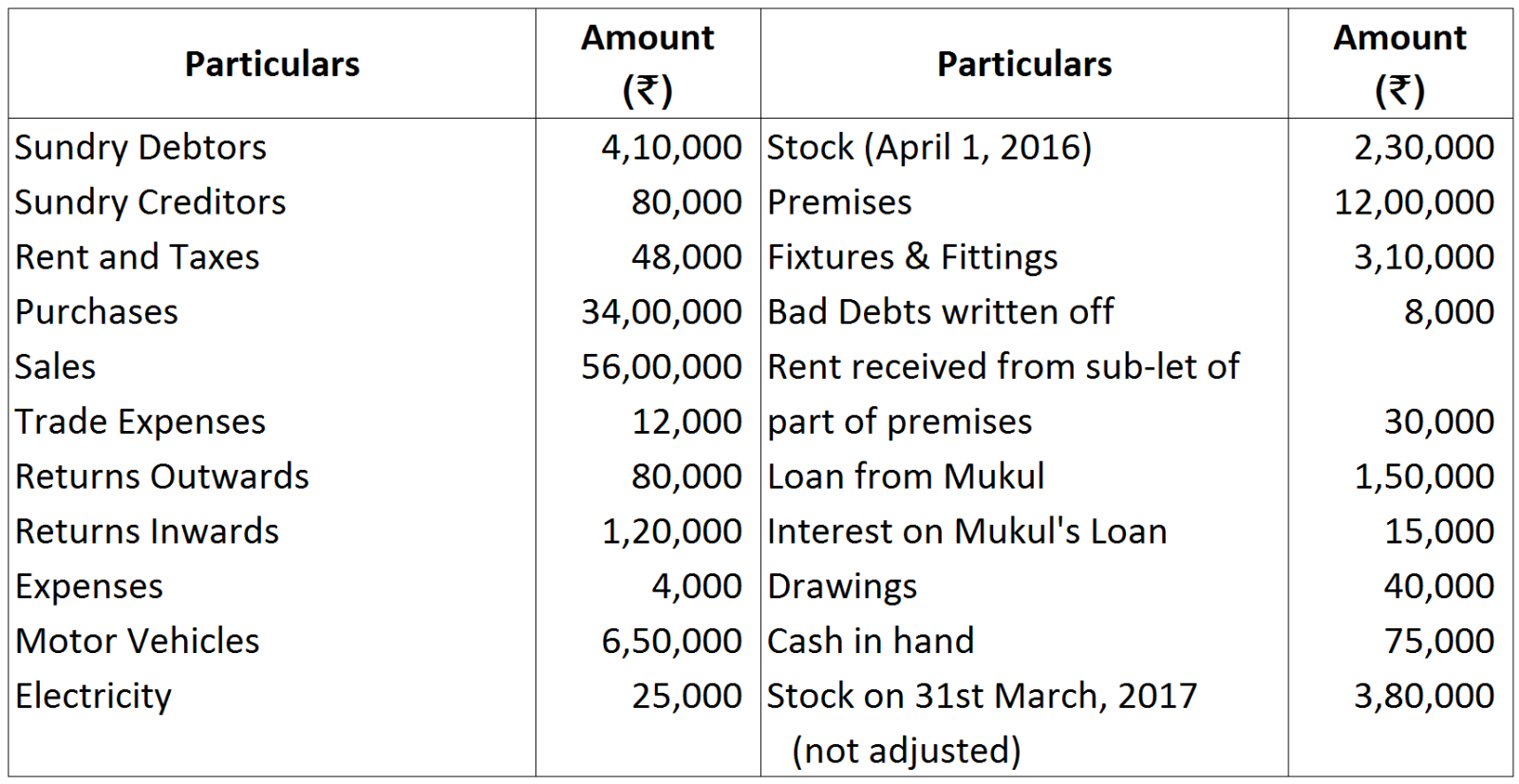

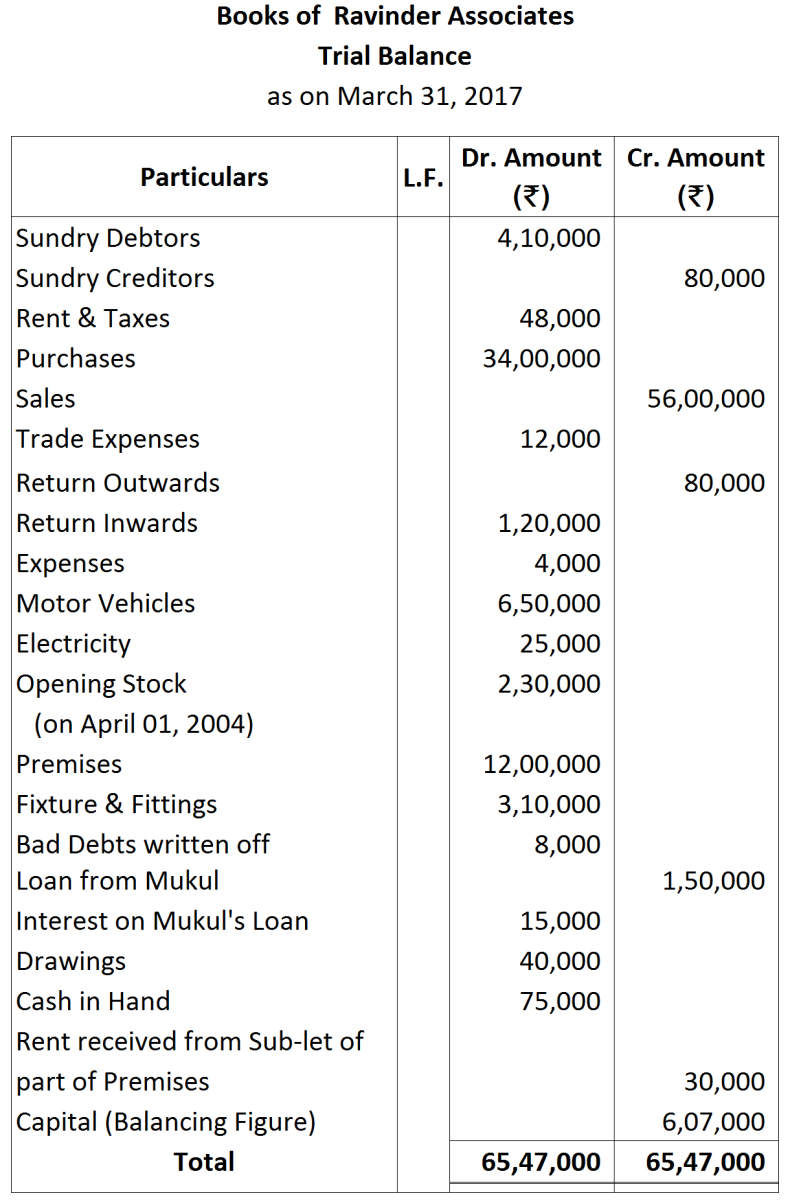

You are required to prepare the trial balance treating the difference as his capital. Note: Closing Stock of ₹ 3,80,000 will not appear in Trial Balance, because it has not been accounted yet.

Note: Closing Stock of ₹ 3,80,000 will not appear in Trial Balance, because it has not been accounted yet.

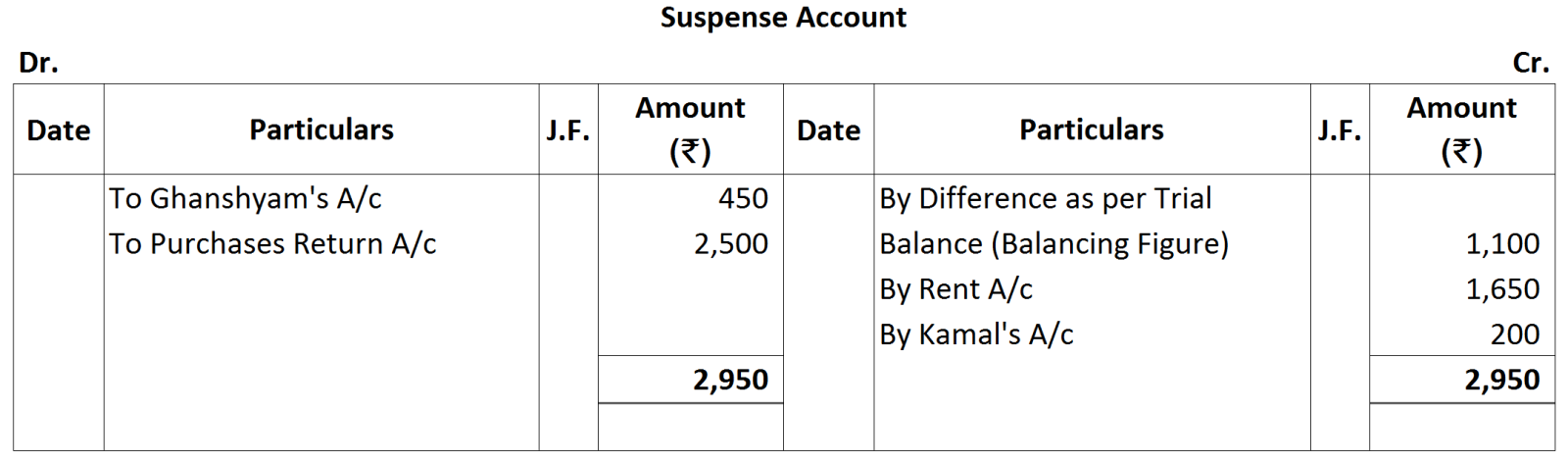

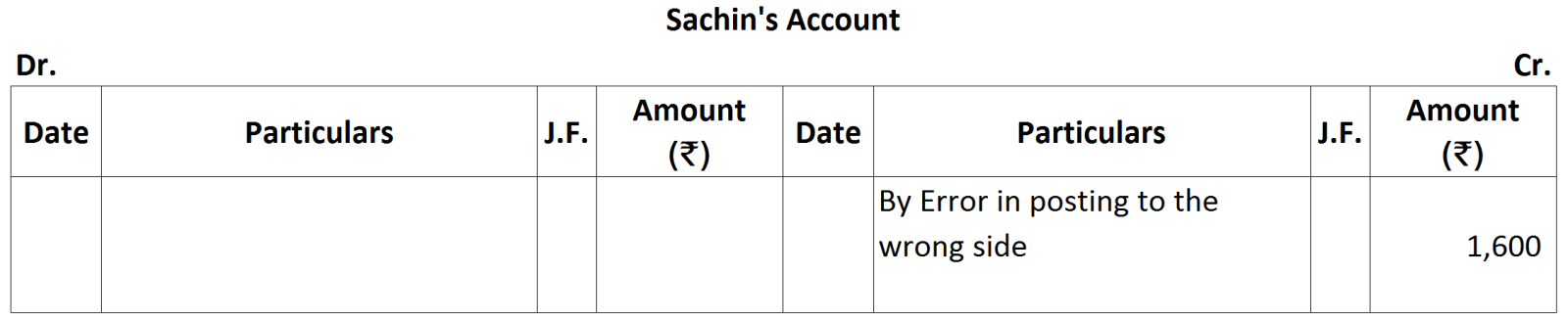

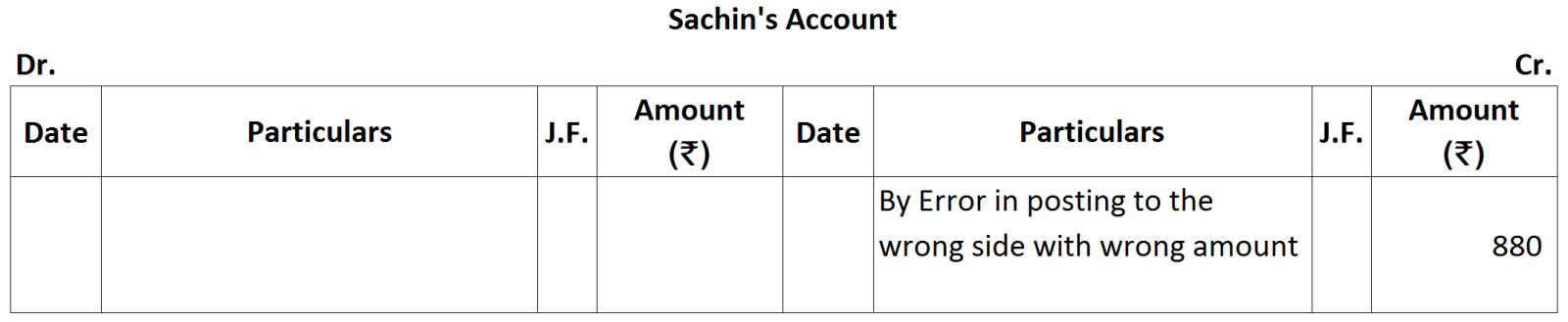

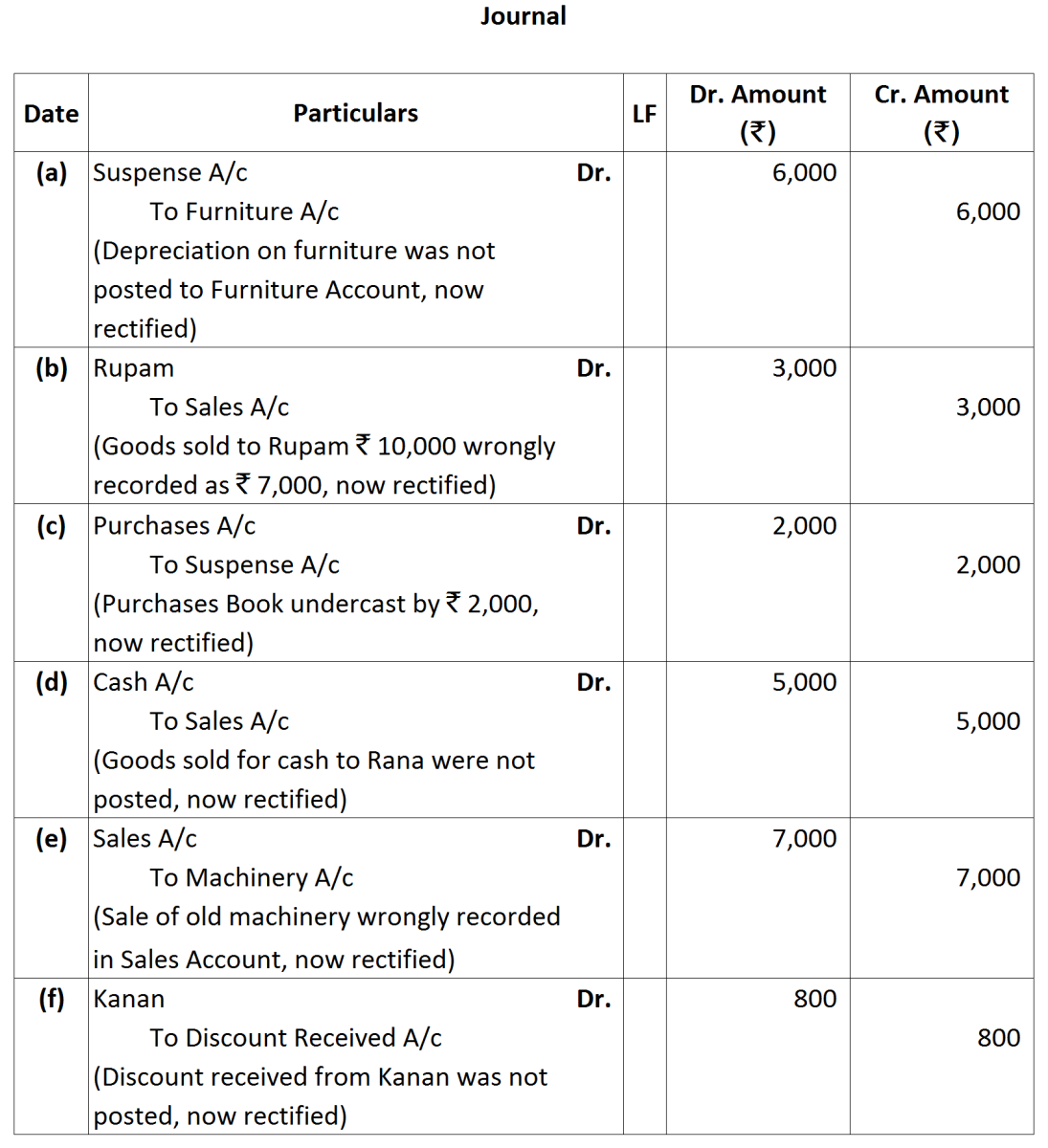

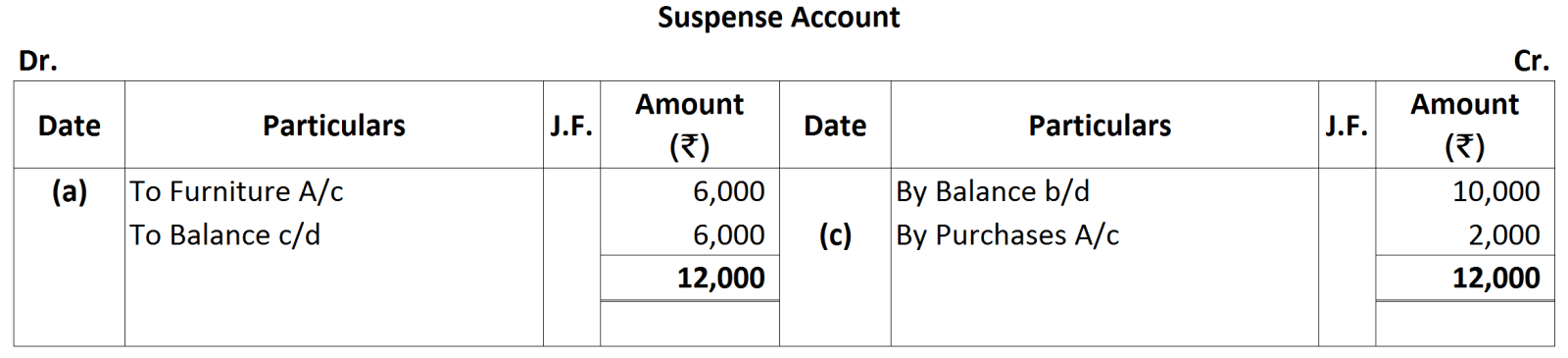

Note: As per the solution, suspense account shows the credit balance of ₹ 6,000. However, in the book the answer is credit balance of ₹ 1,000. So, in order to match the answer with the book item (d) is taken as, ‘Cash Sales to Rana ₹ 5,000 were not posted to the sales account.’ Thus, the rectifying entry of this error will be:

Note: As per the solution, suspense account shows the credit balance of ₹ 6,000. However, in the book the answer is credit balance of ₹ 1,000. So, in order to match the answer with the book item (d) is taken as, ‘Cash Sales to Rana ₹ 5,000 were not posted to the sales account.’ Thus, the rectifying entry of this error will be: