Question 14 Marks

Given the following information:

Answer

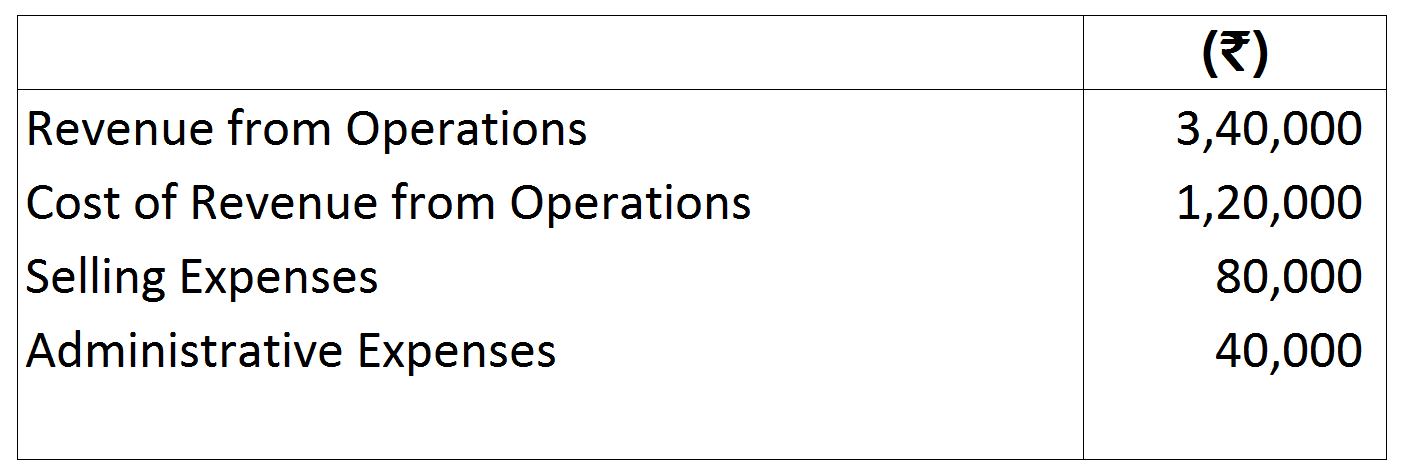

View full question & answer→Gross Profit = Revenue from Operations - Cost of revenue from operations

= ₹ 3,40,000 - ₹ 1,20,000 = ₹ 2,20,000

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations}}\times100$

$=\frac{₹\ 2,20,000}{₹\ 3,40,000}\times100=64.71\%$

Operating Expenses = Selling Expenses + Administrative Expenses

= 80,000 + 40,000 = 1,20,000

Operating Ratio $=\frac{\text{Cost of Revenue from Operations + Operating Expenses}}{\text{Net Revenue from Operations}}\times100$

$=\frac{₹\ 1,20,000+₹\ 1,20,000}{₹\ 3,40,000}\times100=70.59\%$

= ₹ 3,40,000 - ₹ 1,20,000 = ₹ 2,20,000

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations}}\times100$

$=\frac{₹\ 2,20,000}{₹\ 3,40,000}\times100=64.71\%$

Operating Expenses = Selling Expenses + Administrative Expenses

= 80,000 + 40,000 = 1,20,000

Operating Ratio $=\frac{\text{Cost of Revenue from Operations + Operating Expenses}}{\text{Net Revenue from Operations}}\times100$

$=\frac{₹\ 1,20,000+₹\ 1,20,000}{₹\ 3,40,000}\times100=70.59\%$

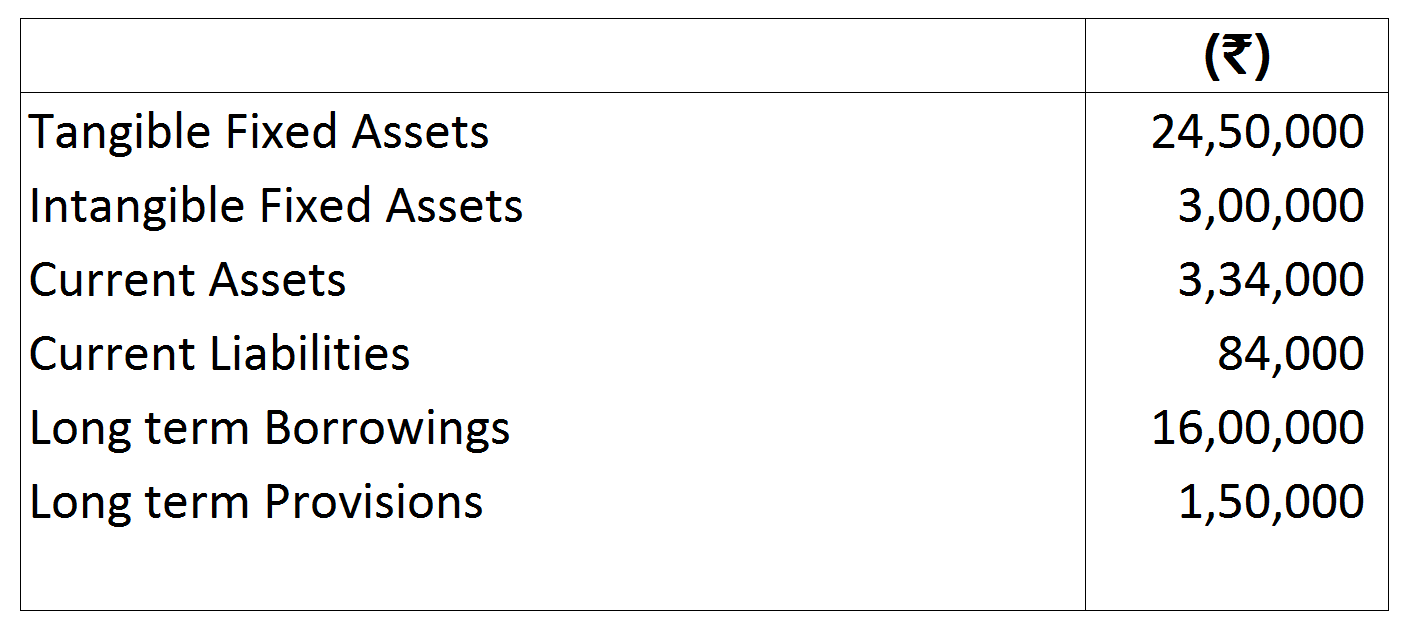

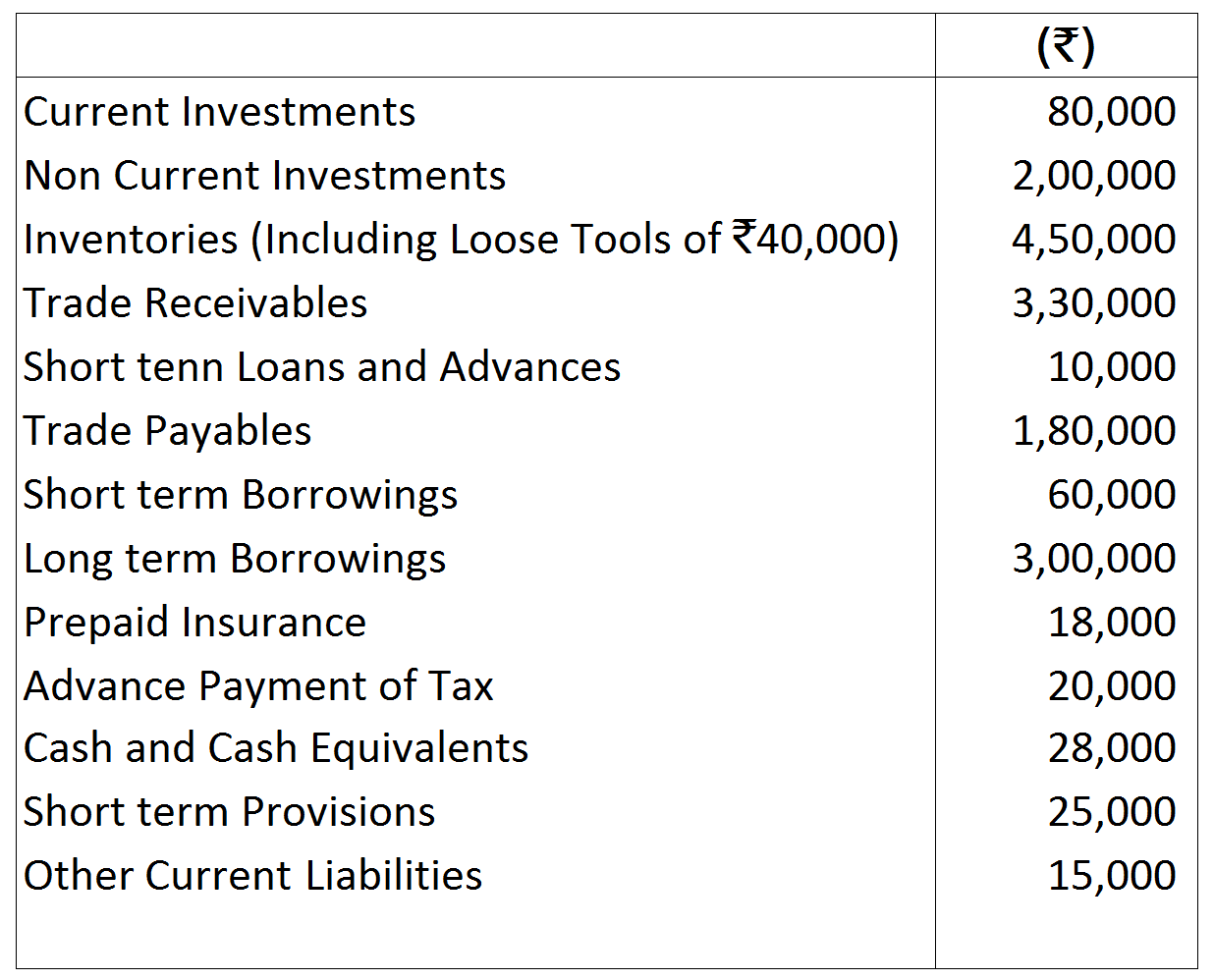

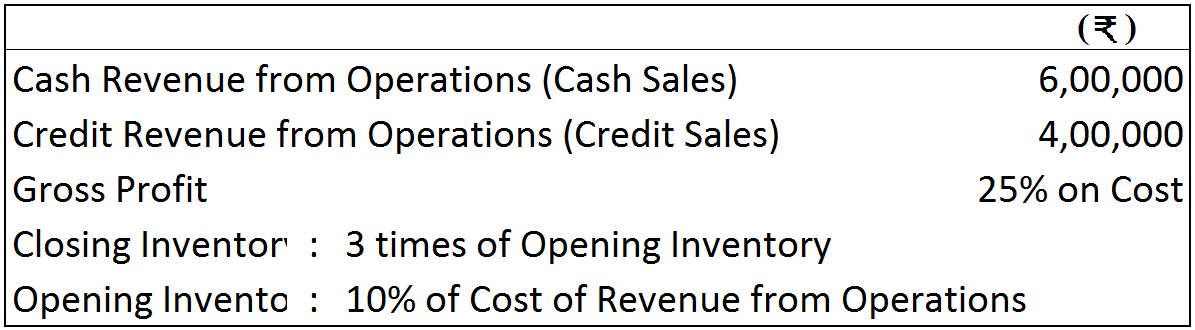

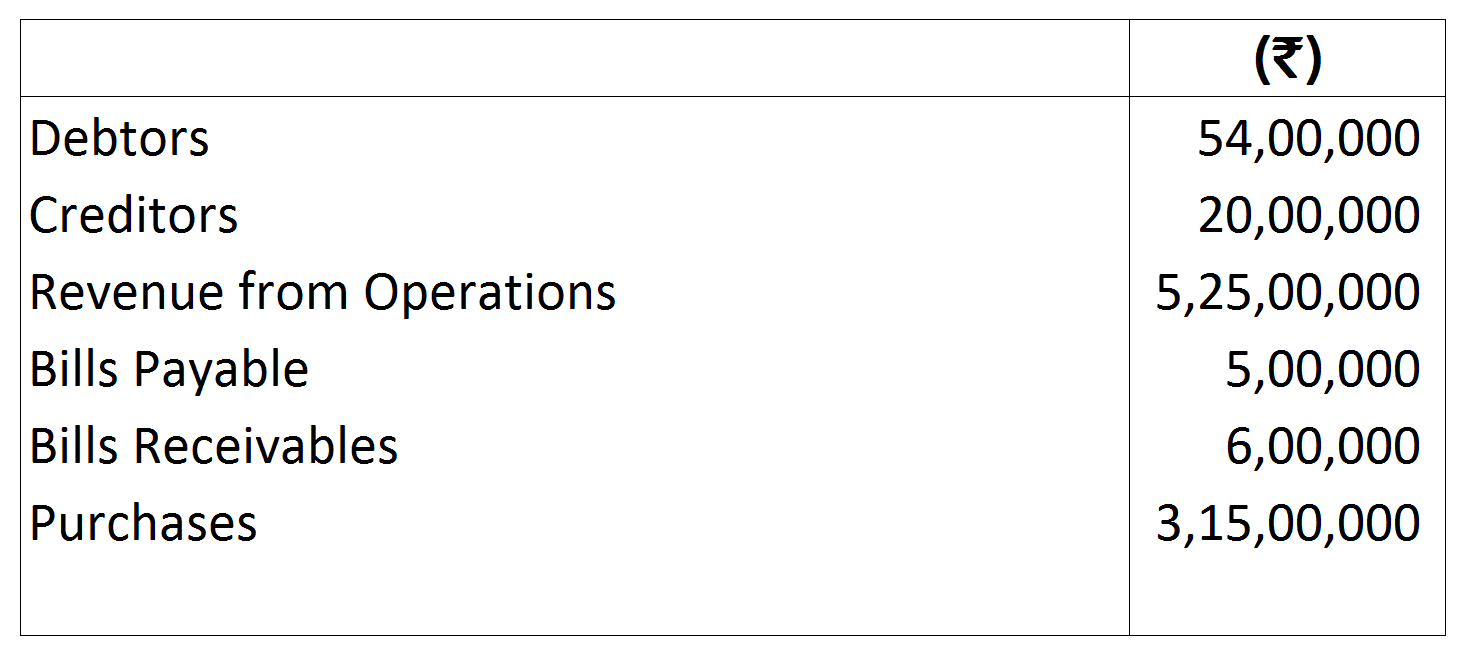

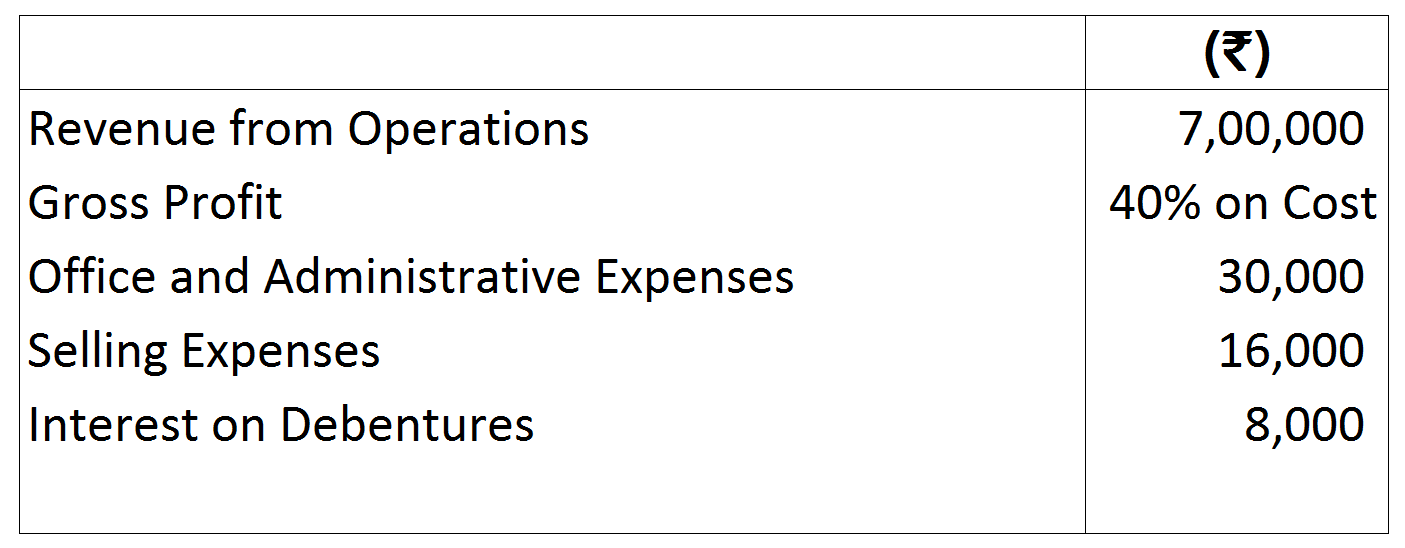

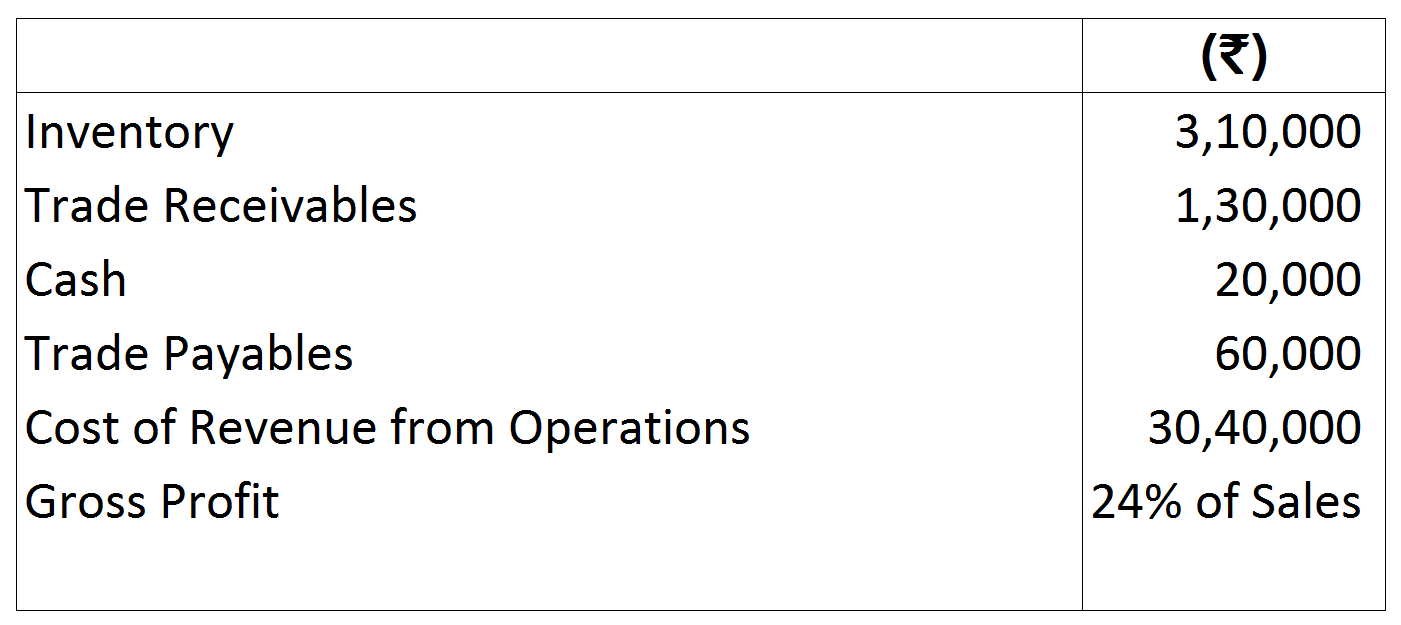

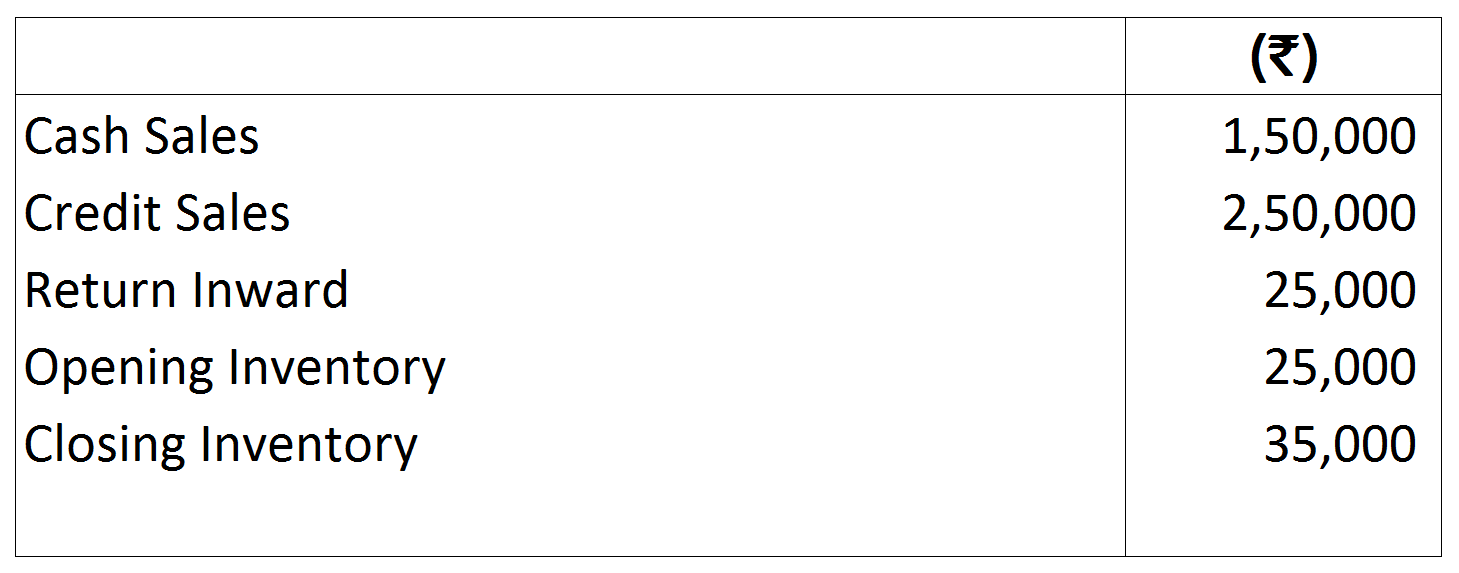

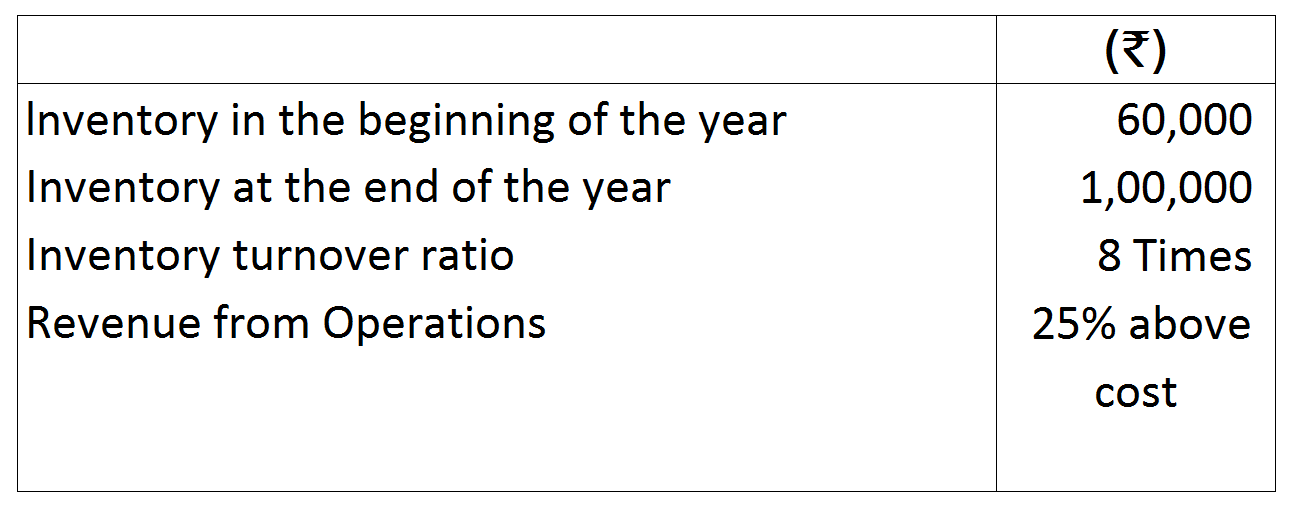

Compute the amount of gross profit and revenue from operations.

Compute the amount of gross profit and revenue from operations. If the closing inventory is more by f4,000 than opening inventory, determine the following:

If the closing inventory is more by f4,000 than opening inventory, determine the following: